Contactless payment solutions have been around for several years but have been somewhat slow to catch on in the American market.

One report in 2018 revealed that just 0.18 percent of transactions at the point of sale (POS) in the U.S. were contactless, even though 70 percent of POS terminals were capable of processing such payments.

The pandemic is serving as a catalyst by driving the increased adoption of contactless payment technologies, however, prompting a growing number of consumers to seek out financial products that can deliver such experiences.

One study conducted in March revealed the rapid nature of this shift, finding that 38 percent of consumers believed offering contactless payment capabilities was a basic and necessary function of their payment cards — an 8 percent year-over-year increase. That finding also coincided with a dip in the share of consumers who said they did not need contactless payment capabilities, which declined from 41 percent in March 2019 to just 30 percent during the same month in 2020.

Many merchants have recognized that consumers value contactless payment experiences and have worked to offer them online and at the physical POS. Some card issuers are taking note as well, but many banks and credit unions (CUs) are still struggling to satisfy these new demands even as contactless payment solutions become more critical to consumers.

The following Deep Dive examines the rise of contactless payment tools during the pandemic and what CUs can do to meet members’ growing preference for them.

The Pandemic And The Push Toward Contactless Payments

Many financial institutions (FIs) in the U.S. have worked to roll out new payment tools for their customers in recent years, including P2P solutions. Their inclination to offer contactless payment tools, on the other hand, has been relatively muted — at least before the pandemic’s onset.

The Federal Reserve Bank of Boston’s 2019 Mobile Banking and Payment Survey of New England Financial Institutions polled 85 banks and 45 CUs across all six New England states to gauge the region’s shifting attitudes toward mobile and digital banking developments. It found that just 4 percent of the CUs surveyed offered contactless cards and that only 31 percent planned to provide them for members within the next several years.

Marianne Crowe, the study’s co-author and the vice president of the Federal Reserve Bank of Boston, explained that the pandemic would likely have a significant impact on this trend, however. She said public health guidelines recommending that consumers limit their physical interactions with merchants and POS terminals could make contactless payment solutions more appealing, positing that more FIs — including smaller players — would offer these payment tools in the future.

Contactless payments may have been less popular in the U.S. before the pandemic began, but more recent research examining the technology’s use abroad and domestically paints an optimistic picture for its continued adoption.

Card network Visa noted in April that 60 percent of the non-U.S. transactions it processed at the physical POS were contactless, for example, and a Mastercard study released during the same month found that 79 percent of consumers around the world were tapping contactless transactions.

A different study conducted in January found that 38 percent of U.S. consumers have used contactless payment options at every available opportunity within the past three months, while 54 percent expect to use such payments as much or more than they do now once the health crisis has passed.

Getting CUs On Board With Contactless Payments

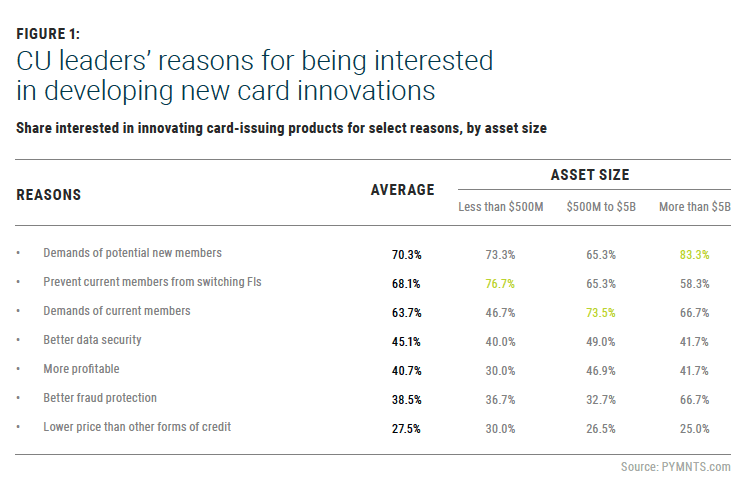

CUs have long been known for offering personalized customer service, and research shows that many have worked to tailor their payment card innovation strategies to members’ preferences. PYMNTS’ Credit Union Innovation Playbook: Card Trends Edition found that 70 percent of CU leaders considered the demands of potential members when innovating their card offerings prior to the pandemic, for example. Sixty-eight percent said they geared their card innovation strategies toward preventing members from switching to other FIs, while 64 percent said they innovated to meet current members’ demands.

Research also shows that CUs innovating their card solutions with current and potential members in mind would do well to focus on contactless card solutions. PSCU’s annual consumer payments study among CU members revealed a 72 percent year-over-year boost in the share who have at least one contactless card, for example. Fifty-seven percent of those polled said that they used contactless cards a few times per month before the pandemic began, a share that has since risen to 65 percent. Sixty-nine percent of respondents said they anticipate continuing to use their contactless cards at least a few times per month even after the pandemic ends, illustrating the value and staying power that these payment tools now hold for CU members.

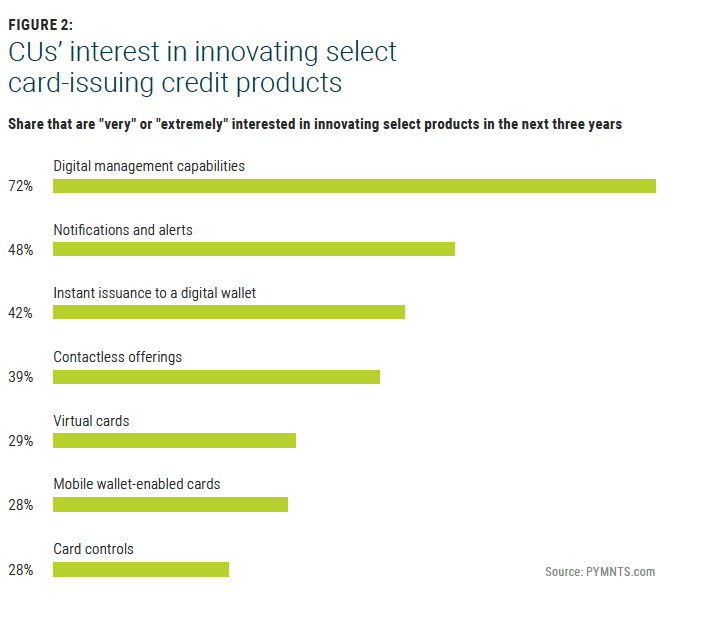

There could still be a gap between the card innovation priorities outlined by many CUs and those in which members have expressed interest, however. The Credit Union Innovation Playbook: Card Trends Edition noted that 72 percent of CU executives were “very” or “extremely” interested in providing digital management capabilities for their members before the pandemic, but just 42 percent said the same about instant issuance to a digital wallet, and 39 percent said the same about innovating contactless offerings.

Consumers’ digital priorities and preferences for contactless payment solutions have changed dramatically over the past year, however, and CUs that fail to adjust their innovation strategies could fall short on meeting existing or potential members’ expectations.

Keeping pace with members’ demands and competing with other FIs makes it imperative for CUs to innovate their digital offerings, especially as more members have come to expect seamless, contactless payment solutions. This trend shows no signs of slowing, which means that the CUs that can best tailor their card innovation strategies to satisfy members’ growing demands for contactless payments will be poised to stay one step ahead of the competition.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More