Texting is ubiquitous.

Texting is, in many cases, real time — we open those digital missives almost as soon as we see them, and respond in kind.

Jon Halpern, Head of ISV at Fiserv, told Karen Webster in an interview that 98% of texts get opened once they cross our phones. And to that end, Fiserv is betting that with a device in hand, the messages that fly back and forth between customers and merchants, with payments embedded in the mix, will open up a new channel of digital commerce.

The end result, he said, will be a better end-user experience and timelier payments for merchants (who no longer have to send an invoice and hope they get paid in 30 days).

And text payments, he added, may help give rise to truly conversational commerce, the voice-activated kind.

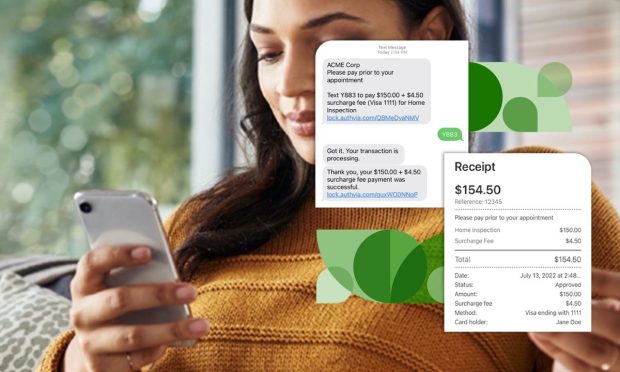

Fiserv said earlier this week that it had enabled text-to-pay functionality so that independent software vendors (ISVs) can embed those payments into their software without the need to build out their own solutions.

“We’re always trying to find ways to enable our software partners to collect payments among their merchants,” Halpern said, “in new ways that drive revenues and improve collections.”

In terms of the mechanics, the text payments and payment during chat conversation functionality is available through an application programming interface (API)-fostered integration between Fiserv’s ISV payment engine and the conversational commerce Software-as-a-Service (SaaS) firm Authvia.

At a high level, he said, invoices and bills can be sent, and payments accepted through text (using Authvia’s TXT2PAY tech) — expanding the value add that software vendors can offer merchant customers adapting to a post-pandemic, omnichannel world. The pandemic has given a tailwind to a surge in contactless payments — and TXT2PAY has seen increasing adoption across several verticals in which Fiserv’s ISV partners operate.

Asked by Webster about the initial use cases and verticals that are most obvious candidates for payments via text, Halpern noted that, in general, the services space is fertile ground — including healthcare. B2B payments, too, can be made more seamless via text-to-pay.

“But the interesting thing we’ve seen,” he said of TXT2PAY, is that the appeal goes “beyond the invoice.” A subscription firm might conceivably use TXT2PAY to collect a delinquent or failed payment — and getting paid via text can be a more effective option than trying to collect payment via email or phone.

“It’s more convenient for the merchant,” said Halpern, “because they don’t have to key in the payment information — and it’s a convenience for the consumer as well, especially if they’re a returning client off the Authvia platform — which enables you send a four digit code to authorize that payment as opposed to filling out all of your information.”

Compliance and Comfort Levels

As with any burgeoning, new payments channel — and especially a digital one where there’s no face-to-face interaction — compliance and safety are top of mind. There’s been no shortage of headlines swirling around text-based scams and spoofing.

Authvia, said Halpern, has partnered with messaging providers and phone carriers to make sure that “all the right things are being done to enable the message to come across in a way that is not ‘spam-oriented.’” He also noted that consumers are receiving those messages in conjunction with a service and from the merchants with which they are already doing business, so there is likely more inclination to allow those firms to bill and accept payments via text.

Conversational Commerce Set to Grow

TXT2PAY maintained Halpern, will help speed the evolution of conversational commerce.

We’re headed toward a future where transactions will be voice-activated, and he noted that the Authvia platform is built so that there “is some back and forth dialogue” that takes place before payments are made.

“This will continue to evolve as the technology improves,” he said. “We’re still in the early innings of integrated payments — and there’s still a lot of upside for these vertical specific software platforms to create a very tight knit experience within their software that creates a better consumer and merchant experience.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More