Pay by bank is no longer an unfamiliar concept in U.S. payments, but it has yet to earn a permanent place in consumers’ daily spending habits.

The payment method, which allows consumers to move money directly from their bank accounts to merchants without using cards, has reached a meaningful trial phase. A PYMNTS Intelligence report done in collaboration with Trustly finds 3 in 10 U.S. consumers have used pay by bank in the past year. Yet despite that exposure, the method still accounts for just 1.5% of all consumer retail transactions, underscoring how far adoption has to go.

Where Pay by Bank Delivers Value

At its core, pay by bank functions much like a debit card transaction. Funds move directly from a consumer’s bank account to a merchant’s account, often over real-time rails, or when unavailable, via ACH. Unlike traditional bank transfers, consumers do not share routing or account numbers with merchants. Instead, they authenticate through their bank, typically with multi-factor security, and authorize the payment.

That structure creates clear benefits for both sides of the transaction. Consumers avoid exposing sensitive account details, while merchants sidestep card network fees that are ultimately baked into retail prices. PYMNTS Intelligence notes that pay by bank effectively delivers a built-in discount by eliminating interchange and processing costs, even when merchants do not explicitly advertise savings.

Banks and FinTech providers also benefit from faster settlement, lower fraud exposure tied to stored credentials and more direct account-to-account flows. In theory, those advantages position pay by bank as a strong alternative to debit cards, especially for online transactions, subscriptions and bill payments.

Why Adoption Remains Limited

Despite those advantages, pay by bank has not crossed the threshold from occasional use to habitual behavior. The report shows usage remains concentrated in narrow categories such as monthly bills, account transfers and subscriptions. Retail and grocery spending remain largely untouched.

Security perceptions are the most significant obstacle. Nearly half of consumers who reject pay by bank believe using bank credentials is less secure than using a debit or credit card. That concern persists even though the payment method does not expose login credentials to merchants and relies on encrypted authentication through banks.

Equally important is the absence of familiar buyer protections. Consumers are accustomed to chargeback rights, liability limits and dispute mechanisms attached to cards. Pay by bank does not yet offer standardized protections comparable to those frameworks, leaving many consumers uneasy about recourse if something goes wrong.

Rewards also matter. Credit cards have trained consumers to expect tangible benefits, typically cashback or points, for everyday spending. Without comparable incentives, pay by bank struggles to compete at checkout.

A Large Persuadable Middle

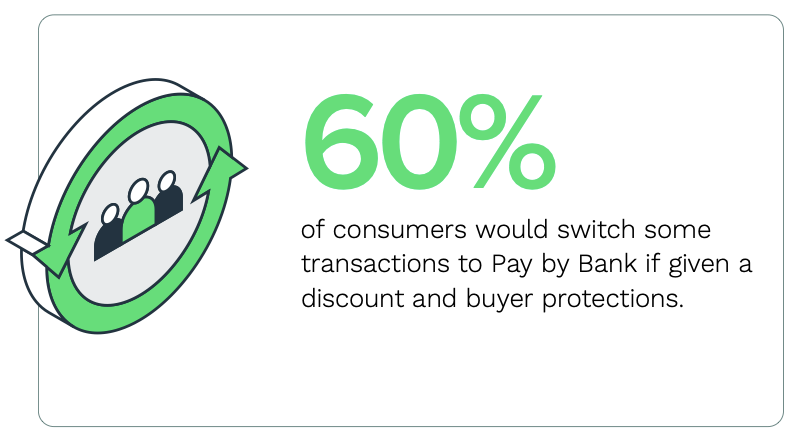

The gap between interest and usage is where the opportunity lies. The data show that 6 in 10 consumers would consider shifting some transactions to pay by bank if it offered both buyer protections and financial incentives. Among digital wallet users, that share rises to 72%, signaling a sizable audience is already comfortable with digital payments and direct account access.

The report also highlights that “immediate cash value” matters more than abstract rewards. More than 6 in 10 consumers say discounts or instant savings would make them more willing to log in to their bank accounts to pay merchants directly. Security assurances rank a close second, reinforcing that adoption hinges on trust as much as price.

What Would Move the Needle

The report outlines several clear levers to improve adoption. First is education. Many consumers are unaware that pay by bank avoids sharing account numbers and relies on bank-level authentication. Closing that knowledge gap is essential.

Second is protection. To compete with debit cards, pay by bank must incorporate clearer liability coverage, refund mechanisms and buyer guarantees that mirror what consumers already expect.

Consistency is key. Pay by bank has achieved trial but not habit. Broader availability across everyday purchase categories and seamless checkout integration are critical to turning occasional users into regular ones.

And: Incentives must feel real. Discounts, instant rebates or merchant-funded rewards tied directly to savings resonate far more than abstract promises of efficiency.

A Path Forward for Pay by Bank

Pay by bank sits at a crossroads. It can remain a niche option used primarily for bills and transfers, or it can emerge as a mainstream alternative to cards. The data suggests the latter is possible, but only if providers align the experience with consumer expectations around security, protection and value.

If those pieces fall into place, pay by bank could reshape everyday payments by lowering costs, reducing friction and strengthening trust across the ecosystem.