There’s nothing like that new car smell. And the fun of driving a new car off the dealer’s parking lot.

But the process of getting there is anything but fun, especially if one is financing a car. Even when the process has gone swimmingly and the customer has found the right ride, in the right color, with the right trim package that’s in the right price range — the proverbial friction hits the fan when it comes down to negotiating the final deal.

Sometimes there is a four-box diagram drawn out, usually involving several visits with the manager/head of customer auto financing as part of the negotiations. Bad coffee from Styrofoam cups is consumed. The customer starts to question what’s so wrong with some combination of the Old Bessie they drove there and Uber.

This struck the team at AutoGravity as a particularly strange hole in the car shopping marketplace — considering how much of the auto financing process had already been made transparent through the magic of hip pocket access to the internet.

“What is interesting, if you are a consumer today, there are almost unlimited resources when it comes to researching the purchase of a new car — there are … endless suppliers. When it comes to financing your car, your smartphone goes dark,” AutoGravity’s CFO Lukas Wickart told Karen Webster in a recent conversation.

The startup was founded, he explained, to find the pain points in the customer journey from researching a new car to driving off the lot with it. The firm quickly discovered that transparency and speed were where the consumer experience cratered.

Building on Consumer Feedback

In the early days, AutoGravity had a seed investor named Daimler Benz and an idea or two about building transparency into the lending process that consumers did as part of the car shopping experience but didn’t enjoy.

“The tough part about the beginning is that we didn’t really know if [making financing easier using a mobile app] is what consumers wanted. So we built a minimum viable product and put it out there for consumers to play with,” Wickart said.

Mission accomplished, Wickart told Webster, since through that process, AutoGravity learned a lot about what consumers liked and what they didn’t, where the app worked and where consumers were getting stuck. Wickart said that a large part of their strategy, product and road map came from that first round of consumer feedback they got.

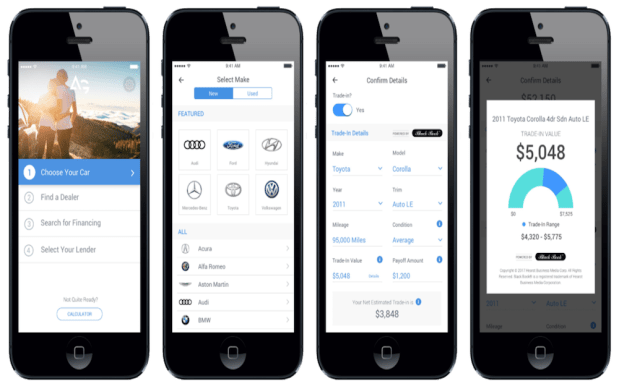

Which has led to a platform today that has moved beyond helping a car buyer find financing and get pre-approvals for the car they want to buy, to the ability to browse new or used cars by make, model, trim package — and price; find local dealers with cars that meet those specs and visit those dealers, car loan offers in hand, to close the deal.

“That is good news for a car dealer because you know this person has made up their mind, chosen a car and gotten a deal approved. Now all you have to worry about is closing the transaction — that means we function as an acquisition channel for dealerships that is way below their normal acquisition costs for customers.”

And having an auto loan that works for dealers, Wickart noted, is important, because in the firm’s early days, they weren’t certain that would be the case.

Working with Everyone (to Get More Cars Sold)

The early perception, Wickart told Webster, was that dealerships wouldn’t like what AutoGravity was doing, because arranging auto loans for consumers is/was part of their dealership revenue model. But Wickart told Webster that’s also why their platform was built as a complement to — rather than a competitor of — those existing dealer lending options. It’s made partnering with the largest auto dealerships in the nations a much easier ride — pun intended.

“From [the dealer’s] perspective, if we can bring qualified buyers to a dealer with the car that they want to buy, that’s a good deal any day of the week,” Wickart said, adding that AutoGravity is viewed by dealers as a “great” millennial customer acquisition channel.

Millennials, Wickart pointed out, are a group whose buying power and credit-worthiness is increasing, but for some, automotive manufacturers have been out of reach. Daimler, their original investor and the makers of the Mercedes, has an average age in dealership financing of 55. Which is good news for AutoGravity, whose average finance customer’s age is 33.

It’s why, Wickart also noted, they caught the attention of VW (Volkswagen) Credit, who invested in the company last week and have increased their partnerships with an ever-increasing number of dealers.

“I think with this business, this isn’t rocket science; we are giving the consumer what they want — the ability to fully finance a car with their mobile device and decide on the terms they want.”

What’s Next

Among the surprises of the development of AutoGravity, Wickart noted, was that even though consumers have many resources available to shop for specific cars out in the marketplace, many were coming to the AutoGravity alt lending platform looking to shop for a specific car (as opposed to a specific type of car) to go with the car loan they were shopping for.

“For us, that was a big surprise and a good one,” Wickart noted, saying it has given them more ground on which to work directly with auto dealers, as they can move more customers to their specific lot looking to make a specific, and pre-approved, deal.

“There is a big push to integrate real live inventory where we can show the actual car available on the dealer’s lot because we found customers were saying they don’t just want a Jetta — they wanted to be able to find a specific Jetta to purchase. So you can use AutoGravity to search a specific VIN on an actual dealer’s lot and arrange for financing.”

The car loan offers, he noted, are priced to MSRP — so though there can still be some pricing negotiation at the end, the customers have the comfort of knowing they won’t be charged more than the car is worth.

“If you negotiate on the car and do better, your payment will go down accordingly. Car buying is like booking a vacation, there is the happy thing waiting at the end, but you have to get through this tedious process to get to the reward. We try hard to make this not tedious, smartphone-based and with binding offers, [so] you know all the info you need when you get to the dealer.”

Because what customers want, he noted, is transparency in alt lending — which means his firm’s roadmap for the future is pretty well laid out.

“Keep building to the features customers are asking for and make it easier for them to decide what type of deal they want, because ultimately that will sell them the most cars.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More