Thus far, it appears, American Express’ Serve hasn’t put much of a dent in Green Dot’s performance, but the prepaid market appears ripe for a good ole fashioned feud between the two companies. Although pricing has yet to play out, Amex’s low-cost proposition and free money-management tools may eventually push Green Dot to make changes. For now, however, Green Dot appears poised to compete based on its own pricing, reputation and product differentiation.

For prepaid issuers, distribution is key. But brand can also play a role in determining a product’s success, as can reputation and existing longevity in the market. Cost, however, may be a secondary factor, or at least one of the leading prepaid players in the U.S. market contends that’s the case.

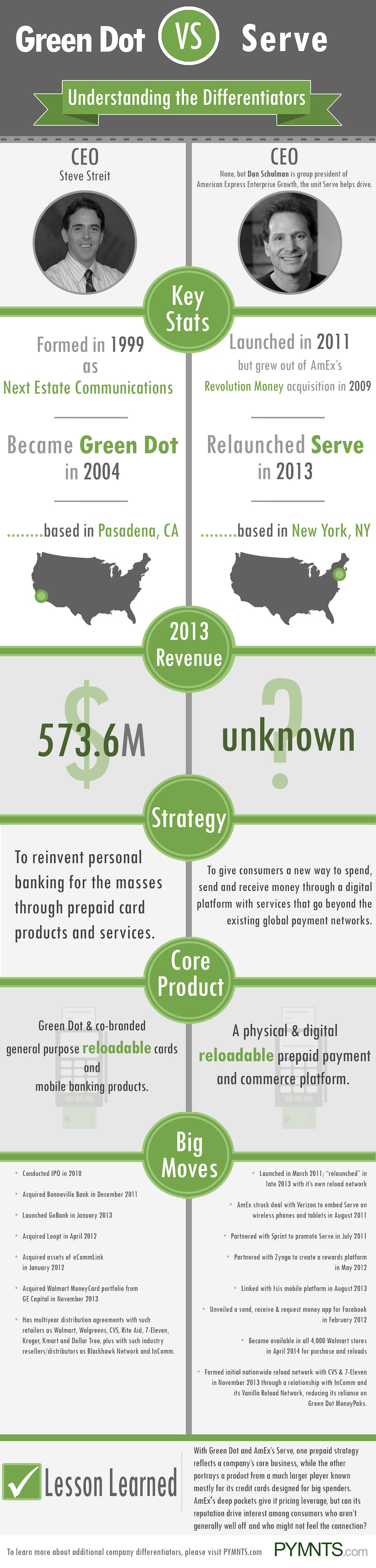

Virtually all these issues come into play for both Green Dot, a long-time player in the prepaid market, and American Express’ Serve, a relative newcomer. Serve launched three years ago and “relaunched” late last year, this time with more media spend and backed by a cross-country reload and distribution network.

Serve, now a chief growth driver for Amex’s Enterprise Growth Group, grew out of the card company’sRevolution Money acquisition in 2009. Since then, it has been building out its distribution channel. The card is now available at more than 31,000 retail locations, having added Walmart and Safeway storesearlier this year. It also expanded its cash-reload network to 27,500 locations by addingWalmart and Family Dollar retail locations.

New market

The transition to the prepaid market represented a challenging one for Amex, whose traditional customer has been the relatively wealthy credit card user. But between using its Serve platform to support a prepaid product with Walmart calledBluebird launched in 2012 while also going through other distribution channels under its own branded Serve product, Amex obviously sees prepaid as an emerging business sector where it can grow.

Amex brought Serve to market as a relatively low-cost product. Though not free, it’s pretty close. Amex waives the $1 monthly with direct deposit or with reloads of $500 or more, and it comes with free financial perks, including recently addedfinancial-management tools that allow customers to monitor their spending by automatically sorting transactions by such categories as bills, shopping and transportation. Cardholders also can create budgets, set spending limits and alerts and set and track financial goals.

Serve cards cost nothing when acquired online, and $2.95 in retail locations. Reloads are free, as are withdrawals at MoneyPass ATMs. Withdrawals at other ATMs cost $2.

Cost comparisons

Green Dot’s network-branded cards also are free when ordered online but cost up to $4.95 in retail stores. They also come with a $5.95 monthly charge that Green Dot waives with reloads up to $1,000 or when at least 30 qualifying purchases are made with the card. Direct deposit reloads are free. Otherwise, reloads cost $4.95 with Swipe Reload at the register or with a Green Dot MoneyPak. Green Dot ATM withdrawals are free at MoneyPass locations and are $2.50 elsewhere.

Serve is starting essentially from scratch, though it is showing quick progress. During the first four months of the year, Amex acquired 2.4 million customers to the Serve platform, which includes both Serve and Bluebird in the U.S. and LianLian in China, where it acquired more than 1 million customers in April alone, Amex said in announcing its financial-management tools in June. Transaction sales volume over the same period on the Serve platform was $1.9 billion, tripling the total from a year earlier and representing an annual run rate of $6 billion, Amex said.

Comparatively, gross dollar volume on Green Dot’s cards in the second quarter alone totaled $4.6 billion, up 4.5 percent $4.4 billion a year earlier. Purchase volume was $3.4 billion, up 6.3 percent from $3.2 billion. During the quarter, Green Dot expanded its Walmart relationships, including by extending its longstanding open-loop gift card contract and by entering into a new agreement to provide credit card bill-pay services at the register. In late June, Walmart began selling Green Dot-branded Everyday prepaid cards. In November last year, Green Dotacquired Walmart’s MoneyCard portfolio from GE Capital.

The introduction of a such a sizable competitor, at least in terms of what Amex brings to the table, has not been lost on Steven Streit, Green Dot’s CEO. As Green Dot’s relationship enhancements indicate, Walmart is an important customer as well for his company, as 64 percent of its product-sales revenues were derived from its stores last year. By comparison, its three other largest distributors as a group generated 22 percent of product-sales revenues, according Green Dot’s2013 annual report.

Where’s the beef?

So it’s not surprising Streit is paying close attention to Serve, and criticizing it when he has the chance.

During a recent second-quarter earnings call with investors, Streit noted that Serve has been on sale side by side with Green Dot’s products at nearly all the same places across the country. And despite Amex creating a Serve documentary and Serve benefiting from the full support of the Amex marketing machine, with “millions and millions of dollars spent on television and other media, in-store promotions, cash giveaways and more,” Streit said, Serve has seemingly “had no material impact on Green Dot’s business.”

“Serve sales are actually slowing off an already low level in one major retailer,” Streit said. “In fact, in the most recent independent third-party sales data that we received, Green Dot sales’ lead over Serve is now widening, where Green Dot products now outsell Serve by as much as 17 to 1 at one of our top five retailers where we both compete.”

Streit conceded that Green Dot only has visibility into Serve’s performance in the retail channel and that it has no reliable reporting on how Serve is performing online or through itsmobile Walmart partnership. “But I think the evidence is clear that at least in the retail channel, American Express Serve has not achieved any material traction with consumers and may actually be losing ground, while the Green Dot brand has emerged stronger than ever,” he said.

Brand over cost?

Amex also received a blow in late May, when Serve’s head of sales and business development, Thien Truong,joined Green Dot as senior vice president of sales and business development.

Streit on the call also went on to tout how brand can play a more important role than price when determining whether a prepaid product succeeds. “We believe prepaid customers don’t just want a low price in absolute terms, they demand the best value absolutely,” he said. “Like Kellogg’s in cereal, Coke in colas and Tide in detergent, Green Dot’s brand power and the values our brand represents allows us to command a fair price, even if that fair price isn’t always the lowest price.”

It’s important to note that, for all practical purposes given the lack of earlier marketing from Amex, Serve is less than a year old, while Green Dot has been around for more than a decade. So side-by-side comparisons are likely only showing minimal impact for that reason.

Momentum yet to come?

Amex executives know the strong competitive market that Serve is up against, and that is why they view Serve as a long-term growth proposition. During his company’s own second quarter earnings call, Jeffrey Campbell, Amex executive vice president and chief financial officer, indicated the company plans to be patient as it works to grow Serve.

“One long-term thing we did is, as we said for quite some time on Serve, that is a long-term proposition for us that we believe in,” he said. “And this is the first time we’ve ever really done any media spend on Serve.”

Just as drops of water won’t hurt in the short run, over time they’ll eventually sting. Whether Amex’s continued bombardment of Serve marketing will make Green Dot eventually sting remains to be seen. Expect one of the earlier results being Green Dot having to adjust its pricing to compete effectively, or vice versa if Amex’s “free” pricing isn’t sustainable.

Either way, some adjustment in pricing will likely occur. Despite Streit’s views that consumers will pay more for a better product, prepaid could quickly become a commodity. And that could affect either company’s current pricing strategy.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More