Last week, Goldman Sachs decided to open access to its once proprietary databases and risk management tools for direct use by their business clients. Bob Solomon, the CEO of Software Platform Consulting, dissects this decision and its potential to become a full-fledged business. Information may, or may not “want to be free,” but platforms definitely want their independence!

Last week’s Wall Street Journal ran an interesting article entitled “Goldman Sachs to Give Out ‘Secret Sauce’ on Trading.” The gist of the article is that Goldman is opening access to its previously proprietary databases and risk management tools for direct use by their clients.

The article points out that Goldman’s clients will now be able to use the technology to build their own trading strategies and maybe even trade independently of Goldman. The article concludes:

“But the firm’s executives believe the upside outweighs those concerns. Goldman is betting that its clients, such as hedge funds and other money managers, will use the individual applications, or apps, to develop strategies and then execute their trades with the firm. By deepening ties with those clients, Goldman hopes it will pick up other business from them as well.”

The tension between building proprietary applications and open platforms is as old as the origins of software itself, but it is a trend that has accelerated in recent years. Examples range, in rough chronological, order from:

And I need not remind you payment gurus that even the credit card networks and ATM networks began as single-bank initiatives!

These days, many folks feel that Platforms Beat Products Every Time. (This is true, in part, because it is hard to draw a fine distinction between many products and platforms. And it is not easy to define “proprietary” versus “openness.” These are all matters of degree, not binary options.) I will not try to cover that topic here; I’ll just note a couple of points in Goldman’s favor in creating an “open” platform:

As with Microsoft and the Windows platform, the platform owner makes the rules (unless the government steps in!). Goldman has to balance playing nicely with others and allowing them to create and capture value, with keeping tight control and trying to capture all of the value themselves. It’s a delicate balance. Ask the folks on the Amazon Marketplace and their third-party vendors.

If Goldman just wants to have a few applications for its existing clients to use and enhance existing relationships, no big deal – almost every bank does that these days. On the other hand, if Goldman wants to sell software, with stand-alone value, to non-Goldman clients, that goal may require a different standard and nature of application.

One thing is for certain: the further a proprietary application provider proceeds in creating a more open platform, and the more successful that platform becomes, the more gravitational forces are created that will inevitably pull that platform away from the “host” and out into the open marketplace.

Just ask SABRE, Microsoft, GXS, Ariba, and maybe AWS. All have been spun out, opened or may be setting up to do so in the case of AWS(?). On the opposite end of the spectrum, take a look at Force.com. I think of it as only moderately successful, because it is still overshadowed by an application company with grand ambitions. (Some developers are reluctant to build on a platform whose owner might compete with them!)

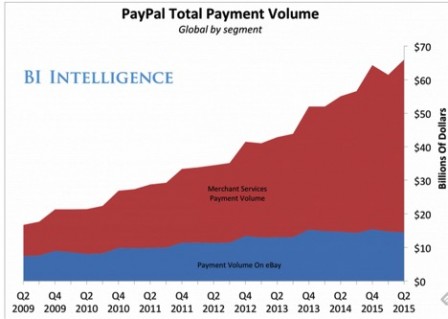

Maybe the best example of the gravitational forces associated with platforms is in the payments space: PayPal. As you know, PayPal was independent of eBay, but it was following the “remora” strategy of attaching itself to eBay users to get started. eBay tried to kill PayPal with its own application, but could not and eventually bought PayPal. Under eBay, PayPal actually lessened its dependency on the eBay Marketplace [see graphic below], but eBay still eventually split PayPal off. (Carl Icahn provided a gentle nudge.)

Bob Solomon

CEO, Software Platform Consulting

Bob Solomon is the principal of Software Platform Consulting, Inc. (SPCI). Bob helps clients develop networks and platforms that offer value to all industry participants, including their owners. Prior to founding SPCI, Bob was President of ServiceChannel, a SaaS platform in the facilities management industry. During Bob’s tenure, ServiceChannel nearly doubled in size, instituted a new business model, and dramatically improved profitability. Prior to ServiceChannel, Bob was Senior Vice President, Network and Financial Solutions for Ariba, Inc. (now part of SAP). Reporting to Ariba’s CEO, Bob was responsible for monetization of the Ariba Network, Ariba’s cloud platform for connecting Global 2000 customers to their supply bases. Bob’s team helped make the Ariba Network Ariba’s fastest growing and most profitable business.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More