“There is also no question that doing business with [XXX] can give a supplier a fast, heady jolt of sales and market share. But that fix can come with long-term consequences for the health of a brand and a business.”

I’m sure that most of you reading that quote today would ascribe those XXXs to Amazon. Along with similar quotes about XXX killing Main Street and jobs and becoming an evil monopolist.

It’s not a bad assumption, either, given the many media accounts of Amazon’s MO for putting the big squeeze on wholesaler prices so that it is the cheapest guy in the online town. One such article, recently published in Salon, reports that the firm’s “predatory” pursuit of discounts from brands that wanted to be part of the Amazon platform were driving those firms’ profits to unhealthy low- or even no-margin situations, that they claim force many smaller retailers to close up shop.

So, would you believe me if I told you that the quote was from an article published 14 years ago, in December 2003, by Fast Company — about Walmart?

Believe.

The Retail Predatory Pickle

The article was written as sort of an exposé of Walmart’s supplier negotiating practices, using a $2.97 gallon jar of Vlasic pickles as its main character.

The $2.97 price was negotiated as part of a deal that the storied pickle maker made with Walmart in the mid-to-late 1990s, a price that was also less than what most grocery stores had priced a quart size jar. At $2.97, the price for this mother of all pickle jars of whole cukes (it weighed 12 pounds) was so low that the article claimed that both Walmart and Vlasic were making “only a penny or two” on the sale of each.

As the story goes, Walmart put the squeeze on Vlasic to commit to that price point, even though tests done before the launch showed pickles flying off the shelves at a price slightly north of three bucks a jar. Walmart said no, and since Walmart was 30 percent of Vlasic’s business, Vlasic stood down, hoping that this loss leader would pull through on the sale of other Vlasic products that consumers would buy once inside a Walmart store.

And boy, did the people buy the pickles!

In fact, consumers bought more kosher dills than any one person could humanly eat. The great American pickle promotion at Walmart was reported to have moved 240,000 gallon jars of pickles each and every week at Walmart’s 3,000 stores, driving tons of foot traffic to Walmart. Walmart and Vlasic made the prices of pickles so insanely cheap that if people wanted to buy pickles, Walmart was where they went to buy them.

It also, unfortunately, created something of a real pickle for Vlasic.

Consumers bought pickles all right, but they stopped buying the kind that Vlasic makes money on — what they call “the cuts.” Why buy smaller jars of those pricey pickle slices, spears and relish when those same consumers could be kept awash in pickles for the low, low price of $2.97? If the pickles got yucky before all 12 pounds of them could be eaten, NBD, just run back to Walmart to buy a brand new 12-pound jar for that everyday low price of $2.97.

Vlasic execs continued their pleas to raise prices to cover what was becoming a real double edge for their company: record sales and sales growth but shriveling margins. Consumers changed their pickle-buying habits — chopping and slicing and mincing those $2.97 jars of whole cukes instead of buying them ready-made. Vlasic told Fast Company that they were finally permitted to raise prices when Walmart said they’d won the pickle market and could now slowly raise prices.

Shortly thereafter, in January of 2001, Vlasic filed for bankruptcy. Its pickle and BBQ sauce business was bought by Heinz later that month for $195 million. At the time, Vlasic held a 24 percent share of the pickle and condiment market to Heinz’s 3 percent. As the Fast Company article points out, Vlasic’s business had a heap of other issues that drove it into Chapter 11 status, and the great gallon-jar pickle caper was likely one idea hatched by them to pump up the brand with the hopes of pulling through the sales of higher margin pickle products.

Today, that same gallon of pickles can be bought at Sam’s Club for $4.18.

Hold that thought for a minute — it will become important later.

Ironically, the reason that Vlasic was willing to do that deal with Walmart in the first place was to access the 100 million consumers who visit a Walmart once a week and spend 7.5 cents of every dollar with them when they do. For Vlasic, Walmart accounted for 30 percent of their sales and was thus a very important channel to the customer. Walmart, as a powerful intermediary between Vlasic and its customers, negotiated accordingly.

And it wasn’t just Vlasic that Walmart put the squeeze to — it’s just about everyone, including the players in our own payments world, where Walmart is legendary for driving a very hard bargain for how much they are willing to pay in interchange (zero is the best, and they’working on it) and even what payment methods they’ll accept in their stores.

Walmart’s comeback to anyone who pushed back was simple: Don’t sell your stuff in our stores. We promise everyday low prices, they say, and can drive a ton of customers your way — remember that 90 percent of the U.S. population lives within 20 minutes of one of our stores.

But, they continue, for us to live up to our brand promise of giving our consumers a good deal, you need to give us a good deal. And, you need to be operationally efficient. We know that serving 100 million consumers every week can crush a business, so if you can’t adapt your own processes to avoid that from happening, then we can’t do business together.

It was pretty much take or leave it. And lots of people took it — and still do.

This gave Walmart tremendous power — which made the company a threat to suppliers, whose margins it cut into, and Main Street, who couldn’t compete, and all those people who worked at those Main Street brick-and-mortar stores. That’s what pundits talked about a lot back in the 1990s and much of the 2000s.

But back in 2003 when that article was written, Walmart was just the latest version of an intermediary that aggregated brands into a single place that made it more efficient for consumers to buy goods from a variety of different brands — and for those brands to reach a critical mass of would-be buyers.

Department stores did that in the late 1800s, when for the first time, consumers didn’t have to hoof it up and down Main Street to buy the things they needed from individual merchants.

Shopping malls took that model a step further in the mid-1950s by making it possible for a collection of stores to be assembled under the same enclosed, climate-controlled roof for the convenience of a shopper. Mall of America, the largest in America, has 520 shops and 50 restaurants, attracting 42 million people — a year. Woodfield Mall, outside of Chicago, and one of the most visited malls in the U.S. aside from Mall of America, pulls in 27 million each year.

Each of these intermediaries has their own rules of play, too — sell us stuff a price at a low price so we can mark it up and make a profit or pay us rent and a share of sales so that we can cover the costs of bringing consumers to your front doors and make sure that they can park for free and stay a long time.

But until Walmart, none of them had anywhere near the depth and breadth of consumer reach — and, therefore product distribution — and potential to drive buyers into their welcoming arms. Walmart offered brands — in one week — the kind of consumer foot traffic that it would take even the biggest mall in the U.S. — never mind one of the 520 stores there — two and a half years to see.

That is, until Amazon.

Amazon’s Hard Bargain

Amazon is the latest generation of intermediary that does what all retail intermediaries have done before it: assemble a bunch of things for consumers to conveniently buy.

And do that so efficiently that every other retailer now complains that their business is damaged.

Since its debut in 1995 as an online bookseller, Amazon’s captured roughly 5 percent of all retail sales (excluding autos — about 3.5 percent if you include them) in the U.S.

Amazon’s Prime customer base of 85 million (before any new additions from last week’s Prime Day) visit Amazon two to three times a month and spend twice as much as non-Prime customers when they visit. Those 85 million households cover about 215 million people, assuming that one membership covers the average American household of 2.53 members. Just about everyone who wants to buy from Amazon with a guarantee of two-day free shipping, more or less, can.

Amazon has taken the friction out of shopping — on or offline — by offering consumers more than just a convenience — it offered them certainty.

Certainty of price — the lowest or close to it — the certainty of selection — adding more brands and sellers by the day — for Prime members, the certainty of a two-day delivery and at checkout, the certainty of an easy, one-click experience.

That certainty means that Amazon is often the starting point for consumers when they want to buy something. In a separate study that we did in 2015, nearly 60 percent of consumers told us that they started their product hunting on Amazon, with a traditional search coming in third at 40 percent.

That certainty translates into app usage that dwarfs even the largest and oldest brick-and-mortar retailers.

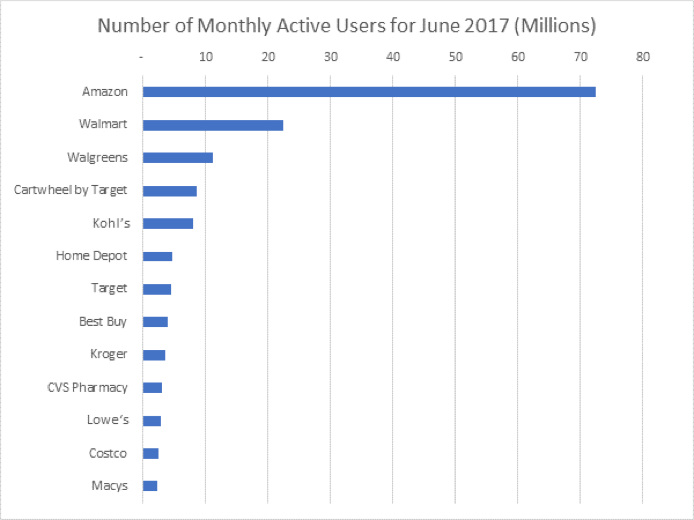

According to the latest App Annie data for June 2017, Amazon’s monthly active users beat out everyone pretty handily, and its nearest competitor, Walmart.com, by a factor of nearly three.

That certainty can be seen in its share of online spend. Amazon today accounts for just about one of every two dollars spent online and shows no signs of slowing down.

And, unlike most other retailers — clicks or bricks — the panorama of products that Amazon has assembled gives consumers a reason to visit them every day.

Not once a week to buy groceries, but today, when that consumer realizes that the paper towel supply is running low. Not once a month when it’s time to shop for clothes, but today when that consumer wants a new pair of Kate Spade sandals the day after tomorrow to pack for vacation. Not once a summer to get ready for the endless summer cookouts, but three or four or five times to buy summer placemats and garden planters and serving plates and other accessories for outdoor entertaining.

Meet the New Boss, Same as the Old Boss – Sort of

Amazon is a very new generation of intermediary, one with its roots in digital across now any number of connected access points: online, in their app and via a collection of voice-activated speakers.

And soon, in physical form with the acquisition of Whole Foods.

Amazon’s ecosystem of products, including music and movies, is now available to consumers across a number of Echo devices, including smartphones via its app and inside a number of existing products. Analysts say that Amazon and its 70 percent of the voice-activated speaker market — in less than three years — is already lightyears ahead in innovating the most natural interface for shopping — using one’s voice to ask a personal assistant to fetch them what they need. In fact, 14 percent of the consumers we surveyed as part of our How We Will Pay study with Visa say they own one, and 42 percent of those with six or more connected devices, including a voice-activated speaker, said they use it to buy things.

Amazon, as this new generation of digital intermediary, creates some interesting dynamics — and decision points for retailers.

If you’re a brand like a Nike or a Kate Spade or a Stuart Weitzman that relied on the more traditional intermediaries like a department store or even your own branded storefront in a shopping mall to drive traffic, being inside of Amazon’s ecosystem could up the odds of getting a sale.

And by a lot, since mall traffic is on the decline, dropping more than 8 percent in 2015 and more than 6 percent in 2016. Since consumers already use the brand name as part of their shopping search – I’m looking for Kate Spade sandals — being part of Amazon offers Prime members something that those malls and stores can’t deliver now — more than 70 million eyeballs a month and two-day free shipping, if someone decides to buy.

If, on the other hand, you’re a store that makes its living aggregating a bunch of those brands, you could be in a world of hurt.

Our research shows that consumers do start their searches with a store about 44 percent of the time, but it’s not always the case that the process of search leads to a sale at that merchant. And, as the interface for shopping becomes voice, that probability will diminish even further. It’s hard to imagine someone asking Alexa to search Macy’s for a Ralph Lauren shirt; they’ll just skip the Macy’s part and go right to the Ralph Lauren shirt.

The “hard bargain” that Amazon will drive for those brands is that part of their ecosystem is rooted in what they believe makes for a great consumer experience. In some cases that will be about being the cheapest guy in the online town — like Walmart and pickles — so that they can raise prices later or produce their own higher margin private label version of it. Part of the reason investors are so bullish on Amazon is because they expect that it will do both — since it already has.

In 2003, the Fast Company article made the point that the only thing worse than doing business with Walmart was not doing business with Walmart.

More stories followed about Walmart ruining retail and ruthlessly forcing the shuttering of generations-old mom and pop stores. Stores did close, but something else happened too: Retailers and brands were forced to think differently about their business and how to attract and retain customers in that new era of retail. Those who could, did and survived.

Fourteen years later, the storyline seems the same — only the names have been changed to reflect the changing of the retail intermediary guard. Where people once talked about Walmart, they now talk about Amazon — how they’re forcing retailers one by one out of business, how they’re dominating retail to the point where no one else can compete and how they’re forcing retail into one narrow, Amazon-branded box.

And just like before, we’ll see the same retail cycle repeat itself:

Stores will close, brands will disappear and those stores and brands who can think differently about how to attract and retain customers will survive and even thrive.

Like Walmart, Amazon is changing the face of retail by changing the expectations of what consumers will get when they go shopping. In many ways, those consumer expectations are no different than they’ve always been: being able to efficiently buy the things that they want to buy at a competitive price. But in a digital world, those consumer expectations now include getting those items shipped to their homes in two days and for free, without a lot of checkout friction along the way, and doing that anywhere they happen to be: commuting, while watching TV, in bed with a glass of wine after a long day at the office.

So, retail – meet the new boss – same as the old boss, sort of.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More