Bulls and bears have seen more Square angles than your high school geometry text. But lapping its one-year anniversary, the payments processor may be smoothing out some rough edges, gaining traction on margins and larger merchants. We break it all down.

We promised we would not start this article with “what a difference a year makes.”

We will remain true to our word.

What a difference a year and two days make.

Since payments processor Square debuted on the public markets slightly more than a year ago, the stock and the company behind the stock have been on a wild roller coaster ride. Maybe the ups and downs may even out a bit, given the latest results seen early in the month.

But first a bit of chronology. Square priced at $9 a share right before its IPO last Nov. 19, and that was below the projected $11–$13 range, a range that was below the $15.46 a share that had been raised in private investment rounds prior to going public.

The company was one of the vaunted unicorns, among the firms sporting $1 billion plus valuations, and was seen at the time as being a canary in the coal mine, of sorts, for how unicorns would go to market — or not — amid fickle investors.

The first day of trading did see the company get a boost as shares rebounded within the initial pricing range out of the gate, to more than $13. The high headed into the next few months came in at $14.78, and then sank to $8 and change in February, and then back to almost $15.48 in April, and then back to the IPO price at $9. See what we mean by dizzying rides?

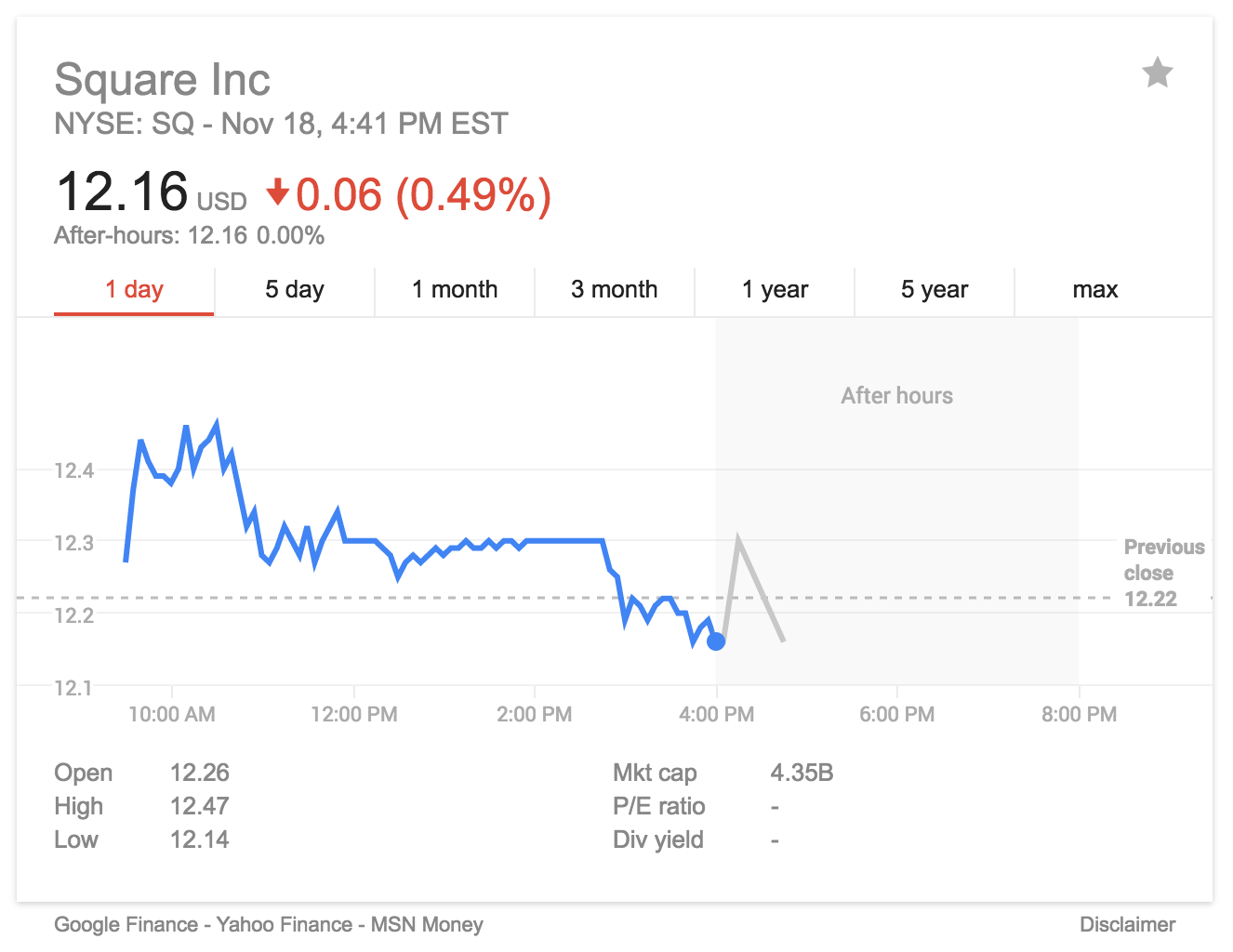

Now, the stock stands at $12.16. And looking at that rise, though admittedly below previous levels, it’s important to notice investor attitude towards the fortunes of the company and the actual fortunes themselves.

The first caveat is that the company is a bit away from turning a bottom line, a hallmark of many a growth-y tech firm. Projections call for the firm to lose as much as $0.31 on revenues of as much as $2.1 billion in 2017, with the sales number representing as much as 24 percent growth.

There are other issues that are company-specific, of course, and they include the fact that Square is helmed by Jack Dorsey who also created and steers Twitter. The “show-me” story that has hovered around the stock will likely stick as long as Dorsey wears those two hats, and skeptics wonder how he keeps appropriate focus on both firms.

The business case for Square has also had its measure of skeptics on The Street. The company still depends on its core processing, with an emphasis on smaller merchants paying 2.75 percent of the transaction value passing through Square readers (the value proposition here has been that, even the smallest and somewhat remote businesses, can accept multiple forms of payment). In addition, as the merchant of record, the firm takes on the risk of the (mostly) smaller merchants it onboards — although it has reported that a growing percentage of its merchants are larger, smaller merchants. (Larger smaller means $125,000 or more in annual revenues.)

Square also takes on the cost burden of fees per transaction that are typically paid out to Visa and others. Analysts (and Barron’s) have taken the measure of the smaller transactions and surmised that loss-making activities persist at levels below $10, while the firm has not disclosed just how much of its business falls below this threshold.

In any event, it is the latest quarter that has helped Square turn a corner, so to speak, and bring the stock from an October end level of $11 to north of $12 now.

Square’s most recent numbers were good enough, and more importantly, the momentum was good enough so that Square beat its own guidance. The all-important gross payments volume was up 39 percent to $13.2 billion as measured in the third quarter, year over year. That was a high-level surge that translated into top-line gains of 32 percent year over year to $439 million. Even the net loss was better than expected, $0.09 a share in red ink, where analysts had foreseen $0.11. The gross payments volume was most significant for the amount that came from larger sellers and had jumped 55 percent year over year. This increase shows that Square is indeed gaining ground in its effort to grab larger (and more lucrative) transactions. As of the third quarter, 43 percent of sales came from those merchants who have logged $125,000 or more in annual revenues, a good boost from the 37 percent contribution a year ago. Square has also been able to streamline the transaction speed measured across its EMV devices to about four seconds from six seconds. Every second counts when you want to please consumers and merchants and eliminate friction at the point of sale.

Going forward, it just may be Square Capital that gains the most eyeballs, with growth at 70 percent in the latest quarter and stretching through 35,000 loans. Cumulatively, Square’s lending arm has doled out more than $1 billion to 100,000 firms. Boosting guidance over The Street for the top line has helped the stock, too. The positive momentum just might continue on payments volume, with traction among larger merchants and lending, if there will be as big an expansion in domestic spending as some might expect (via the incoming administrations at the congressional and presidential levels).

Square has circled a roller coaster first year and may have a smoother ride ahead.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More