Navigating through Merger Control Review in China – Challenges for U.S. Companies during a Time of Uncertainty

Navigating through Merger Control Review in China – Challenges for U.S. Companies during a Time of Uncertainty By Cheng Liu, Audrey Yumeng Li, and Jeff Liu (King Wood Mallesons)1

Escalating tensions between China and the United States (the “U.S.”) over the China-U.S. trade war since early 2018 have led to growing concerns that it may become more challenging now for deals involving US companies to obtain antitrust approval under China’s merger control regime. Under these circumstances, parties involved in a global merger almost always ask whether the China merger control review is impacted by geopolitical factors, and if not, what are the issues which may lead to greater scrutiny. This article will try to answer these questions, and offer some practical guidance for U.S. companies to better prepare for their merger filings in China during this uncertain time of China U.S. trade tensions.

Background

The China U.S. trade tensions have lasted for over 450 days.2 In the last round of tariff increases, the U.S. increased tariffs on US$200 billion worth of Chinese goods to 25% from 10% on May 20, 2019, following which China raised tariffs on US$60 billion worth of American goods from June 1, 2019. Thus far, the U.S. has already slapped tariffs on US$250 billion worth of Chinese products, and has threatened tariffs on US$325 billion more, while China has set tariffs on US$110 billion worth of US goods.3

Tensions caused by trade has started to spread to other areas. Certain Chinese telecommunications companies, including Huawai, have been under intense scrutiny in recent months. The U.S. added Huawei to its “entity list” on May 15, 2019, restricting Huawei from buying technology and parts from American firms. On the same day, the U.S. President signed an executive order prohibiting American businesses from using telecoms equipment made by companies that could pose national security risks. On May 31, 2019, the Ministry of Commerce of the PRC (“MOFCOM”) announced that China planned to establish an “unreliable entity” list which will include organizations that take discriminatory measures against Chinese local entities, cause substantial harm to relevant industries in China and pose a national security threat for China.

China and the U.S. have been engaged in economic and trade negotiations since February 2018. While it is encouraging that Chairman Xi and President Trump have agreed to restart discussions to resolve the trade conflict during the G20 summit, the direction of the trade tensions between China and the U.S. seems likely to remain uncertain at least in the short term.4

Merger Filings in China under the China-U.S. Tensions

In spite of the escalating tensions, our general observation is that no undue delay has been caused during the merger control review in China purely because of political factors or the national identity of a U.S. company. In fact, from March 22, 2018 to June 14, 2019, 96 cases involving U.S. companies, including a number of high-profile cases (e.g. Walt Disney / 21 Century Fox) have been unconditionally approved by MOFCOM (acting in the pre-SAMR period)/State Administration for Market Regulation (“SAMR”).

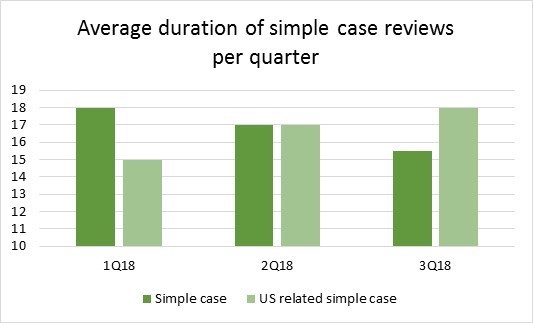

However, it is interesting to note that statistically, since the start of the China-U.S. trade tensions, the review time for transactions which involved U.S. companies has been longer than the review time for all transactions (regardless of whether U.S. companies were involved) (as shown in Graph 1 below). The reasons for the longer reviewing time are not clear – it may simply be because U.S. companies are involved in more complex transactions. However, under the background of the China U.S. trade war, it should not be a surprise if SAMR takes a more cautious attitude when reviewing transactions involving US companies, especially considering the China U.S. trade war may cause uncertainties to the market structure. For instance, if a U. S. company is proposing to acquire a Germany company, and the U.S. company is in a sensitive industry and could potentially cut off supply to the Chinese market, SAMR would need to carefully examine the potential impact of the transaction to Chinese manufactures and customers and thus take a longer time to review the transaction.

(Graph 1: Case Reviewing Time for Simplified Procedure5)

There are a number of other China-U.S. trade tension related considerations which may lead to additional uncertainty for merger filings involving US companies. One possible example is the ‘unreliable entity regime’ that the Chinese government may release soon. According to MOFCOM’s announcement, the regulator will consider the following factors when deciding if to add an entity on to the “unreliable entity list”: (a) whether the entity has enforced blockades, cut off supplies, or adopted other discriminatory measures against Chinese businesses; (b) whether that entity’s actions are based on non-commercial reasons, or in breach of any market rules and contractual terms; (c) whether the entity’s conduct has resulted in substantial harm to Chinese business or relevant industries; and (d) whether the entity’s actions constitute a threat or potential threat to China’s national security. The MOFCOM official also commented that one of the legal basis for the “unreliable entity regime” is the Anti-Monopoly Law of the PRC(“AML”). 6 If an entity involved in the transaction is on the “unreliable entity list”, it is possible that it may face more difficulties during the merger review process and thus the review would require more time.

Understand SAMR’s Particular Areas of Concerns

To better navigate China merger control reviews in such time of uncertainties, it would be important to understand SAMR’s particular areas of concerns and take them into consideration when planning filing strategies.

A. For horizontal mergers

An overview of competition concerns identified by MOFCOM/SAMR in horizontal remedies demonstrates that MOFCOM/SAMR generally examined typical theories of harm, i.e. unilateral effect and coordinated effect, which are also relied on by other antitrust enforcement agencies. However, it should be noted that in some situation, even if the parties’ combined market share is less than 30%, MOFCOM/SAMR may still raise competition concerns from a horizontal perspective. For instance, in Advanced Semiconductor Engineering, Inc.(“ASE”)/ Siliconware Precision Industries Co., Ltd. (“Siliconware”), MOFCOM imposed “hold-separate” condition even though the combined market share of the merging parties would be around 25% in the global semiconductor sealing and testing OEM service market and around 30% for the Chinese market. We understand that MOFCOM considered the oligopoly market structure in this case and the merging parties ranked first globally and in China while the other competitors have fragmented and limited market share. 7

In addition, although there remains some controversy regarding this “innovation-based” theory of harm, MOFCOM/SAMR will generally consider if the transaction will have an adverse impact on innovation where the parties have the ability to develop new products. For instance, in UTC/Rockwell Collins, SAMR concluded that “once UTC’s oxygen supply product enters the market, it will directly threaten the current market dominance of Rockwell Collins. The proposed transaction would eliminate this potential competing product and would strengthen Rockwell Collins, possibly reducing its R&D investment and motivation for commercialisation of its innovative products of the same kind ” and consequently required that the scope of divestiture would include all of UTC’s research projects on oxygen systems. 8 In Bayer/Monsanto, MOFCOM (acting in the pre-SAMR period) also emphasized that the level of innovation and R&D capacity of a party were important factors to take into account when assessing their market position.9

B. For vertical mergers and conglomerate mergers

While MOFCOM/SAMR generally recognizes that vertical and conglomerate mergers10 are less likely to have an adverse effect on competition than deals involving competitors, and in fact may produce efficiencies and be pro-competitive, they have paid special attention on the possibility of foreclosure effect that may limit the supply to Chinese companies/customers. In 2018 and 2019, as one of the few competition regulators around the globe to have imposed remedies in Essilor/Luxottica11 and KLA/Orbotech12, SAMR’s heightened scrutiny of conglomerate mergers was evident13. In fact, as early as in 2009, MOFCOM already sought to block Coca Cola’s proposed acquisition of Huiyuan based on the concern that Coca Cola would leverage its market power in the market for carbonated soft drinks to the neighbouring market for fruit juice, thereby foreclosing Chinese domestic juice manufacturers.14 In past years, MOFCOM/SAMR has imposed remedies on the ground of conglomerate effect in 8 cases , namely, Walmart/Yihaodian15, Merck/AZ Electronic16, HP/Samsung17, Essilor/Luxottica, UTC/Rockwell Collins18, KLA/Orbotech, Broadcom/Brocade19 and Shenhua/GE20. It appears that MOFCOM/SAMR has taken the view that if a party has significant market power in one product and the transaction involves a “complementary product”, the merger parties would be more likely to engage in anticompetitive bundling or tying of the products.

MOFCOM/SAMR also paid attention to interoperability, which is a quite common issue in the high-tech sector, in vertical mergers and conglomerate mergers. The interoperability theory of harm examines a situation where a dominant firm degrades product interoperability so that a product by a competitor cannot be made reasonably compatible or interoperable with readily available information. In Broadcom/Brocade21, MOFCOM considered that by having significant market power in FC switches, Broadcom may, while improving the interoperability between its own FC switches and FC adapters, refuse to improve interoperability with third-party FC adapters, thus restricting competition in the AC adapter market. Consequently, MOFCOM required Broadcom to keep the interoperability between its own FC switches and other’s FC adapters and shall not be involved in any discriminatory conducts against other’s FC adapters. Also in HP/Samsung, MOFCOM required commitment for taking no actions to bundle A4-printers with other products or to limit compatibility within third party consumables. 22

Transactions involving “Strategic” Sectors

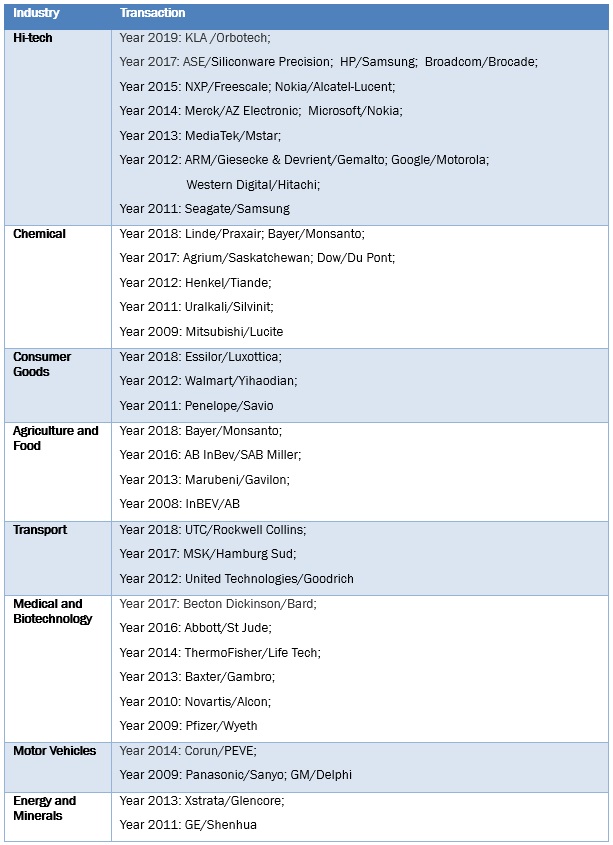

Although divergence should not be overstated, SAMR is legally obligated to consider the impact of a transaction on national economic development, the overall industry and customers during the merger review,23 which means that more uncertainties would remain if the transaction involves sectors that are strategically important or sensitive to China. From year 2008 (i.e. the effectiveness of AML), we have witnessed that MOFCOM/SAMR imposed conditional remedies in the following sectors:

(Table 1: Strategic Sectors for which Conditional Remedies are Imposed)

(Table 1: Strategic Sectors for which Conditional Remedies are Imposed)

Given the background of the China US trade war, it is likely that SAMR will continue to assess the impact of transactions involving U.S. companies on Chinese industry specifically such as in the high-tech sector. If the transaction involves a strategically important sector, it would be important to consider the impact to the Chinese industry and to understand any concerns from relevant Chinese stakeholders (e.g. customers, license users).

Although there have not yet been any actual data-related cases reviewed by MOFCOM/SAMR, we understand that SAMR is also considering and developing its related theory of harm for data-driven mergers. While there still remains a great deal of debate regarding whether data held by one party could be recognized as an essential competition element/whether to request open access to data, we have noticed that the European Commission (“EC”) and the competition regulators in the U.S. (i.e. Federal Trade Commission, “FTC” and Department of Justice “DOJ”) are paying closer attention to examining if data could trigger input foreclosure.24 The DOJ is also considering data privacy issues – if two horizontal market players compete on privacy as an aspect of product quality, their merger could be expected to reduce certain level of quality, i.e. companies in a concentrated market may tacitly coordinate to void competition on privacy. 25 With respect to China, in the latest draft Measure of Prohibition of Abuse of Dominance (draft for comment),26 SAMR has recognized that the acquisition of data can be a factor in deciding if the party has a market dominant position. Companies in relevant sectors are encouraged to monitor the legal development in China closely.

China-specific Remedies Imposed by MOFCOM/SAMR

Considering MOFCOM/SAMR’s special areas of concern, it is not surprising to see that the Chinese regulator tended to resort to a wider range of remedies to allay China-specific concerns. In general, while MOFCOM/SAMR considered structural-type remedies to the same/similar extent as U.S. regulators and the EC, it has showed a greater preference for behavioral remedies27, and the following types of behavioral remedies are quite unique for China (/not usually required in other jurisdictions):

C. FRAND commitment

Generally, a standard essential patent (“SEP”) holder would be under a FRAND commitment regardless of the proposed transaction, i.e. the SEP holders would need to make the patent available to all interested third parties, not to discriminate against different licensees, and to offer a license under fair and reasonable terms. While the EC and the FTC/DOJ usually do not consider FRAND issues to be merger-specific and take a “wait-and-see” approach (i.e. they will continue to monitor the SEP holder’s behavior after the transaction), MOFCOM/SAMR usually requires a behavioral remedy to emphasis the SEP holder’s commitment.

This approach has been seen in Google/Motorola,28 Microsoft/Nokia29 and Nokia/Alcatel-Lucent30. For instance, in Nokia/Alcatel-Lucent, MOFCOM concluded that the acquisition would strengthen Nokia’s position in the communications technology SEP market and increase the concentration on that market. In China, a majority of licensees are mobile device and wireless communications network equipment manufacturers, who do not have the leverage to cross-license with Nokia. MOFCOM found that any unreasonable changes to Nokia’s SEP licensing policy may force these businesses out of the market or pass their costs to final customers, and accordingly required FRAND commitment remedies be imposed on the merging parties.

D. Continued R&D

To address concerns regarding loss of innovation, structural remedies or behavior remedies (or a combination of both) may be required. For instance, in UTC/Rockwell Collins, SAMR required all of UTC’ research projects on oxygen systems, including all assets, IP, R&D contracts and employees participating in the research projects to be divested. More frequently than divestments, parties were requested by MOFCOM/SAMR to commit to continued R&D investment – in Seagate/Samsung31, Seagate was required to invest at least US$ 800 million a year in R&D; in Western Digital / Hitachi32 , the parties committed to an R&D expenditure and speed equivalent to those of previous year; and in UTC/Rockwell Collins, continuous R&D investment were again imposed by SAMR as a condition, including a commitment to promoting certain levels of innovation benefiting the aviation industry and aircraft platforms in China.33

E. No Tying or Bundle Sales

As mentioned above, MOFCOM/SAMR usually considers the potential of tying and/bundle sales concern for conglomerate mergers. Accordingly, a common behavioral remedy used to address these concerns is a promise not to conduct tying or bundles sales as used in UTC/Rockwell Collins34, HP/Samsung35, Broadcom/Brocade36 and Merck/ AZ Electronic. For instance, in Merck/AZ Electronic, MOFCOM requested Merck not to engage in bundling/tying between Merck’s LCD products and AZ’s photoresist products in China.

F. China specific remedies to deal with stakeholder complaints

Although not very common, we understand that to address the concerns of Chinese stakeholders, it is possible that MOFCOM/SAMR may require China specific remedies in cases where the relevant markets are considered global.

One example is imposing FRAND commitment in non-SPE related cases to ensure Chinese customers would have access to certain product/license. In Merck/AZ Electronic, MOFCOM imposed a reasonable and non-discriminatory licensing obligation to Merck for any patent it held (not limited to SEPs) in liquid crystal. In Bayer/Monsanto, MOFCOM required that the parties would need to allow all relevant Chinese App developers access to the parties’ digital platform on FRAND terms within five years’ after the parties’ digital agricultural platform comes into China. In UTC/Rockwell Collins, for the A664 terminal system chips which will be sold into China, SAMR requested the merged entity to provide the chips to Chinese customers on FRAND terms.

Another example relates to the continuation of supply/performance of existing contracts to Chinese customers. In Linde/Praxair, MOFCOM/SAMR considered the merged parties would have significant position in worldwide noble gas market post-transaction, and to protect the Chinese customer’s interest, the merged parties would need to supply noble gas to China on reasonable price and substantial volume (not less than the total suppling volume of the parties for year 2017).37 In UTC/Rockwell Collins, SAMR required to parties to continue all the contracts performed with Chinese customers, and not to change any terms or conditions contained therein.

Measure to Prepare Beforehand

In light of the above, for transactions involved U.S. companies, the parties would need to carefully prepare their filing strategies. Generally speaking, the parties would need to consider the following issues:

- Does the transaction involve any “strategic” important sector, and if yes, what impact would the transaction have on the national economy?

- Will the transaction give rise to any competition concerns, especially any particular areas of concerns recognized by SAMR?

- Are there any complaints from Chinese stakeholders? and

- Are the parties involved being investigated by Chinese regulators?

Of course the detailed filing strategy preparation would require a case-by-case analysis. Nevertheless, we have provided below some general suggestions from a technical perspective for US companies which are parties to a China merger filing:

G. Use economic analysis if necessary

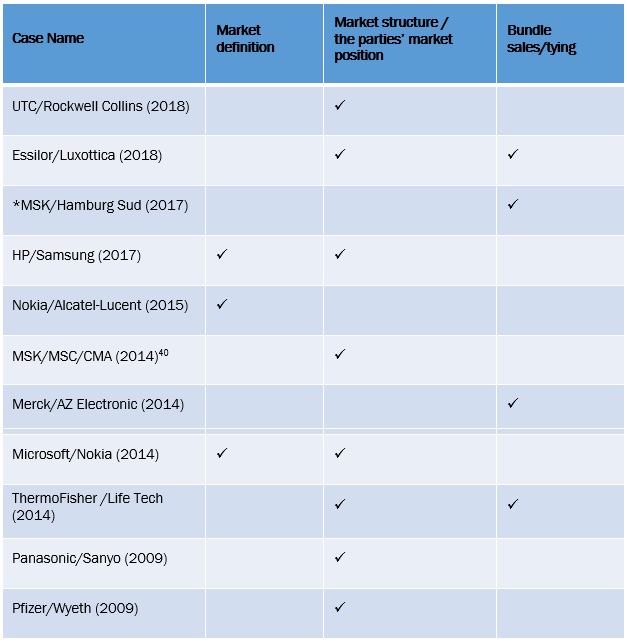

We have noticed more rigorous economic analysis has been adopted by SAMR in recent cases. For instance, in Essilor/Luxottica, SAMR carried out an extensive economic analysis to examine if Essilor has any incentive to bundle sell the glasses frames with the lens, which is a “must-have” for retailers based on market surveys in China. An official from SAMR has also publicly expressed that they will use more economic analysis in future merger control reviews. 38

We summarized the conditional decisions where economic analysis were carried out in the following table – economic analysis has been used to determine market definition (to assess substitutability between products/geographic areas), in assessing the market structure pre- and post-transaction as well as the parties’ market position, and whether the parties would have ability or incentive to engage in bundle sales or tying.39

(Table 2: Economic Analysis in Conditional Decisions)

H. Be Flexible in Offering Remedies

When designing remedy proposals, China-specific factors should be taken into consideration in the very early stages. SAMR is not only requiring China-specific remedies to address particular areas of concerns for the Chinese market, for international remedies (remedies commonly required in other jurisdictions), we have noticed that MOFCOM/SAMR may want to review the buyer of a globally divested business. For instance, in UTC/Rockwell Collins, MOFCOM required to review the buyer of the globally divested business – the parties shall sign a sale agreement and transfer the businesses to be divested within six months from the date of the announcement to buyers that meet the necessary legal requirements and after obtaining SAMR’s approval.

When designing and offering remedies, the parties would also need to be prepared to be more flexible. If commercially feasible, the parties could offer behavioral remedies (e.g. not to bundle sale or tying, or FRAND commitment) to address SAMR’s special areas of concern and to offer remedies on a voluntary basis to reduce uncertainties in the reviewing process.

In addition to the above, some general advice would include: closely engage with and maintain good relationship with SAMR, regularly update SAMR of the progress in other jurisdictions (e.g. in the EU and U.S.) and carefully devise a stakeholder outreach plan to understand customers/suppliers’ concerns.

Conclusions

To what extent a specific case could be affected by the China-U.S. trade war would require a case-by-case analysis. In the absence of competition concerns, we do not expect abnormal delay will be caused by the China-US trade war, especially considering the review process has become more transparent – since April 2019, SAMR is publishing cases granted clearance on a monthly basis and even on a two weeks basis recently.41 However, that being said, as SAMR will need to consider more factors, longer reviewing times might be required even for simple cases. For transactions which are likely to give rise to competition concerns or industry concerns, the trend of increased intervention by SAMR is likely to continue.

Click here for a pdf version of this article.

1 Cheng Liu is a partner, Audrey Yumeng Li is an associate, and Jeff Liu is a foreign legal consultant at KWM Beijing office. The authors would like to acknowledge the contribution of Lushen Hong, an associate at KWM.

2 If we counted that from March 22, 2018, on which date the U.S. president signed the memorandum to impose tariffs on Chinese products.

3 See https://www.china-briefing.com/news/the-us-china-trade-war-a-timeline/

4 See http://www.xinhuanet.com/english/2019-06/29/c_138184230_2.htm.

5 See PaRR Analytics: China antitrust approval held up US deals more than others post 1Q 18, visited at https://app.parr-global.com/intelligence/view/prime-2763653

6 http://bokeshuofa.blogchina.com/855335552.html

7 Decision No. 81 of MOFCOM’s Announcement (2017), available at http://fldj.mofcom.gov.cn/article/ztxx/201711/20171102675701.shtml

8 Decision available at http://www.cqn.com.cn/zj/content/2018-11/24/content_6502272.htm.

9 In assessing the parties’ position in Chinese non-selective herbicide market, MOFCOM considered that Bayer and Monsanto were important developers of the product. Decision No. 31 of MOFCOM’s Announcement(2018), available at http://fldj.mofcom.gov.cn/article/ztxx/201803/20180302719123.shtml.

10 Vertical mergers involve parties operating at different levels of the supply chain. In conglomerate mergers parties will generally be active in different but related markets.

11 Decision available at https://www.lawxp.com/Statute/s1819100.html.

12 SAMR Decision No. 7 of year 2019.

13 Apart from China, Essilor/Luxottica was cleared with remedies imposed in Turkey. For other jurisdictions, including European Commission (“EC”) and Federal Trade Commission of the United States (“FTC”), Essilor/Luxottica was cleared with no remedy attached.

KLA/Orbotech was cleared without any remedies imposed in any other jurisdictions (except in China) including the U.S. No filing was made to the EC regarding the transaction.

14 Decision No. 22 of MOFCOM’s Announcement (2009).

15 Decision No. 49 of MOFCOM’s Announcement (2012). No filing in EC or in U.S.

16 Decision No. 30 of MOFCOM’s Announcement (2014) No filing was made in EC and the transaction received unconditional clearance in U.S.

17 Decision No. 90 of MOFCOM’s Announcement (2011). The transaction received uconditional clearances in EC and in US.

18 No remedies to address conglomerate concerns for this transaction from EC or in US.

19 Decision No. 46 of MOFCOM’s Announcement (2017). The EC considered that the merged entity would not likely to have the ability or the incentive to engage in bundling strategies and accordingly not require any remedies in relation to bundle sales or tying; the FTC did not require remedies relevant to bundle/tying as well.

20 Decision No. 74 of MOFCOM’s Announcement (2011). No filing was made to EC or to US.

21 We notice that the EC has reached the same conclusion with MOFCOM on the interoperability issue.

22 Decision No. 90 of MOFCOM’s Announcement (2011).

23 See Article1 of the AML, which sets out the purpose of the AML includes to safeguard the interests of consumers and the public interest and to promote the healthy development of the socialist market economy. Article 1 of the AML provides that “This Law has been formulated to prevent and prohibit monopolistic acts, ensure fair market competition, improve economic efficiency, safeguard the interests of consumers and the public interest and promote the healthy development of the socialist market economy”.

24 For instance, in EC’s conditional approval regarding Microsoft/LinkedIn, and FTC’s ruling regarding WhatsApp/Facebook.

25 See https://www.cnbc.com/2019/06/11/MAKAN-DELRAHIM-SPEECH-LAYS-GROUNDWORK-FOR-ANTITRUST-VERSUS-BIG-TECH.HTML

26 http://gkml.samr.gov.cn/nsjg/bgt/201902/t20190216_288674.html

27 On the 10th Anniversary of the Implementation of China’s Antimonopoly Law (AML) in Beijing, one official from SAMR commented that the Chinese antitrust regulator has been “attaching increasing importance” to behavioural remedies in merger review. She also said that the agency would likely move to improve regulations to support, implement and supervise decisions on behavioural remedies in response to a query on the lack of regulations for behavioural remedies. See PaRR report available at https://app.parr-global.com/intelligence/view/prime-2708084

28 Decision No. 25 of MOFCOM’s Announcement(2012). MOFCOM required the merger parties to continue to observe Motorola’s FRAND commitment in relation to the SEPs they hold on mobile phones.

29 Decision No. 24 of MOFCOM’s Announcement(2014). MOFCOM required the merger parties to continue to observe their FRAND commitment in relation to their SEPs made to the SSOs.

30 Decision No. 44 of MOFCOM’s Announcement(2015).

31 Decision No. 90 of MOFCOM’s Announcement (2011), this deal was cleared by the U.S. and EU without any conditions.

32 Decision No. 41 of MOFCOM’s Announcement (2015). In this case, both FTC and EC only imposed the “hold-separate” remedy, which also formed part of MOFCOM’s conditions.

33 In this case, the DOJ and EC both imposed structure remedies through divestitures only.

34 SAMR requested that the parties shall not engage in tie-in sales or bundling or impose unfair deal terms to directly or indirectly force Chinese clients to purchase a package with bundled or tie-in products without reasonable justifications for the following six products – avionics equipment, engine nacelles, auxiliary flight control actuators, ice detection systems, power generation systems, and fire prevention system. As explained, such no tying remedy was not requested from the EC or in the U.S.

35 MOFCOM requested commitment for taking no actions to bundle A4-printers with other products.

36 MOFCOM requested Broadcom not to change any transaction terms it provides in relation to FC switches in China, and not to conduct any bundle sales or tying in any kind.

37 Decision available at https://www.lawxp.com/statute/s1822470.html

38 See http://finance.sina.com.cn/meeting/2016-11-10/doc-ifxxsmic5900228.shtml

39 * are those cases not involving U.S. companies.

40 The transaction was prohibited in China.

41 http://www.saic.gov.cn/fldj/zwgk/201905/t20190528_301492.html.

Featured News

Judge Mehta Questions Both Sides in Landmark Google Antitrust Case

May 2, 2024 by

CPI

FCC Urges Urgent Funding for Removal of Chinese Telecom Equipment from U.S. Networks

May 2, 2024 by

CPI

Former Pioneer CEO Facing Potential Criminal Charges For Colluding With OPEC

May 2, 2024 by

CPI

South Korea’s Antitrust Regulator Greenlights K-Pop Powerhouse Deal

May 2, 2024 by

CPI

Exxon’s Pioneer Purchase Approved, Former CEO Barred from Board

May 2, 2024 by

CPI

Antitrust Mix by CPI

Antitrust Chronicle® – Economics of Criminal Antitrust

Apr 19, 2024 by

CPI

Navigating Economic Expert Work in Criminal Antitrust Litigation

Apr 19, 2024 by

CPI

The Increased Importance of Economics in Cartel Cases

Apr 19, 2024 by

CPI

A Law and Economics Analysis of the Antitrust Treatment of Physician Collective Price Agreements

Apr 19, 2024 by

CPI

Information Exchange In Criminal Antitrust Cases: How Economic Testimony Can Tip The Scales

Apr 19, 2024 by

CPI