Six billion and counting. According to VantageScore, that’s how many credit scores generated by its model have been used by card issuers and other industry participants. Yet, VantageScore tells PYMNTS, there remains one category in which the use of alternative scores has yet to take hold. Can you guess which one?

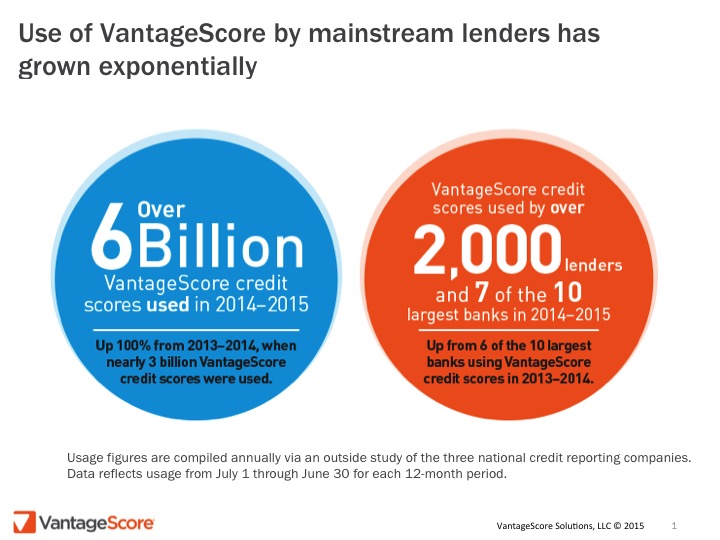

ShutterstockAccording to an outside survey, more than 6 billion VantageScore credit scores were used from July 1, 2014 to June 30, 2015, showing a notable spike in usage compared to the previous 12-month period, in which just 3 billion VantageScore credit scores were accounted for.

The company noted that the growth in the use of credit scores in recent years coincides with the increased use of credit scoring models that more accurately generate scores for millions of people who would otherwise be ignored by conventional credit scoring models.

However, according to VantageScore, there is still one category that continues to exclude potential borrowers based on the ongoing use of outdated scoring. The mortgage origination market is experiencing slower growth due to lenders being forced to use a credit scoring model based on data from 1995-2000, the company stated, adding that it hopes to encourage mortgage lenders to use more updated credit scoring models going forward.

The usage of VantageScore credit scores reflects the number of requests for and receipts of VantageScore credit scores by any user for any reason during 12 months preceding the report, which the company said has surged due to the new ways these scores are being used in the market.

The determination of creditworthiness for credit cards is where credit scores are most often used, with significant growth attributed to card issuers, VantageScore explained. Not only has the company witnessed an increase in the number of lenders using its credit scores, but it also noted growth among websites that provide free credit scores to users.

Given the myriad of ways credit scores are now used in the market, the survey found it more valuable to roll all of VantageScore’s credit score usage into one total number, rather than attempting to break it down more granularly by specific usage segments.

“We are seeing tremendous growth in many consumer lending categories, and bypassing the 6 billion scores used marks a major milestone for the VantageScore model,” Barrett Burns, president and CEO of VantageScore Solutions, said in a press release.

“Lenders are clearly seeing the benefits of greater predictiveness, consistency and the ability to score more people that the VantageScore model provides, and consumers are reaping the benefits of innovation bred by the competition we bring to the credit scoring market,” Burns added.

To measure the overall usage of VantageScore credit scores, the study polled the three national credit reporting companies (CRCs), which are responsible for selling credit scores to lenders and other users of credit scores. The uses of these credit scores by consumer lenders include functions such as marketing, underwriting, pricing, portfolio management, model building, testing and validation.

According to the survey, CRCs also noted that seven out of the 10 largest financial institutions in the U.S. utilize VantageScore credit scores.

While there remains a growing number of branded scoring systems available in the consumer credit market today, VantageScore emphasized the need for consumers to look at their credit score as an educational tool, no matter which scoring model they decide to go with.

To put it simply, there is no one-size-fits-all credit scoring solution for all lending decisions.

“A credit score is indicative of the information in your credit report, which in turn reflects credit behaviors which is where consumers should concentrate on improvement if their score is low,” the company said.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More