Merchants have a checkout problem, and they know it. But many are unable to put their finger on how to move the needle forward in the right direction and how bad the problem really is.

And after looking at 10,000 data points over nine months, we can say that it’s not what merchants know they don’t know; it’s what they know they cannot see.

“To really optimize checkout online is hard, because we are talking about both user experience and design — somehow having a really simple checkout experience, while giving the consumer as much flexibility as they want,” Scott Fitzgerald, SVP at BlueSnap, recently told Karen Webster during a live digital discussion on this topic.

“A lot of times those two times are in conflict,” he added.

A conflict that costs merchants plenty but, Fitzgerald emphasized, that could be resolved if merchants are given a clear line of sight into the four big blind spots that get in the way of a better online — and mobile — checkout experience for their consumer and a better bottom line for themselves.

“Merchants just aren’t well-equipped to understand the root cause of abandonment.”

Insights into why a customer abandons her shopping cart or why a payment didn’t go through — checkout conversion analytics — usually aren’t at the top of the list of the types of data most payment operations or systems collect.

And why it’s challenging to fix a problem that merchants don’t know they have.

Fitzgerald reflected on the many times he’s asked a merchant what their current payment conversion rate is. He says that it’s “amazing” how few don’t have access to that data.

Lacking that information makes it hard to know whether a merchant is having a decline problem at a certain price, because of currency mismatches, or the device used to transact.

“Having that information and then being able to act on it is the difference between sales that could have gone through and hit the bottom line but instead disappeared,” he added.

Without the right data in place, merchants could also risk laying the blame of losses in the wrong places. Maybe everything is working to successfully drive traffic to an eCommerce site, but what’s getting in the way of sales is an ongoing problem with cross-border declines.

It’s not a surprise that, once retailers do get ahold of this type of payment conversion data, Fitzgerald said they don’t let go — and give their conversions a leg-up in the process.

“Large retailers often extend their existing physical POS payments provider to serve their online needs.”

The quarterly Checkout Conversion Index, coupled with deeper conversations with more than 70 retailers, shed light on a really interesting fact: Many merchants have wrongly assumed that operating in a digital world is similar enough to their existing physical environments that they can leverage their existing POS payments providers to get them to an online or mobile optimized checkout.

Let’s just call this what it is — a strategic and fatal assumption.

“Certainly, checkout is a significant part of the in-store shopping experience but rarely do you see consumers get to the front of the line, have everything in their cart scanned and bagged and then they simply walk out the door,” Fitzgerald remarked.

But online, this is happening at a staggering rate, and Fitzgerald knows why.

“In eCommerce, checkout isn’t just part of the experience; it’s, in effect, part of the product,” he explained.

The fatal mistake of thinking that online is simply a digital expansion of the physical POS misses the fact that, online, checkout is a significant piece of the experience.

“We’ve documented pretty well what the potential effect is on merchant sales if they don’t,” he emphasized.

Fitzgerald noted that this happens because physical merchants looking to grow an eCommerce footprint probably have great rates on their POS processing and want to extend that online.

But he said that it’s rare to find a provider that’s really good at handling all of the complexities at the POS, while also being really good at handling all of the complexities of eCommerce.

“I know there are folks that are trying to do it — and it’s a noble effort — but it’s a rare thing,” he added.

“Online merchants lack a checkout strategy that gets the consumer from the front door through the back door with a purchase.”

Fitzgerald observed that the reason that online checkout continues to be separated from the online product, overall, in the minds of merchants is that there simply isn’t a strategy around what that checkout experience needs to be.

Fitzgerald used this example. In meetings with merchants, he will often ask how many of them have a regular ongoing discussion about how to test, design and create the best experience possible on their site’s homepages. Not surprisingly, most of them do.

But when that same question is asked with respect to the checkout page, he said that few hands remain in the air.

His view is that that there needs to be the same amount of energy applied to both.

“Thinking about checkout with the same level of discipline and rigor around ongoing management and continuous improvement and a vision for what it could be — all of those things is what makes up a checkout strategy,” Fitzgerald said.

“And there’s not a lot of organizations we see that are really thinking about it.”

Fitzgerald also said that it’s easy to spot merchants that don’t have an online checkout strategy in place: They’ve designed a mobile website because they know it’s important and have a strategy in place, but checkout is nothing more than the existing checkout page presented in a responsive design.

“That’s when we know merchants don’t have a checkout strategy, because checkout on mobile is about more than responsive design,” he added.

What it’s about, he says, is a number of things, including a variety of payments options that can be enabled and using data capture flows that are unique to mobile versus a desktop.

That, Fitzgerald said, could also include integrating mobile wallets into the checkout product but resisting the temptation to consider a mobile wallet as the checkout strategy in and of itself.

When wallets are implemented correctly, he says that they can overcome conversion checkout problems but cautioned that it’s also important for a merchant to look at consumer demand when considering adding a mobile wallet to its checkout strategy and why adding one will help and not hurt.

“If merchants don’t have a baseline for what their checkout experience is today and what they want it to be, then whether they should add a mobile wallet or not will be up to whoever is screaming the loudest,” Fitzgerald explained, while noting that, if there is actual conversion data in place, the decision can be easier to make.

“Retailers should focus on enabling a best-in-class experience in every channel that the consumer uses to interact with them.”

Fitzgerald said merchants feel a lot of pressure to “be omnichannel,” which they interpret as two things: having a great experience for their customer, no matter how that customer wants to interact, and common data about the customer in every channel.

While those are concepts that will ultimately become table stakes in the omnichannel game, Fitzgerald noted that the problem arises when merchants believe the only way to get there is by going all in with one provider or solution — all at once.

Forgetting, he says, that it might be a better idea to deliver a best-in-class experience for each channel first. Fitzgerald believes that the race to omnichannel may be causing merchants to lose sight of the main goal: offering the highest level of experience across each and every channel.

“You’ve got to have a great experience in every channel and try to get things as consolidated as possible without compromising that,” Fitzgerald said. “Not doing that is a mistake we see people making.”

Something that Fitzgerald asserts compromises the great experience in each of those channels, which he says becomes counterproductive.

“If we all just keep to the simple penance of wanting a customer to have a great experience, no matter how they want to interact and having the data on hand to service them,” Fitzgerald said, “you can do a lot more, I think, when you think of it that simply.”

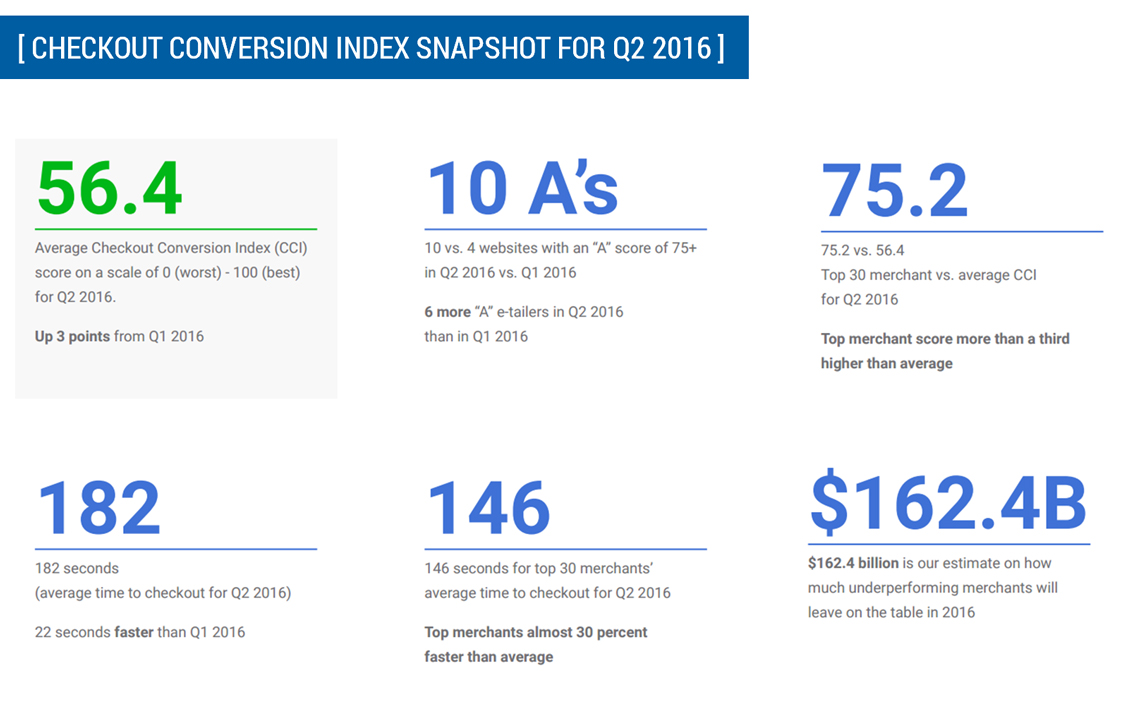

$162 billion in annual revenue.

That’s how much money underperforming merchants are leaving on the salesroom floor when they just can’t convert an online shopper to an actual buyer.

Whether it’s too many clicks, the requirement of too much information or charging way more than a shopper is willing to pay for shipping, there’s many attributes of the online checkout process that can quickly turn shoppers away in the blink of an eye.

The Checkout Conversion Index™, a PYMNTS and BlueSnap collaboration, reveals what’s causing consumers to abandon their virtual shopping carts and what merchants can do about it. The CCI measures these payment conversion problems by analyzing the digital shopper experiences of more than 650 U.S.-based eCommerce sites across 14 merchant categories.

The Q2 2016 CCI report found that big merchants still lack an online checkout strategy. Key takeaways from the latest release of the index include:

Despite the noted progress and the overall index improvement of three points to 56.4 from the first quarter of this year, the fact remains that merchants, both large and small, are still suffering from the “failure to convert.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More