The CFPB is casting a critical eye on overdraft fees charged by banks — despite facing an uncertain future in the Trump administration.

The Dodd-Frank-enabled consumer protection group has long been making noises about limiting the fees banks can charge consumers for overdrawing their accounts — and now it seems it will drop a new set of governing rules later this year.

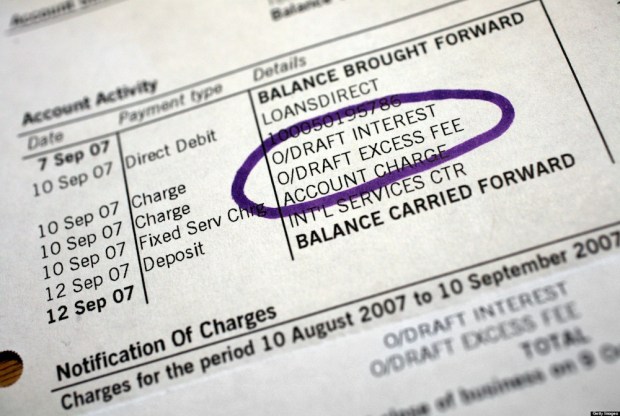

Consumer advocates have long noted that overdraft fees have quietly become a surging source of income for banks. Some observers said that revenue from overdraft fees now outpaces that from pawn shops, payday lenders and tax-refund anticipation checks put together. These advocates argued that banks have essentially found new ways to make consumers foot the bill in the face of profit-dropping low interest rates.

“[Overdrafts] allow customers to spend money they don’t have — then punish them for it,” noted Josh Reich, cofounder and CEO of Simple, an online bank based in Portland, Ore. The seven-year-old bank has never allowed account balances to go below zero and never will.

“Big banks are preying on people when they need financial help the most,” he claimed.

And some big banks have made some pretty big bucks on overdrafts.

Wells Fargo, for example, increased income from overdraft charges at more than five times the rate of its U.S. bank peers in the third quarter. And most large banks have seen overdraft revenue on the incline in recent years; charges for overdrafts amounted to $3.02 billion between July and September, up 2.4 percent since the same period last year, according to data out of FIG Partners of Atlanta.

By comparison, overdraft income at Wells was up 7.5 percent in the third quarter from a year earlier, while the other four banks making up the top five (JPMorgan Chase, Bank of America, TD Bank and US Bank) collectively saw increases in the 1.3 percent range.

Kris Dahl, a spokesperson for San Francisco-based Wells, said that Wells’ $35 overdraft fee has not changed in five years — and exists to “cover the costs associated with this service, to discourage reliance on overdrafts and to mitigate the financial risk the bank assumes when extending additional funds.”

Nick Bourke, a research director at The Pew Charitable Trusts, noted that under current regulatory rules, consumers are losing a week of pay to overdraft fees per year.

“There is a better way to do this,” he said.

However, David Pommerehn, associate general counsel for the Consumer Bankers Association lobby, noted that at present there is not a better way to do this — as the rise in overdrafting reflects consumers making heavier use of debit cards as opposed to cash and the fact that consumers simply lack options when they are struggling.

He cited a 2013 move by the Federal Deposit Insurance Corporation and the Office of the Comptroller of the Currency to tighten rules on banks offering small-dollar loans known as deposit advances — a ruling that was intended to protect consumers but that actually cut off their access to emergency funds.

“We view overdrafts as a consumer choice,” he said. “In this market, there are very few opportunities for many consumers to obtain the short-term liquidity they need.”

Plus, it remains a question mark whether the CFPB will have the power to punch it once did during the Trump administration — given the incoming president’s open and stated contempt for both the agency and the legislation that enables it, Dodd-Frank. Some are anticipating that the consumer protection agency could soon see some big changes that will “diminish meaningfully” its ability to enforce its will against big banks and their products, according to Isaac Boltansky, an analyst at Compass Point in Washington, D.C.

Still, CFPB boosters remain hopeful and encourage the agency to carry on much as it has, for as long as it can.

“This is a shadow payday lending program by the banks, dressed up in a different name,” Mike Calhoun, president of the Center for Responsible Lending, based in Durham, N.C., claimed. He further noted regulatory action is “long, long overdue.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More