CPI Asia Column edited by Vanessa Yanhua Zhang (Global Economics Group) presents:

State of Merger Control in India – K K Sharma (KK Sharma Law Offices & ex–Director General, CCI*)

June 1, 2011 was the day India entered into the club of the countries having fully functional competition law.1 After considerable speculation, doubts, oppositions and persuasions, carrying all the stakeholders together, India finally set in place a mechanism for reviewing the acquisitions, mergers and amalgamations (called ‘combinations’ under Indian law) from the perspective of competition law. Even after having been enacted in January 2003, on account of certain legal challenges, the enforcement provisions of the Competition Act, 2002 (Act) could not be brought into force in India till as late as May 20, 2009. Even after the commencement of enforcement of provisions relating to the prohibition of anticompetitive agreements and abuse of dominant position, the opposition to the complete implementation of competition law in India did not die down. The opposition was more from domestic constituents as they saw in it another layer of Government regulation which, to the extent possible, was better kept in abeyance.

The reasons for opposing merger review regime were varied. Starting from the speculation that the CCI would be sitting over merger clearances for a long time and thus delaying business transactions, to the claims that the CCI did not have a capacity to review complex mergers being a new competition agency, all types of conjectures and surmises were being thrown around with the sole objective that a fully functional competition agency does not come to existence in India. In any case, history shows that in any jurisdiction – be it the US, Canada or EU – competition law enforcement has not been welcomed with open arms by businesses to begin with. These oppositions had their impact. Despite the competition law becoming functional as early as May 2009, it took a little more than two years for merger control to come into existence. It was of no little help that the draft merger control regulations were already prepared, in-house by the CCI, and were ready to be tested on the ground. However, the fact that the Act had certain areas in need of improvement, harmonization and, in some cases, plain typographical error removal, efforts to stall the introduction of merger review into the country succeeded. There was even talk of first amending the Act before the provisions could be brought into force.

In early 2011, good sense prevailed and the proposal of bringing in amendments before the merger control provisions could be brought into force was shelved. Instead, the logical argument that amendments only be considered if faults were found with the Act as it existed. It was the result of this changed thinking within the Government of India that a beginning towards a fully-functional competition law regime in India could be made.

The CCI finally unveiled its final draft merger regulations to the world on May 11, 2011 after consulting a wide body of stakeholders including business houses, law firms, professional associations, business and industry chambers, consumer organizations and government departments. Despite grim warnings to the contrary, June 1, 2011 came and went without any earth-shattering obstructions to the normal peaceful existence to the business enterprises; It was business as usual. On the contrary, the international antitrust community welcomed2 the performance of an Indian merger control regime.

Very soon, the CCI realized that some areas of the regime needed improvements. For example, the review machinery of CCI was avoidably clogged by a large number of intra-group merger filings, many of which did not change the control dynamics of enterprises. To ease the burden on businesses in these cases, the CCI relaxed the merger review format by amending the merger regulations so as to ensure that those merger filings that did not result in a change of control did not have to seek approval of the CCI. Similarly, the regulator noticed that harmony between the security regulator (SEBI) requirements and merger review by CCI could be further enhanced. This was done by suitably amending merger regulations. The highlights of the first amendments to the combination regulations, of February, 2012, by the CCI are as follows:

- No requirement to file for merger review if the cumulative share purchase is below 25 percent (compared to the earlier 15 percent).

- No filing requirement for intra-group mergers or amalgamations involving enterprises wholly owned by the group companies.

- Acquisitions of shares or voting rights pursuant to buy backs and acquisition of shares or voting rights pursuant to subscription of rights issue (without the restriction of their ‘entitled proportion’), not leading to acquisition of control, included in the list of transactions in Schedule I which lists transactions where a merger filing need not be made.

- The Company Secretary of the company, duly authorized by the Board, was authorized to sign Form 1 or Form 2, in addition to those persons specified under the general regulations.

- The distinction for filling up Part I for certain types of transactions and Part II for the remaining transactions was removed, leading to clarity and uniformity.

On gaining further experience, the combination regulations were amended once again by the CCI in April, 2013. The main changes were as follows:

- No notice need be filed for acquisition of shares or voting rights of companies if the acquisition is less than five percent of the shares or voting rights of the company in a financial year, where the acquirer already holds more than 25 percent but less than 50 percent of the shares or voting rights of the company.

- Where one of the enterprises had more than 50 percent shares or voting rights of the other enterprise, filing of notice with CCI for mergers/amalgamations involving these two enterprises was not needed. Similarly, if more than 50 percent shares or voting rights in each of such enterprises are held by enterprise(s) within the same group, no notice was needed.

- Some rationalization in the categories of exemption for acquisition of certain current assets like stock-in-trade, raw materials etc.

On completion, more than two years after the journey into a merger control regime began, it is the right time to look at the performance of the CCI in this vital area of competition law enforcement. When the final merger regulations were notified by the CCI, there was great excitement as well as doubts about the rules being laid down by the competition agency of India. There was a great curiosity about the CCI – especially for its capacity to deliver. Until that time, despite the commencement of provisions relating to anti-competitive agreements and abuse of dominance, the markets felt hardly any impact because of the matters before CCI. Compared to the performance of neighboring Pakistan where, right in the first 18 months of its existence, the CCP had showcased a considerable amount of work it did in exposing cartels and issuing government advisories, the performance of Indian competition agency was considered quite slow. Similarly, in another neighborly comparison, although the Act in India was enacted much earlier than China’s, China enacted and brought into force its Anti Monopoly law much earlier than India. It also started merger control with a bang and the Coca-Cola case became a selling point for antitrust law in China. Perhaps an open and vibrant democracy has a price.

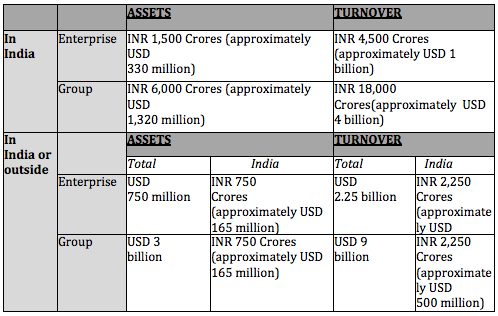

India opted for a mandatory filing regime. As of today, the thresholds for triggering the filing requirements are as follows:

As would be obvious to any discerning eye, the Indian thresholds for merger filings are extremely high – perhaps the highest in the world. Interestingly, even the default merger filing form, Form 1, is also, perhaps, the simplest in the world. After having faced the severe criticisms for having a very burdensome filing form and low thresholds, prior to the commencement of enforcement of merger control in India, these may appear to be quite stark revelations to many.

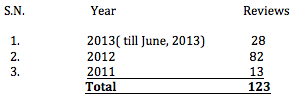

Starting from June 1, 2011, till the end of June 2013, following number of merger cases has been reviewed by the CCI:

Thus, starting from June 1, 2011 – a little more than two years since the commencement of merger review having come into force – a total of 123 cases of acquisitions, mergers and amalgamations have been reviewed by the CCI. There have been studies3 indicating the average time it takes the CCI to review a merger as just over a fortnight – which is a relatively quick merger review clearance by any standards, especially for a new agency commencing operations in the midst of questions about its effectiveness. So far, nearly all merger filings have been through the simple form – Form No 1. On account of the pressure of stakeholders, the first draft of merger regulations was made in such a way that the opponents of merger review did not get an opportunity to create unnecessary noise. The first form for merger filing was such that, effectively, it was almost discretionary to make a merger filing. This was due to the fact that even the most basic information about a transaction was to follow on the assertion of the merger-filing party that the transaction was not falling within some stated categories given in the schedule and the regulations. It was quite a big relief to businesses, but how helpful it was for competition assessment can be gauged from the fact that, despite being under no obligation to do so, nearly all the merger filings voluntarily included the details of the transaction, as well as the reason why it was not to cause an appreciable adverse effect on competition (AAEC – the substantive test for evaluation of mergers in India). Despite having a mandatory merger review regime, the first filing requirements practically gave the merger filer entire discretion on which form to choose: Form 1 or Form 2. Form 1 is minimalistic in the information sought; a large proportion of merger filings are through Form 1 only.

For all practical purposes, nearly everybody was using Form 1. The basic reason for introducing this was that any burden on business would have been used as a handle by the hawks amongst those opposing merger controls, leading to a further possible postponement of enforcement of merger control on different grounds. The cases filed through Form 2 could be counted not only on one’s fingertips, but on a single finger. These were the only cases in which some horizontal overlap amongst products and services was admitted by the parties. Prior to these cases, in no case was any horizontal overlap between products and services either admitted or claimed by the CCI during the merger review.

A look at India’s journey and progression of merger control enforcement shows a very slow movement. No doubt, the prompt clearances by the CCI, a laudable achievement, have been widely appreciated.4 However, where do we go from here? Do we have similar glowing testimonials for an in-depth analysis and incisive dissection of the issues? One possibility may be that all the cases coming before the CCI really had no competitive concerns. But if we look at the Indian thresholds, nearly the highest in the world, wherein only the big ticket acquisitions, mergers and amalgamations come under the CCI scanner, the possibility of some cases containing issues that can only be dealt with through modification cannot be ruled out, if looked at carefully. The modification mechanism (called ‘remedies’ elsewhere) has not yet been tried and tested in full. However, there is a silver lining.

Gradually, the CCI is increasing the rigor of review. Except for giving plain approvals, there are some notable exceptions where the CCI examined the agreements in detail and directed some agreements to be amended to change some of the conditions considered anti-competitive. Two cases stand out: Orchid Chemicals and Pharmaceuticals Ltd. (Combination Reg. No. C-2012/09/79), and Mylan Inc. (Combination Reg. No. C-2013/04/116). In the case of Orchid Chemicals and Pharmaceuticals, the CCI observed “non compete obligations, if deemed necessary to be incorporated, should be reasonable particularly in respect of (a) the duration over which such restraint is enforceable; and (b) the business activities, geographical areas and person(s) subject to such restraint, so as to ensure that such obligations do not result in an appreciable adverse effect on competition.”5

Similarly, in its order dated June 20, 2013, in the case of Mylan Inc. (Combination Registration No. C-2013/04/116), the CCI has accepted the modifications offered by the parties under regulation 19(2) of the combinations regulations. In both these cases, the CCI put into practice the provisions of Regulation 19(2) of the combination regulations. Under these regulations, the parties to the combination can come forward with modifications to the combinations on their own which may be accepted by the CCI. This is something similar to the undertakings in EU.

Another case stands out for comment: the notice for acquisition given by GSPC Distribution Networks Limited (“GDNL”) to acquire Gujarat Gas Company Ltd. (GGCL) (Combination Registration No.: C-2012/11/88). In this case, an undertaking was taken from GGCL to modify the agreements of GGCL with its customers. Object of this exercise is not known. This kind of action is fascinating and sometimes questionable.

The question which arises is if one party is acquiring another enterprise, what is important: the possible future conduct, or the past conduct? If an agreement being routinely entered into with its clients comes to the knowledge of the CCI during a merger filing, should the CCI start examining it in addition to the review of merger filing? In merger control, it is the counterfactual (situation where the merger has not happened) which is important for evaluating the impact of a merger on competition in the market. If counterfactual does not show any adverse impact on the competitive environment for the product under question, is it alright to get entangled in side issues? Or ideally speaking, should such cases be dealt with in a different manner? Even if some compellingly anticompetitive practice comes to notice during merger review, should it be mixed with the job at hand or dealt separately? What the CCI did in this case was to allow the merger, but accept undertakings to modify the agreements.

However, it is noteworthy that the CCI has been able to prove all of its critics wrong by ensuring that even within the country, amongst various regulatory approvals, the approval from the CCI is almost invariably the first to come. This has certainly gone down well with businesses and has helped quell negative noise about the CCI becoming another government regulator delaying business transactions and raising the cost of business. On the whole it can be said that the CCI has generally had a good start on merger review. The importance of economic analysis has been well recognised and CCI is paying enough attention to this aspect. At least 40 percent of the CCI is made up of economists. This compares well with even the most mature antitrust jurisdictions. One thing can certainly be said: the CCI is not shying away from learning from experience. Until now, two significant amendments have taken place in merger regulations, both of which aimed at ensuring a more workable and practical merger control review in India. Having travelled safely so far, we wish the CCI bon voyage ahead.

(Click here for a PDF version of the article.)

* For further details, visit www.kkslawoffices.com and the author can be reached on kksharma@kkslawoffices.com or kksharmairs@gmail.com

1 Notification dated March 4, 2011 http://www.cci.gov.in/images/media/notifications/SO479%28E%29,480%28E%29,481%28E%29,482%28E%29240611.pdf

2 http://www.ibanet.org/Article/Detail.aspx?ArticleUid=73c4fdd7-9776-41cd-8fbb-3a7dd96c8c7c

3 http://www.slashdocs.com/qispu/combination-review-in-india-a-mid-year-review-by-kk-sharma-part-1.html

4 http://www.ibanet.org/Article/Detail.aspx?ArticleUid=73c4fdd7-9776-41cd-8fbb-3a7dd96c8c7c

5 http://www.cci.gov.in/May2011/OrderOfCommission/CombinationOrders/C-2012-09-79.pdf