Mobile devices have enabled monitoring and management to a degree once thought impossible. Consumers can now get alerted to someone ringing their doorbell miles away and view video of the visitor, and can measure heart rate and steps taken daily through smartwatches. They can also see where a child or partner is using a shared credit card in real time and can even restrict usage at establishments deemed off-limits.

The latter is the power of mobile card services (MCS) which allow users to turn their cards on and off, set spending limits, restrict usage based on purchase location and receive alerts when cards are used.

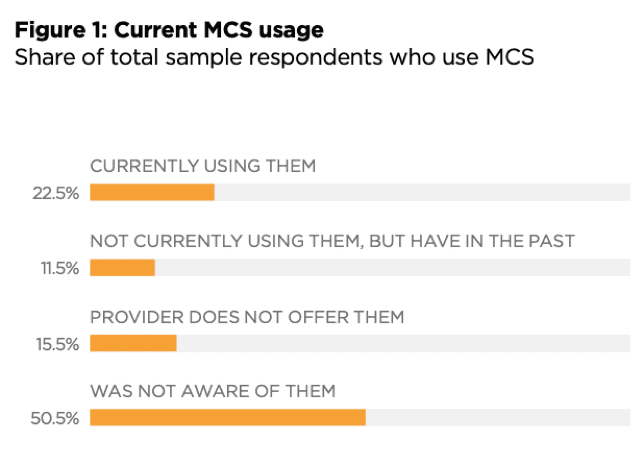

The thing is, fewer than one-quarter of consumers currently use mobile card services.

What gives?

According to the new Mobile Card Services Playbook: Driving MCS Usage Edition, low adoption appears to be an awareness issue. Half (50.5 percent) of consumers report that they have never heard of MCS.

Initially, most consumers who are interested in MCS picture using them for their primary accounts. Fifty-four percent who have never used them, but are interested, would do so in conjunction with their own cards. Fewer are interested in using MCS for a partner or child, at 18.2 percent and 8.4 percent, respectively.

When presented with tools MCS offers like card on/off controls, text alerts and spending limits, those who would use MCS with children’s accounts are “very” or “extremely” interested in an average of 5.5 controls, while those who would use them only with primary accounts are interested in four.

Vaduvur Bharghavan (VB), president and CEO of Ondot Systems, a firm offering MCS, told PYMNTS in an interview that location-based controls are by far, the most popular restriction used by customers. “It’s over 70 percent,” he said. Locations controls can provide transaction and merchant details, such as names and mapped locations.

Interest in MCS for primary cards did not vary remarkably by income. More than half (57.5 percent) of those making more than $150,000 per year and 51.8 percent of those earning under $25,000 had interest for themselves. Perhaps, not surprisingly, those with higher incomes are more likely to be interested in MCS for dependents’ accounts;15.7 percent of those making more than $150,000 per year were interested while 2.4 percent of those earning under $25,000 were.

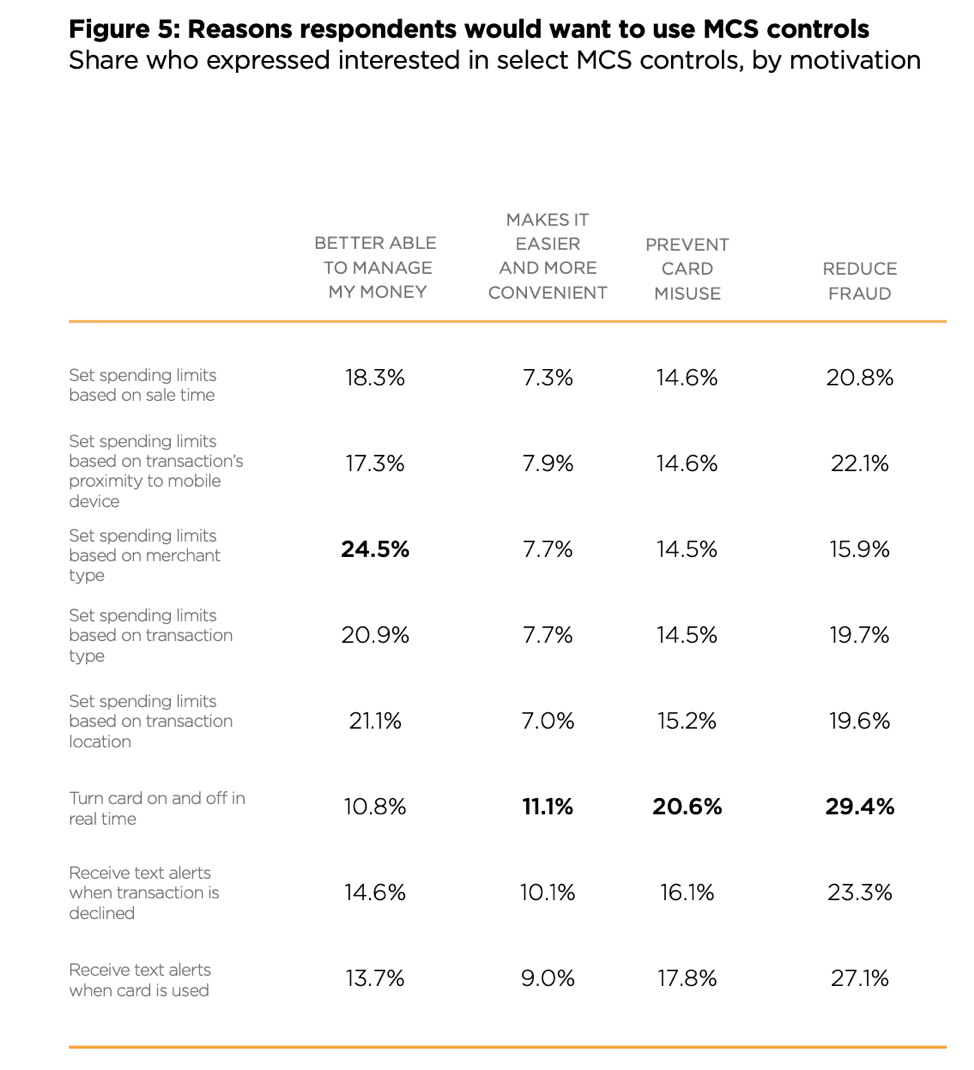

According to the study, two big reasons for consumer interest in MCS is the potential for reducing fraud risks and being able to increase spending control. Over one-quarter (29.4 percent) liked the idea of being able to turn a card on and off in real-time to prevent fraud while 20.6 percent liked this feature to prevent card misuse. There was also significant interest in setting spending limits based on merchant type to enable better money management.

The report dove deep into personas and use cases and found that middle-aged parents providing financial support for older children — likely in possession of their first credit card — were more interested in an on/off option than younger parents or seniors. Roughly one-third (31.8 percent) of those between 35 and 64 who provide financial support would use the on/off option because they believe it reduces fraud, and 22.8 percent in this group would use it to reduce risk of card misuse. Just 17.8 percent of those under 35 with dependents and 18.3 percent of those over 65 were motivated by reduced risk of card misuse.

Family circumstances and other demographic factors play a large role in how consumers envision using MCS. Purchase type is also an important factor, which makes sense considering younger consumers might spend their own money differently than they would their parents.

For example, groceries and monthly bills have far lower rates of purchase when a child is using an MCS-linked card compared to the primary user; 86.7 percent of primary users would purchase groceries using an MCS-linked card. Only 39.4 percent of children would, presumably because groceries and bills would be taken care of by the primary card user. No surprise, children using an MCS-linked card are the most likely to use it to pay for education-related expenses (26.3 percent).

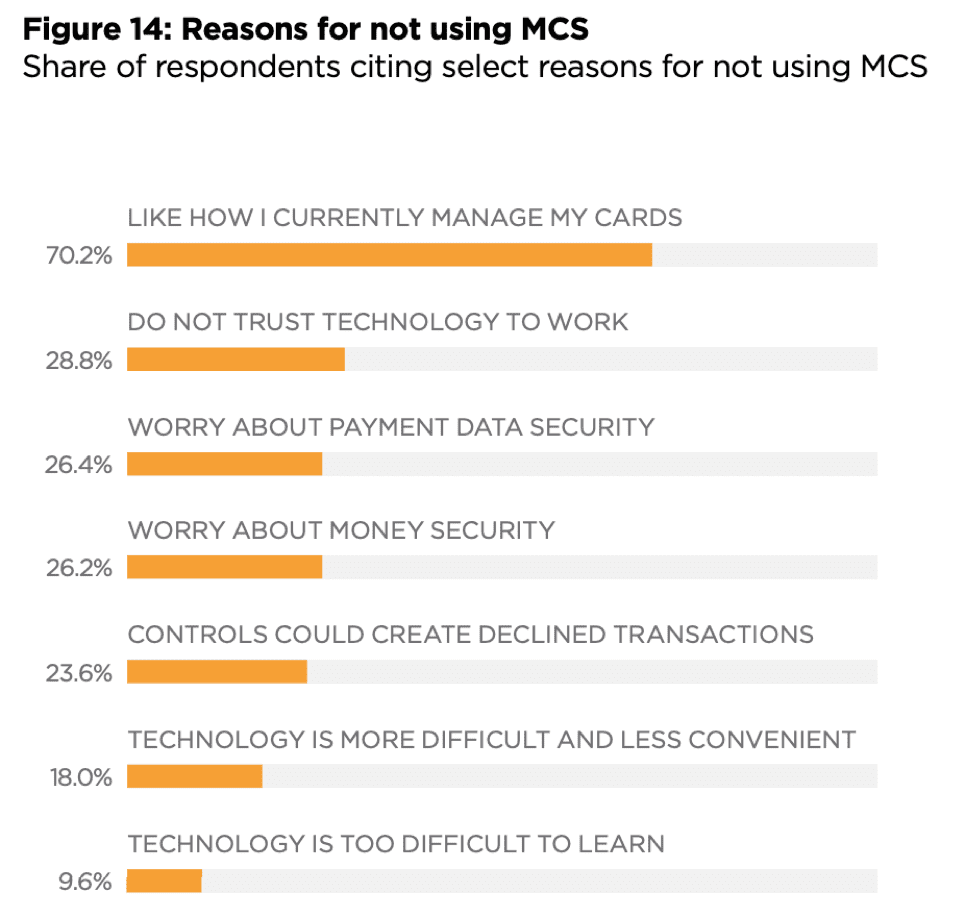

Clearly, MCS offers a great degree of control for card users, so why aren’t consumers using the services if they know about them? Mostly it’s a case of complacency and being fine with the way things have always been done. Nearly three-fourths (70.2 percent) said they did not use MCS because they like how they currently manage their cards.

Other reasons were cited by fewer than half the number of consumers who were complacent. Many were skeptical about the technology working (28.8 percent) and roughly one-quarter were concerned about data and money security.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More