Banks have been facing a concerning rise in account takeover (ATO) attacks targeting their customers, with financial institutions (FIs) losses due to such schemes rising 72 percent from 2018 to 2019.

Banks have been facing a concerning rise in account takeover (ATO) attacks targeting their customers, with financial institutions (FIs) losses due to such schemes rising 72 percent from 2018 to 2019.

Fraudsters have only upped their efforts during the pandemic, with phishing attacks alone increasing 667 percent between late February and late March.

The July FI Fraud Decisioning Playbook examines how FIs are working to better detect and defend against ATOs. Relying on static usernames and passwords to authenticate customers is no longer sufficient, and many FIs are therefore examining how tools like biometrics can offer greater security.

The July FI Fraud Decisioning Playbook examines how FIs are working to better detect and defend against ATOs. Relying on static usernames and passwords to authenticate customers is no longer sufficient, and many FIs are therefore examining how tools like biometrics can offer greater security.

Around The FI Fraud Decisioning World

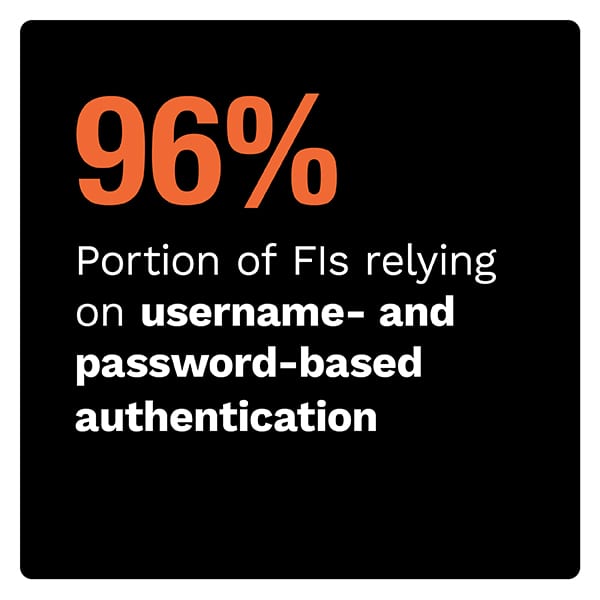

Cybercriminals have become adept at stealing customers’ usernames and passwords, details that they can then use to log in to victims’ accounts without triggering fraud alarms. A recent report highlighted this problem and advised FIs to adopt harder-to-trick methods like biometric authentication. Customers using mobile devices could scan their fingerprints on their smartphones to verify their identities.

This could be a particularly important switch as major data breaches have made it easier than ever for fraudsters to find the personal details they need to figure out customers’ logins and thwart password-based authentication measures. Breaches like those experienced by Equifax in 2017 and Capital One in 2019 may have contributed to the high prevalence of identity thefts reported in 2019, with new data revealing that such attacks comprised 20.33 percent of all fraud reported in 2019.

FIs may find that they can no longer get by relying on rules-based fraud detection systems that raise alerts when users violate certain conditions. Cybercriminals learn to adjust their behaviors just enough to avoid tripping the systems’ alarms, said Rahul Pangam, vice president of risk strategy at fraud prevention solutions provider Simility, a PayPal service, in a PYMNTS interview. Machine learning (ML)-powered tools can make fraud fighting more flexible and responsive, however.

FIs may find that they can no longer get by relying on rules-based fraud detection systems that raise alerts when users violate certain conditions. Cybercriminals learn to adjust their behaviors just enough to avoid tripping the systems’ alarms, said Rahul Pangam, vice president of risk strategy at fraud prevention solutions provider Simility, a PayPal service, in a PYMNTS interview. Machine learning (ML)-powered tools can make fraud fighting more flexible and responsive, however.

To find more about these and the rest of the latest headlines, download the Playbook.

How Combining Layered Authentication And Behind-The-Scenes Monitoring Helps Fight ATOs

Combatting ATOs requires FIs to be able to rapidly detect when fraudsters have seized control of customer accounts and to have measures ready to prevent such attacks from succeeding in the first place.

In this month’s Feature Story, Ryan Leblond, manager of fraud prevention and investigations at ESL Federal Credit Union, explores using behind-the-scenes monitoring, customer education and biometric authentication to defend against ATOs.

Read the full story in the Playbook.

Read the full story in the Playbook.

Deep Dive: How Biometric Authentication And Behavioral Analysis Detect ATOs

FIs lost 168 percent more to ATOs in 2018 than they did the prior year, and FIs need to get ahead of such crime. Modernizing authentication measures can help FIs defeat such fraud without imposing frictions on legitimate users, however.

This month’s Deep Dive examines how cybercriminals work to take over customer accounts, and how behavioral biometrics and biometric authentication enable FIs to tighten security while keeping experiences convenient for legitimate customers.

Get the scoop in the Playbook.

About The Playbook

The FI Fraud Decisioning Playbook, a PYMNTS and Simility collaboration, examines how understanding legitimate customers’ behaviors can help banks spot and eliminate malicious activities.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More