By Garima Sodhi,1 Sailee Sakhardande,2 & Bhaavi Agrawal3

I. Introduction

The superstructure of robust economic arguments in antitrust cases is based on an underlying foundation of market definition. Defining the relevant market is the yardstick for measuring competitive constraints faced by firms.4 In several cases, the comparison of physical characteristics, functionality, and intended use is sufficient to determine a workable relevant market and it may not require the use of more sophisticated and complex analysis. However, in certain cases, substitution is not easily discernible as it is difficult to predict the consumer’s reaction to price increases, or the market may be too complex to delineate. The Small but Significant Non-transitory Increase in Price test (“SSNIP test”) is a powerful empirical tool used by antitrust agencies all over the world to identify relevant markets.5

Implementing the SSNIP test involves estimating own and cross-price elasticities, price correlations, and factoring in characteristics of products and consumer preferences.6 Estimation of these economic parameters thus requires firm and industry-specific information over multiple years, which can be difficult to gather. For instance, official government statistics that provide information on consumer behavior may often be too aggregated for analytical purposes.7 Further, revealed preference data in terms of historical consumer behavior are more likely to be unavailable or insufficient to identify the relevant market.8

In such cases, a Stated Preference approach manifesting through a consumer survey can offer an effective way of gauging demand substitutability, which is the most important factor to be assessed while defining the relevant market. Consumer surveys are a popular tool employed by competition commissions around the world. They are not devoid of errors, but a carefully designed survey with an appropriate sample can provide reasonable insights and data to help arrive at the relevant market. The consumer survey method may be all the more useful in digital markets, given the huge complexity involved with using econometric analysis due to the presence of indirect network effects. In such a case economic analysis can be performed using qualitative data like the functionality of services, technical characteristics, and specific features of consumer demand.

In some of the recent cases before the Competition Commission of India (“CCI” or “Commission”), market definition has been a particular point of contention. A broadly defined market can by nature dilute both market shares and market power, and can reduce a dominant firm to a constrained, price-taking firm. For example, in the Mohit v. Flipkart9 case, it was contended by the online platforms that the relevant market for books be identified on the basis of genre, language, and the nature of sales, viz. consumer or institutional (CCI). A consumer survey in this case can either dispel or confirm certain contentions regarding the characteristics of different products that can make them substitutes.

In view of the above, this paper aims to examine the usefulness of the consumer survey method in defining the relevant market, particularly in the case of digital markets.

II. Literature Review

A. The Role of Consumer Surveys in Competition Analysis

The discourse on the admissibility of consumer surveys as evidence in the U.S. dates back to the twentieth century10 and the U.S. Federal Trade Commission notes the role of consumer surveys in estimating demand elasticity and their ability to control leading questions, selection bias, and randomness.11 The UK’s Office of Fair Trading stated that consumer survey evidence can be particularly useful when the competition concerns affect a large segment of the population, whose opinion may not be sufficiently captured by consulting a few members of the segment.12 It comes as no surprise then, that the UK Competition and Markets Authority has used consumer surveys in about half of its merger enquiries.13 The European Commission also uses consumer surveys on usage patterns and attitudes to consider whether two products can be regarded as substitutes, in addition to understanding their brand strength.14

Consumer surveys are a popular research tool amongst antitrust authorities on account of several important factors. For one, a stated preference survey is an effective alternative to traditional econometric tools used to assess consumer demand and delineate market boundaries.15 Further, consumer surveys can be used in the computation of Critical Loss Analysis as well as Diversion Ratios, which are conventional economic tools for market definition and merger analysis.16 For example, in the Kraft Gen. Foods case17, the Federal Trade Commission deployed consumer surveys to understand the determinants of demand for cereal such as taste, prices, and nutrition, as well as garner evidence to debunk the plaintiff’s claim of separate “adult” and “child” cereal segments.

Given the usefulness of consumer surveys in establishing market definition and carrying out merger analysis, as well as in supplementing qualitative or other documentary evidence18, it is no wonder that surveys find relevance in the complexities of digital markets. For example, in the HungryHouse and Just Eat merger case19, the UK Competition and Markets Authority supplemented the econometric analysis with market surveys to define the market as well as to obtain diversion estimates. Keeping in mind the transactional nature of the platform (i.e. the interaction between customers and restaurants), the CMA interviewed both restaurant owners as well as customers. The survey helped in clarifying how closely the merging parties competed for both restaurants and customers and the extent to which other competitors exert constraints.20

Despite their usefulness, consumer surveys have almost always been classified as “other evidence”.21 And while survey evidence is generally accepted by the courts, the variability in their acceptance as evidence by judges and lawyers means that survey evidence can be challenged vigorously in cases where they are key.22 This is because of a number of technical complexities in the execution and interpretation of surveys. For one, it can be argued that consumer behavior in practice can be different from what is stated, a phenomenon referred to as the “privacy paradox”.23 A case in point is the Lufthansa/Airholding24 merger case where Lufthansa critiqued the “switching question” for a lack of quantification of the minimum percentage of customers that should switch for the SSNIP to recognize that the Brussels and Antwerp airports were substitutes. The CMA, however, could defend its position by demonstrating that it evaluated the survey results for the switching question in tandem with responses to other questions that related to actual past behavior, which was acknowledged as a much more credible source by Lufthansa. This highlights the importance of including questions on past behavior and preferences alongside hypothetical future choices in the survey.

Another key issue is response bias (e.g. self-interest) and there is a risk that responses can systematically over or understate actual behavior depending on how the question is designed.25 For example, if asked whether a product is too expensive, it is in the interest of the consumer to answer affirmatively even if that might not be the case. In this regard, a carefully designed survey which is worded neutrally and refrains from asking agree/disagree questions when possible can be helpful.26

III. Background

We next turn to the application of consumer surveys in the Indian context. First, the Competition Act considers factors such as interchangeability or substitutability and consumer preferences while defining the relevant market.27 Thus, consumer surveys can be an effective tool in identifying products and services as weak or strong substitutes, especially in the case of digital markets where zero prices make price correlation analysis virtually impossible. Second, there is often a lack of consensus regarding the apposite market definition, with the plaintiff, the defendant, and possibly the CCI having different notions of the relevant market (See for e.g. Fast Track v. OLA case28 and RKG v. OYO29). Consumer surveys can come in handy at this point, evaluating whether products or services claimed as substitutes by various parties may indeed be deemed as such.

To examine the usefulness of consumer surveys in understanding the relevant market in India, we consider the recent abuse of dominance (“AoD”) case against Google filed with CCI.30 While the investigation spans across three distinct sections, this paper specifically addresses the market definition for applications facilitating payment through Unified Payment Interface (“UPI”). In the case of UPI payments, the informant and CCI both concurred on the relevant market as the “market for UPI enabled Digital Payment Apps in India,” while the defendant contested this market definition stating that it “ignores competitive reality, as it excludes other forms of payment that users consider to be substitutes (such as net banking, mobile wallets, and credit and debit cards).”

Against this backdrop, we designed a consumer survey that assesses the substitutability of UPI with other modes of payment and evaluates whether UPI apps can themselves constitute a market in their entirety. UPI apps are digital platforms that facilitate pecuniary transactions between senders and beneficiaries of money. A regulatory push, a Virtual Payment Address (“VPA”), and the possibility of origination across a range of other platforms including direct and instant transfer to bank accounts, have been driving the growth of UPI platforms.31 Besides, a number of third-party players and most banks have their own UPI apps which means that consumers now have more than 100 UPI applications to choose from.32

IV. Methodology

Given the nature of the market classified as “transaction markets,” it becomes important to examine factors influencing competition on both sides of the platform before coming up with a relevant market definition. Given the time constraint, however, we examine the consumer side of the UPI-enabled payment app platform and evaluate substitutability among various payment modes.

A. Objective and Target Population

The first step in survey design is the definition of a clear objective followed by identification of a target group for the survey.33 In the case of our survey, the purpose is to identify whether other modes of payments (both digital and non-digital) such as internet banking, Aadhar-based payments (payment service that allows customers to use their biometric data as identification to perform basic banking activities), mobile banking, debit and credit card transactions, as well as cash and cheques, serve as viable alternatives to UPI-based payment applications. The target population therefore are the users of both digital and non-digital payment modes throughout India.

B. Choice of Survey Questions

Meyer34, Reynolds & Walters35 as well as OECD36 provide useful guidelines in designing survey questions. To elicit meaningful responses to questions that may not always be perfectly tuned, the UK Competition and Markets Authority tries to have respondents relive their usage or purchasing decisions.37 This is achieved by asking questions which encompass four factors: matters of fact, matters of behavior, matters of choice, and matters of attitude.

Matters of fact address simple factual points and try to understand the context in which the decision was made. Matters of behavior seek to understand both the range of alternatives considered by customers and the most potent among them. The next factor considered is matters of choice, which aims to uncover the factors responsible for the choice that was eventually made. Matters of attitude usually address counterfactual scenarios of a hypothetical price increase, typically referred to as price diversion. Our survey questions follow these guidelines. Further, questions that profile the average user to understand whether a certain population segment has been over or under represented are included, such as respondent’s age, gender, internet usage, family income etc.

- Choice of Alternatives

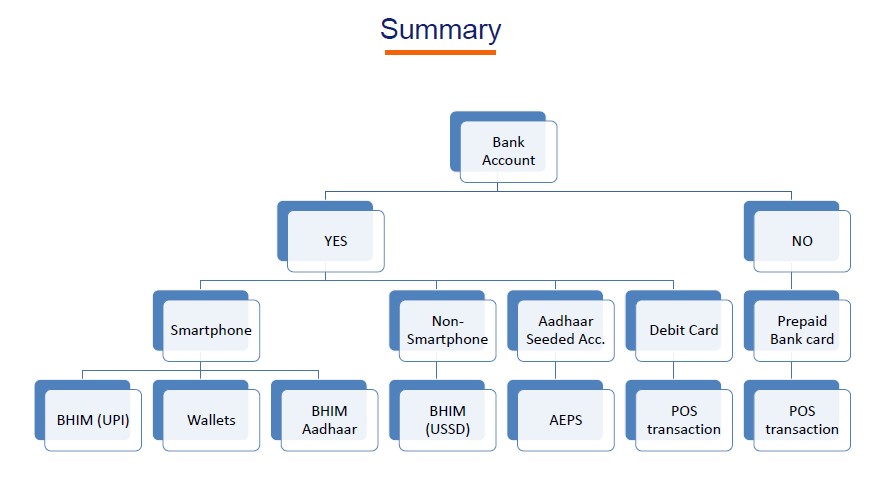

We identified an exhaustive list of digital and non-digital alternatives to UPI available to users. Cash and cheques were the most common non-digital alternatives, while digital alternatives included mobile wallets, BHIM Aaadhar, Unstructured Supplementary Service Data (“USSD”), Point of Sale (“PoS”), Bank prepaid cards, internet banking, mobile banking, credit and debit cards, micro ATMs, and the Aadhar-Enabled Payment System (“AEPS”).38 Since most digital modes and UPI in particular require the use of a smartphone, some of the options listed above do not make for credible substitutes.39 Digital alternatives for smartphone users are depicted in Figure 1 and our final list of possible substitutes thus comes down to cash, cheque, internet banking, mobile banking, mobile wallets, Aadhar payments, bank prepaid cards, and credit and debit cards.

Figure 1: Summary

Another important consideration was categorizing different types of expenditures into multiple segments and examining the use of various digital and non-digital modes of payment for that segment. This was done because consumers often employ varied modes of payment for different types of purchases. The idea behind questions 4a – 4g is thus to identify the areas where UPI apps are more likely to be used and then to further zero in on close and weak substitutes for those areas. This is facilitated by understanding the frequency of usage of various digital payment modes for each of these areas – which pans out in the form of a qualitative scale ranging from “Always” to “Never.” While calculating the average score for each question, we use a linear scale from zero to four where zero corresponds to “Never” and “Always” corresponds to a score of four.

- Addressing Bias

Based on the guidelines in OECD (2017)40 and Meyer (2007)41, we incorporate a number of factors in our survey design in order to minimize response bias. For one, we do not include any question which requires respondents to agree or disagree with a statement which can elicit confirmation bias.

Second, we have not included any questions which ask respondents for their opinion on the quality of the service or their satisfaction with the applications in their current state. This minimizes the possibility of respondents’ self-interest influencing their answers. A third key issue is the bias from differences in respondents’ behavior in real life and in their stated choices.42 Since we include a question on forced diversion, we cannot rule out the existence of such a bias. However, we corroborate the findings from the diversion question with results from questions on usage based on past behavior. Fourth, to minimize confusion, we ensured that survey questions are worded simply and neutrally.

Another important aspect that can influence responses is the length of the questionnaire and the ordering of the questions. For both these parameters, we refer to the Hungry House and Just Eat merger survey.43 The consumer survey consists of 24 questions which address consumers’ food ordering behavior, diversion scenarios, and information to profile the users followed by questions on historical usage and frequency. Our survey includes 17 questions and takes about 10 minutes to answer, which is the ideal length for a web survey.44 The survey was designed using Google Forms which ensured that the same ordering of questions and responses were recorded between November 13-20, 2020, with surveys shared through social media including LinkedIn and WhatsApp.

C. Limitations

There are a number of limitations to our survey design, as discussed below.

The first limitation is the inability to measure the response rate and thus to control for non-response bias. Since the survey was shared using social networking sites, it was not possible to identify potential respondents who saw the post with the survey but did not fill it up. The second limitation is the absence of sophisticated stratified sampling techniques that can be applied on various sub-groups, especially if such sub-groups cannot be deemed to constitute a single population.45 The third limitation is the relatively small sample size in this study. This is solely due to time and resource constraints in the context of this study and can easily be scaled up to make it commensurate with the total UPI users in India.

V. Results

The survey recorded 113 responses and after accounting for duplicates and the screening question, the final sample comprised 98 responses.

A. Respondent Characteristics

We collected basic information in the form of respondents’ age, gender, internet usage and household income to profile the average user. Our sample is 43 percent female and 57 percent male. In terms of age distribution, nearly half (46 percent) of respondents are between 25 and 34 years old followed by 24 percent of respondents between 35 and 44 years old, 17 percent between 18 and 24 years, and another 10 percent between 45 and 54 years of age. The median monthly annual income among respondents is between INR 1,50,000 and 2,00,000. Median internet usage for personal use is about 10 hours a week.

To ascertain whether respondents can differentiate between digital payments such as Aadhar-based payments, UPI transactions, and mobile wallets, we introduced a short write-up at the beginning of the survey. Respondents had to choose all the correct options based on the text from a set of four alternatives. Only 35 percent of the respondents managed to answer the question correctly, indicating that consumers are not necessarily aware of the advantages and disadvantages of the payment applications they are using.

B. Respondent Preferences

Respondents used three payment applications on average, providing strong support for multi-homing. The most popular UPI app was Google Pay with 77 percent of respondents using it, followed by Paytm with 72 percent of users and PhonePe with 29 percent. Amazon and UPI Bank Apps have a share of 22 percent each. In terms of the most preferred payment apps, Google Pay again stood first with 61 percent of users listing it among the top two digital apps, used followed by Paytm with 50 percent of users, PhonePe with 17 percent and BHIM with 7 percent. Further, an overwhelming majority of respondents could list two or more such UPI apps, which again strengthens the presence of multihoming and thus lower multihoming costs.

Further, swiftness (72 percent) and instant (55 percent) nature of transfers, as well as wider acceptance by merchants, friends, and online sites (54 percent) emerged as the main factors for usage of UPI apps. Other factors include no transaction charges (46 percent), ease of becoming a user (40 percent) and long-term usage of the app due to fewer options earlier (34 percent). Pre-installation of the app does not appear to be an important reason driving the usage of payment apps as only 10 percent of respondents chose that as the reason for their current choice of apps.

About 74 percent of respondents used an Android phone and the remaining 26 percent used an iOS device. 88 percent of Android users did not report any pre-installed payment application on their phone. Of the 12 percent (9 respondents) that answered affirmatively, six respondents (6 percent of the total sample) reported that Google Pay was pre-installed on their phone, whereas one respondent each reported that Samsung Pay, Paytm, PhonePe and MI Pay were pre-installed on their phone.

C. Historical Behavior

We use Questions 3 and 4 to understand historical usage patterns and substitutability between various modes of payment for different payment categories. Table 2 depicts the average scores for different payment modes for questions 3 and 4. Notably, the overall ranking for questions 3 and 4 is quite similar. In terms of the most used payment modes in question 3, Credit and Debit cards emerged as the first choice with an average score of 2.9, followed by UPI with a score of 2.7 and cash, which scored 2.6. Based on the linear scale where 2 denotes “Sometimes” and 3 denotes “Often,” these scores indicate frequent usage.

Table 1: Overall ranking for Questions 3 & 4

| Rank | Q3 | Q4 (a-g) | ||

| Payment Mode | Average Score | Payment Mode | Average Score | |

| 1 | Credit/DebitCards | 2.9 | Credit/DebitCards | 2.6 |

| 2 | UPI | 2.7 | UPI | 2.2 |

| 3 | Cash | 2.6 | Cash | 2.0 |

| 4 | Netbanking | 2.5 | Netbanking | 1.9 |

| 5 | Mobile Wallets | 2.2 | Mobile Wallets | 1.6 |

| 6 | Mobile Banking | 2.0 | Mobile Banking | 1.4 |

| 7 | Cheque | 1.5 | Cheque | 1.3 |

| 8 | Bank Prepaid | 1.3 | Aadhar based | 1.1 |

| 9 | Aadhar based | 1.0 | Bank Prepaid | 0.8 |

Tables 3 and 4 represent the top three payment modes for each category of payment listed in questions 4a to 4g. Our analysis indicates that UPI payments register a score greater than 2 and feature in the top three payment modes for five payments categories. More specifically, UPI emerged as the first choice for 4a) Transferring money to friends and family 4b) Paying for utilities including mobile bills, grocery bills, etc. It was the second choice for 4e) Paying for travel bookings including flights, hotels, etc. 4g) Paying for online shopping. And it ranks third in the case of 4c) Paying for services including restaurants, salon, movies, etc.

Based on the rankings, we evaluate substitutes for UPI apps by narrowing our focus to these five payment categories. Credit and debit cards, cash, internet banking, and mobile wallets thus emerge as close substitutes for UPI. For the five payment categories under consideration, modes of payment such as cheques, Aadhar based payments, and bank prepaid cards always score below 1.5 which indicates rare usage amongst respondents. Mobile banking scores 1.7 and 1.6 for 4a, and 4b respectively, while scoring below 1.5 for 4c, 4g, and 4e. However, it fails to feature in the top three payment modes for any of the payment categories and never scores above 2 which indicates less than frequent usage.

Table 2: Top payment modes

| Ranking | Q4a | Q4b | Q4c | Q4d |

| 1 | UPI | UPI | Credit & Debit Cards | Credit & Debit Cards |

| 2 | Netbanking | Credit & Debit Cards | Cash | Cash |

| 3 | Cash | Mobile Wallets | UPI | Netbanking |

Table 3: Top payment modes

| Ranking | Q4e | Q4f | Q4g |

| 1 | Credit & Debit Cards | Netbanking | Credit & Debit Cards |

| 2 | UPI | Credit & Debit Cards | UPI |

| 3 | Netbanking | Cheque | Mobile Wallets |

D. Diversion

When asked about the mode of payment that respondents would switch to due to unavailability of their most used UPI application, 34 percent of respondents said they would switch to another UPI application. This result is consistent with the finding that our respondents make use of three payment applications on average, which makes it easier to switch to other UPI applications. Further, 31 percent of respondents would switch to a different mode of payment i.e. credit or debit cards. Given that credit and debit card transactions have emerged as the most used payment method for various transactions, this result also comes as no surprise. Internet banking stood third, as a choice in the absence of UPI for 13 percent of the respondents, followed by mobile wallets and cash. These choices are consistent with the results from questions on usage patterns and choice of payment modes across a variety of transactions where credit and debit card payments, internet banking, mobile wallets, and cash rank in the top five together with UPI apps.

Table 4: Switching behavior

| Switch to: | Frequency | Percentage |

| Another UPI app | 33 | 34% |

| Credit/ debit cards | 30 | 31% |

| Internet-banking | 13 | 13% |

| Mobile wallets | 8 | 8% |

| Cash | 7 | 7% |

| Mobile banking | 4 | 4% |

| Aadhar based | 3 | 3% |

| Total | 98 | 100% |

VI. Discussion

A. Market Definition

UPI apps are digital markets characterized by the interaction between transacting parties, thus, a single market definition that includes both sides of the platform becomes necessary.46 The consumer survey employed in this study seeks to clarify market boundaries on the consumer side of the platform, which together with a survey on the merchant side of the platform can be used to identify the relevant market for UPI apps.

Our analysis of the consumer side indicates that UPI apps may not constitute a market by themselves. This assertion is supported by three different results from the consumer survey. First, UPI apps along with credit and debit cards, cash, internet banking, and mobile wallets are the most frequently used modes of transaction and together they constitute the market for “payments.” Second, credit and debit cards, cash, internet banking, and mobile wallets are equally and sometimes even more popular payment modes for transaction categories where UPI apps are one of the most preferred choices. This indicates clear substitutability between UPI apps and the aforementioned modes based on historical consumer behavior. And third, an overwhelming majority (66 percent) of UPI app users would switch to alternative modes of payment in case their most preferred UPI app becomes unavailable as against using another UPI app. This further consolidates the argument for not considering the market for UPI payments in isolation.

In terms of substitutability between UPI and other modes, credit and debit cards emerge as the strongest alternative, consistently ranking high on frequency of usage in the past year as well as for different categories of payments, often outperforming all other modes. Further, about 31 percent of users indicated that they would switch to credit and debit card payments in case their favored UPI app becomes unavailable, which comes a close second to a switch to other UPI apps (34 percent). Cash, internet banking, and mobile wallets consistently rank in the top three modes of payment that compete with UPI for the same payment categories. This supports the notion of a moderate substitution with UPI apps. In the case of Mobile banking, the evidence for substitutability is weak at best. Other evidence such as the size of SMS banking vis-a-vis UPI and recent trends in usage among smartphone users along with its substitutability on the other side of the platform i.e. for merchants should be considered before excluding it from the definition.

Our survey thus points to a product market definition that is inclusive of credit and debit card payments, cash, internet banking, and mobile wallets when considering the market for UPI apps.

B. Within UPI payments

Qualitative evidence from the survey presents a strong evidence for multihoming within the UPI universe. For one, when asked about the number of payment apps installed on their phone, users indicated that they use an average of three apps. Second, when asked to choose from a list of UPI apps that respondents used, an average user was again found to select three apps. Thus, there appear to be no or little switching costs as users tend to use more than one payment app simultaneously. Third, in our sample, while Google Pay and Paytm were used by over 70 percent of respondents, PhonePe, UPI bank apps and Amazon Pay were used by over 20 percent of respondents. This additionally supports the notion of multihoming by users. The offering of over a 100 UPI apps together with multihoming by users is indicative of strong competition amongst providers of UPI apps and lower switching costs.

Our analysis indicates that Google Pay is the most used and most preferred app among respondents, closely followed by Paytm and PhonePe which is a distant third. Data on UPI transactions however, indicates that Google Pay and PhonePe are the most popular UPI apps followed by Paytm and other UPI apps47 and thus stratified sampling may be employed in a bigger survey in order to sample UPI users commensurate with each app’s market share.

- Pre-installation and the Status-quo Bias

In the referenced Google AoD case, the informant has alleged that “by pre-installing and prominently placing Google Pay on Android smartphones at the time of initial set-up resulting in a “status-quo bias” to the detriment of other apps facilitating payments through UPI” Our survey results provide mixed evidence for the existence of such a bias. Only 10 percent of the respondents stated “pre-installed payment app” as one of the reasons for currently using it, which provides weak evidence in support of this bias. However, out of the six Android users that listed Google Pay as an app that was pre-installed on their phone, 83 percent or five respondents frequently use Google Pay and state it to be one of the most preferred apps. This lends support to the existence of a status quo bias. Since the sample size used to draw this inference is very small in this case (10 and 6 respondents respectively), a larger sample is required to conclusively confirm the existence of such a bias.

C. The SSNDQ dilemma

In digital markets with zero prices, SSNDQ tests may be considered instead of SSNIP tests which cannot be applied in this case.48 However, a number of challenges in implementing the SSNDQ test can render it unworkable.49 A major challenge is identification of the highly ranked vertical dimensions of quality.50 Further, Hartman et al proposed 25 percent decrease in a major performance quality for the SSNDQ test.51 However, differences in the nature of price and quality can make implementing the author’s proposal quite challenging.52 In the case of UPI, factors attracting consumers the most towards UPI were not clear a priori which made identifying key qualities that could be hypothetically downgraded considerably difficult.

VII. Conclusion

Digital markets characterized by network effects, switching costs and multiple sides have posed challenges to traditional market definition tools such as SSNIP tests. Consumer surveys are a popular research tool amongst antitrust authorities for defining the relevant market and have been particularly useful in the complex digital market cases. This paper takes a qualitative approach to market definition in the form of a consumer survey that evaluates the substitutability between UPI apps and other modes of payment. The survey has certain limitations due to time and resource constraints, and hence the results cannot be used conclusively for delineating the relevant market in this case, but it is indicative of a strong substitutability between UPI and other modes of payment suggesting that the relevant market in the referenced case is contestable. The survey method can, however, be easily challenged as stated preferences may be different to actual preferences, thus, requiring caution when designing and sampling.

Click here for a PDF version of the article

1 Senior Fellow, CUTS Institute for Regulation & Competition (CIRC).

2 Research Intern, CUTS Institute for Regulation & Competition (CIRC).

3 Research Associate, CUTS Institute for Regulation & Competition (CIRC).

4 Organization for Economic Co-operation and Development (2012). Roundtable on market definition. Retrieved from http://www.oecd.org/daf/competition/Marketdefinition2012.pdf.

5 Griffith, R., & Geroski, P. (2004). Identifying anti-trust markets. Edward Elgar.

6 Motta, M. (2004). Competition policy: theory and practice. Cambridge University Press.

7 Reynolds, G. and Walters, C. (2008). The use of customer surveys for market definition and the competitive assessment of horizontal mergers. Journal of Competition Law & Economics, 4(2), 411–431.

8 Meyer, C. (2007). Designing and Using Surveys to Define Relevant Markets; L. Wu (Ed.), Economics of Antitrust: Complex Issues in a Dynamic Economy (pp. 101-110).

9 CCI. Mohit Manglani v. Flipkart India Pvt. Ltd.(2015).

10 Early, W. N. (1958). The Use of Survey Evidence in Antitrust Proceedings. Wash. L. Rev. & St. BJ, 33, 380.

11 Harkrider, J. D. (2015, June 25). Operationalizing The Hypothetical Monopolist Test. Retrieved November 03, 2020, from https://www.justice.gov/atr/operationalizing-hypothetical-monopolist-test.

12 Office of Fair Trading. (2012). Price and choice in remote communities. Retrieved from: http://webarchive.nationalarchives.gov.uk/20140402142426/http:/www.oft.gov.uk/OFTwork/consultations/remote-communities/.

13 Reynolds, supra note 7 at 1.

14 European Commission. (1997). Commission notice on the definition of relevant market for the purposes of community competition law. Brussels: Official Journal of the European Communities, 372(03).

15 Meyer, supra note 8 at 1.

16 Oxera. (2008). Customer Surveys and critical loss analysis for market definition.; Oxera. (2009). Diversion ratios: why does it matter where customers go if a shop is closed?

17 York v. Kraft Gen. Foods, 926 F. Supp. 321, 359 (1995).

18 Baker, J. B., & Rubinfeld, D. L. (1999). Empirical methods in antitrust litigation: Review and critique. American Law and Economics Review, 1(1/2), 386-435; Epstein, R. J., & Rubinfeld, D. L. (2004). Effects of mergers involving differentiated products. Final Report for DG Competition, Brussels; Reynolds, supra note 7 at 1; Amelio, A., & Donath, D. (2009). Market definition in recent EC merger investigations: The role of empirical analysis. Concurrences: Revue des droits de la concurrence, 3, 1-6; DG Competition. (2010). Best practices for the submission of economic evidence and data collection in cases concerning the application of articles 101 and 102 TFEU and in merger cases.

19 Competition and Markets Authority. (2017). Just Eat and Hungryhouse.

20 Moon, N. & McHugh, S. (2017). HUNGRYHOUSE/JUST EAT MERGER INQUIRY. GfK UK Social Research.

21 Reynolds, supra note 7 at 1.

22 NERA Economic Consulting. (2010). The Use of Surveys in Litigation: Recent Trends.

23 Glasgow, G., Butler, S., & Iyengar, S. (2020). Survey response bias and the ‘privacy paradox’: evidence from a discrete choice experiment. Applied Economics Letters, 1-5.

24 Case No COMP/M. 5335-Lufthansa/SN Airholding.

25 Meyer, supra note 8 at 1.

26Organization for Economic Co-operation and Development. (2017). Methodologies for Market Studies. Retrieved from https://www.oecd.org/daf/competition/market-studies-and-competition.htm.

27 Section 2(t) & 19(7) of the Competition Act.

28 CCI. M/s Fast Track Call Cab Private Ltd. v. M/s ANI Technologies Pvt. Ltd. (2015).

29 CCI. RKG Hospitalities Pvt. Ltd. v. Oravel Stays Pvt. Ltd. (2019).

30 CCI. XYZ v. Alphabet Inc., Google LLC &Ors. (2020).

31KPMG India. (2019). Fintech in India – Powering mobile payments. Retrieved from https://assets.kpmg/content/dam/kpmg/in/pdf/2019/08/Fintech-in-India%E2%80%93Powering-mobile-payments.pdf; PwC India. (2019). Changing preferences: UPI’s dominance over digital wallets in the payments market. Retrieved from https://www.pwc.in/assets/pdfs/consulting/financial-services/fintech/point-of-view/pov-downloads/changing-preferences-upis-dominance-over-digital-wallets-in-the-payments-market.pdf.

32 Hariharan, V. (2020, January 29). UPI’s rapid growth proves India can build world-class payments infrastructure from scratch. The Print. Retrieved from https://theprint.in/.

33 OECD, supra note 26 at 4.

34 Meyer, supra note 8 at 1.

35 Reynolds, supra note 7 at 1.

36 OECD, supra note 26 at 4.

37 Reynolds, supra note 7 at 1.

38 Government of India. (n.d.). Digital Payments Methods. Retrieved from http://cashlessindia.gov.in/digital_payment_methods.html.

39 Niti Aayog, Government of India. (2016). Digital Payments: Step by Step Instructions for Various Modes of Payment-Cards, USSD, AEPS, UPI, Wallets. Retrieved from https://niti.gov.in/writereaddata/files/Step-by-step_presentation_on_digital_payments-English.pdf.

40 OECD, supra note 26 at 4.

41 Meyer, supra note 8 at 1.

42 Glasgow, supra note 23 at 4.

43 CMA, supra note 19 at 3.

44 Revilla, M., & Ochoa, C. (2017). Ideal and maximum length for a web survey. International Journal of Market Research, 59(5), 557-565.

45 OECD, supra note 26 at 4.

46 Filistrucchi, L., Geradin, D., Van Damme, E., & Affeldt, P. (2014). Market definition in two-sided markets: Theory and practice. Journal of Competition Law & Economics, 10(2), 293-339.

47 S&P Global. (2020). 2020 India Mobile Payments Market Report. Retrieved from https://www.spglobal.com/marketintelligence/en/documents/indiamobilepayments_2020finalreport.pdf.

48 Organization for Economic Co-operation and Development. (2020). Abuse of dominance in digital markets. Retrieved from www.oecd.org/competition/globalforum/abuse-of-dominance-in-digital-markets.htm.

49 Organization for Economic Co-operation and Development. (2013). The Role and Measurement of Quality in Competition Analysis. Retrieved from http://www.oecd.org/competition/Quality-in-competition-analysis-2013.pdf.

50Ezrachi, A., & Stucke, M. E. (2015). The curious case of competition and quality. Journal of Antitrust Enforcement, 3(2), 227-257.

51 Hartman, R., Teece, D., Mitchell, W., &Jorde, T. (1993). Assessing market power in regimes of rapid technological change. Industrial and Corporate Change, 2(3), 317-350.

52 OECD, supra note 48 at 16.

Featured News

Judge Mehta Questions Both Sides in Landmark Google Antitrust Case

May 2, 2024 by

CPI

FCC Urges Urgent Funding for Removal of Chinese Telecom Equipment from U.S. Networks

May 2, 2024 by

CPI

Former Pioneer CEO Facing Potential Criminal Charges For Colluding With OPEC

May 2, 2024 by

CPI

South Korea’s Antitrust Regulator Greenlights K-Pop Powerhouse Deal

May 2, 2024 by

CPI

Exxon’s Pioneer Purchase Approved, Former CEO Barred from Board

May 2, 2024 by

CPI

Antitrust Mix by CPI

Antitrust Chronicle® – Economics of Criminal Antitrust

Apr 19, 2024 by

CPI

Navigating Economic Expert Work in Criminal Antitrust Litigation

Apr 19, 2024 by

CPI

The Increased Importance of Economics in Cartel Cases

Apr 19, 2024 by

CPI

A Law and Economics Analysis of the Antitrust Treatment of Physician Collective Price Agreements

Apr 19, 2024 by

CPI

Information Exchange In Criminal Antitrust Cases: How Economic Testimony Can Tip The Scales

Apr 19, 2024 by

CPI