PYMNTS Innovation Investment Tracker

Here we are two months into Q3 and there are some interesting trends to observe in the FinTech investments space.

- Banking and security rule

- So do investments in retail payments

- Summer was defined by some pretty big acquisitions on both the retail and commercial payments side

The Big Takeaways for Payments and Commerce

- In August, $7.7Bn of financial activity was observed across a variety of investment types – VC funding, private placements, etc (a -52.4 percent decrease vs. the $16.1B observed in July). Of that total, $7.1Bn was driven by strategic or venture –backed investments (which is down 54.4 percent from the $15.6Bn observed in July).

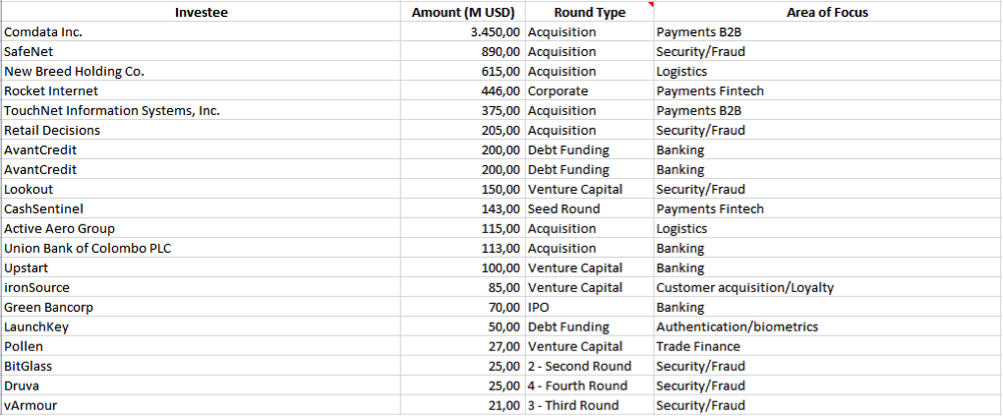

- The biggest transactions in August included the acquisition of Comdata Inc. by FleetCor Technologies Inc. for $3.5Bn and of SafeNet by Gemalto for $890 M. In July, the biggest transaction was the auction won by Blackstone of assets of Catalunya Banc for $4.8 Bn followed by the acquisiton of OneWest Bank by CIT Groupfor $3.4Bn.

- 39 percent of August’s activity was concentrated on the retail payments side(vs. 70 percent in July). 45 percent of August’s activity was in secutity/fraud while 25% was in banking. In July, 79 percent of the activity was concentrated in banking.

- On the commercial payments side the biggest investments were the stated acquistion of Comdata Inc. and of New Breed Holding Co. by XPO Logistics Inc. for $616 M. In July Lindorff acquisiton by Nordic Capital for $3.1 Bn was the biggest move followed by the acquisition of Jacobson Companies by Norbert Dentressangle for $750 Mn.

- Venture backed and strategic investments on the retail payments side accounted for $2.5 Bn of the total investment activity in August (a -77 percent decrease vs. the $10.7 Bn observed in July).

- Most of the venture and strategic backed investments on the retail payments side were in the security/fraud and banking areas accounting for 65 percent of the total. In July 78 percent of the activity was concentrated in banking.

- Venture backed and strategic investments on the commercial payments side accounted for $4.7 Bn of the total investment activity in August (a 5.1 percent decrease vs. the $4.9 Bn observed in July).

- Most of the venture and strategic backed investments were in the payments area accounting for 82 percent of the total. In July 86 percent of the activity was concentrated in Trade Finance and Logistics.

- The most active VCs included Victory Park Capital ($300 Million), Jefferies Group ($200 Million) and T. Rowe Price Associates ($150 Million). In July most active funds included Blackstone($4.8 Bn), Siris Capital ($250 Million) and Apax Partners ($84 Million).

- From a geographic perspectiveUS was the most active region (86% in August vs. 46% in July) followed byEurope ex-Russia (11% in August 53% in July).

- The median investment amount was $3.5 Million (down from $6 M in July)

The Retail and Commercial Payments Top 20 | August

Here are the top 20 investments that drove 96 percent of the funding activity in August 2014.