By Lawrence W. Abrams,[1]

On August 5, 2024, U.S. District Court for the District of Columbia Judge Amit P. Mehta ruled that Google violated Section 2 of the Sherman Act by maintaining a monopoly in general search services. Google achieved and maintained its monopoly via a series of exclusive deals spanning two decades with Apple Computer and other device manufacturers.[2] In this article, we apply market design economics to develop a “but-for” standard for the causal link between Google’s anticompetitive bidding for search engine contracts and harm to rivals and consumers.

As a matter of law, various scholars have argued that Judge Mehta’s ruling is “seriously lacking” because Judge Mehta incorrectly applied the special case “reasonably appears capable of” standard of causation instead of the default “but-for” standard of causation.[3]

We start by conceptualizing negotiations between Google and Apple as a combinational position auction, featuring a bid menu of de facto exclusive versus shared choice screen positions. We embed this market design within the canonical antitrust three-party model of vertical contracting. We make clear that this model is applicable only in cases where each of the three parties – seller, entrant, and buyer — have some market power in their relevant markets.

We argue that Google’s repeated no-bids on shared screen contracts were equivalent to anticompetitive gross overestimates of liquidated damage clauses in exclusive contract offers. By locating anticompetitive conduct early on during the competition for contract, rather than later in the effects of a contract on future competition, our market design framework offers a “but-for” causal link.

Bargaining in our model is not over price and quantity, but a share of excess profits or rent in exchange for platform positions with reduced competition. Our model assumes that bidders and the market designer consider the complex ad revenue effects of shared screen positions. As a result, we view our market design model as bringing forward Raising Rivals’ Costs (RRC) considerations during the competition for contract.

Our market design model locates anticompetitive conduct in Google’s repeated no-bids for shared choice screen contracts. Specifically, we argue that Google’s repeated no-bids in 2007, 2009, and 2012 were equivalent to grossly overestimated and anticompetitive liquidated damage clauses in exclusive contract offers. Below is a comparison of our market design framing and the court’s framing of anticompetitive causation.

I. A Market Design Framing of Causation:

Anticompetitive Conduct: “But-for” (at the competition for contract stage)

- Repeated no-bids by Google on shared position contract offers.

- Equivalent to anticompetitive liquidated damages clauses in exclusive deal offers.

- Evidence of Apple’s insistence that Google bid on shared position contracts.

Harm: (at the contract stage)

- De facto exclusive deals for search engine services.

Antitrust Violations:

- The Sherman Act, Section 1, and Section 2.

II. The Court’s Framing of Causation:

Conduct (at the contract stage):

- Google’s repeated de facto exclusive deals for search engine services involving multi-Billion-dollar revenue sharing.

Anticompetitive Harm: “Reasonably appears capable of”

- Anticompetitive denial of scale, raising rival’s costs.

Antitrust Violation:

- The Sherman Act, Section 2.

III. The Applicable Market Structure

Our market design model is applicable only in cases where each of the three parties — buyers, sellers, and entrants — have some market power in their relevant markets. In industrial organization economics terminology, our model is applicable for vertical contracting in a bilateral oligopoly. There are two to five sellers with downward sloping demand curves as their goods or services are differentiated, but substitutable. In terms of quantifying market power, we see 20% to 40% median market share as a minimum threshold. This is far below the thresholds used in Sherman Act, Section 2 monopolization cases.

The competition for contract is not over a quantity for a price, but a share of excess profits or rent in exchange for access to markets with reduced competition. The typical basis of exchange is a revenue sharing percentage, or retrospective rebates expressed as a percentage off unit list prices.

We see the market power of the sellers as coming from some sort of intellectual property that is differentiated but substitutable. Currently, we see applicability in software networks, operating systems, and electronic payment networks. Another area is preferred provider positions in healthcare networks. This includes competition for favored formulary positions managed by the “Big Three” pharmacy benefit managers (PBMs) and third-party access to electronic health record systems (EHR) owned by the “Big Three” EHR companies. Our model is applicable in antitrust cases involving two-sided platforms. However, the testimony of Apple’s Senior Vice President Eddie Cue makes it clear that Apple does not see itself fundamentally as a two-sided platform. Apple’s core business model and enviable margins are due to the outstanding quality of its devices and resulting customer brand loyalty.

The market designer in our model bears some responsibility for outcomes. Questions about Apple’s role come to the foreground when applying a market design framework to this case. Could Apple have tried harder? Did Apple not see existing contracts with Google as impediments to their own efforts at artificial intelligence (AI) native browsers? Would Apple welcome a remedy that included an injunction to end its search engine contract with Google?

These are fair questions, given the core component of Apple’s business model established by its founder Steve Jobs was never to become dependent on third-party hardware or software. Suffice it to say, a full discussion of Apple’s antitrust liability in this case is beyond the scope of this paper. Adding a market design to the three-party vertical contracting model raises difficult questions of market designer antitrust liability. This liability can run the gamut from accepting anticompetitive “first dollar” bids like bundled rebates or “cliff pricing,” to stock exchange order books favoring high-frequency traders, to PBMs’ colluding to add gross rebates as a basis in their formulary winners’ determination equation.[4]

IV. No-Bids on Shared Position Contracts as a “But-For” Causation

As described in detail in Judge Metha’s antitrust ruling, there were a series of Internet Service Agreements (ISAs) between Google and Apple naming Google the default search engine provider on Apple devices in exchange for a percentage share of keyword-linked ad revenue.[5] The ruling revealed that Apple received $20 Billion in 2022, equivalent to a 36% revenue sharing.

That was not always the case. When Google first launched its search engine services in 1999, it faced multiple competitors including Yahoo, AltaVista, Lycos, and Infoseek. In 2002, Google signed its first ISA contract with Apple. There was no exclusivity, no revenue sharing, no termination limits. In 2005, Apple first granted Google default status with a three-year term and Apple retaining unilateral rights to terminate. Initially, the 2005 contract had no revenue sharing, but it was amended to include $10 Million plus 50% of revenue share.

By 2007, bargaining power shifted to Google’s side. Evidence gathered by the court showed that Google insisted on exclusive default status, even when Apple sought greater flexibility. Google repeatedly refused Apple’s request to bid on shared position assignments in 2007, 2009, and 2012.

Coupled with the release of iOS 8 in 2014, Apple introduced its own innovative, more intelligent search called Suggestions, a nascent AI search challenger to Google’s legacy World Wide Web search. In the 2016 negotiations, Apple was so powerless that it agreed to Google’s demand to include a clause specifying that the Safari default must “remain substantially similar” to prior implementations, effectively killing Apple’s more intelligent Suggestions search. Given the 2016 Suggestions clash, we think it is rhetorical to ask the question of would Apple now welcome an injunction to end its search engine contract with Google.

In sum, our “but-for” link between Google’s bidding and exclusive deals is applicable to the 2007, 2009, and 2012 negotiations when we believed Microsoft could have garnered at least 15% of Safari’s ad revenue market. By 2016, there was no “but-for” possibility. Apple’s only option was to grant an exclusive deal to Google.

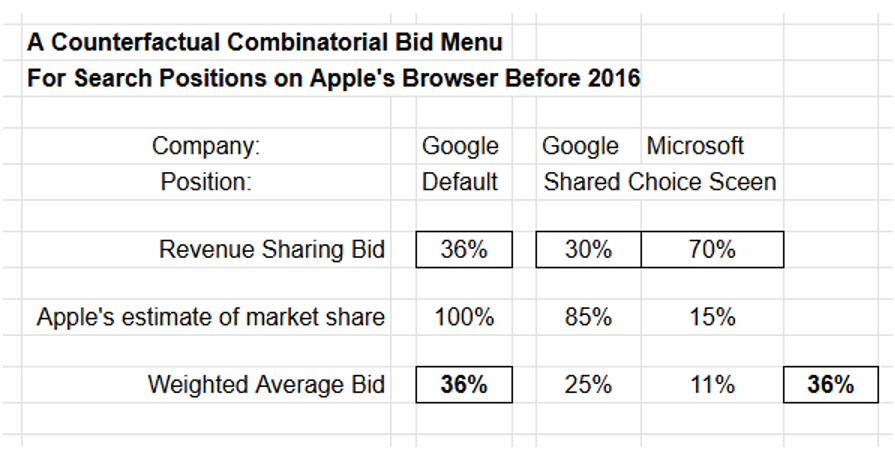

Below is a counterfactual bid menu “but-for” no-bid by Google. Google’s bid-down is from 36% to 30%. Microsoft, with a 70% revenue sharing bid and expected 15% market share, could have swung Apple’s choice to shared position contracts, especially if Apple considered the long-term benefit of keeping competition for contract alive. We strongly believe that “but-for” no-bids by Google before 2016, monopolization of the general search engine service market would have been avoided.

V. Why No-Bids for Shared Position Contracts are Anticompetitive

We now move on to show why Google’s repeated no-bids for shared position contracts were anticompetitive. We start with Aghion and Bolton’s (AB) three party model of vertical contracting presented in their often-cited 1987 paper “Contracts as Barriers to Entry.” [6] The paper represented the first theoretical answer to the Chicago School question of under what conditions would an intermediate market buyer freely enter into an exclusive deal with a seller if it were not in the best interests of itself and downstream customers.

AB viewed the difference between the seller’s and entrant’s bids as a liquidated damage estimate to be considered by the buyer when choosing among contract options. With incomplete information about the entrant’s bid, AB proved a seller, and a buyer could enter freely into a contract that was not in the best interests of downstream consumers. Truthful liquidated damage estimates promote efficient and procompetitive choices in vertical contracting.

It is here we embed the AB model with a market design. We conceptualize negotiations as a common value combinatorial position auction. It is a common value auction because bidders’ willingness to pay for favored positions is profitability as measured by percentage of revenue, a common value that both sides of this exchange can estimate.

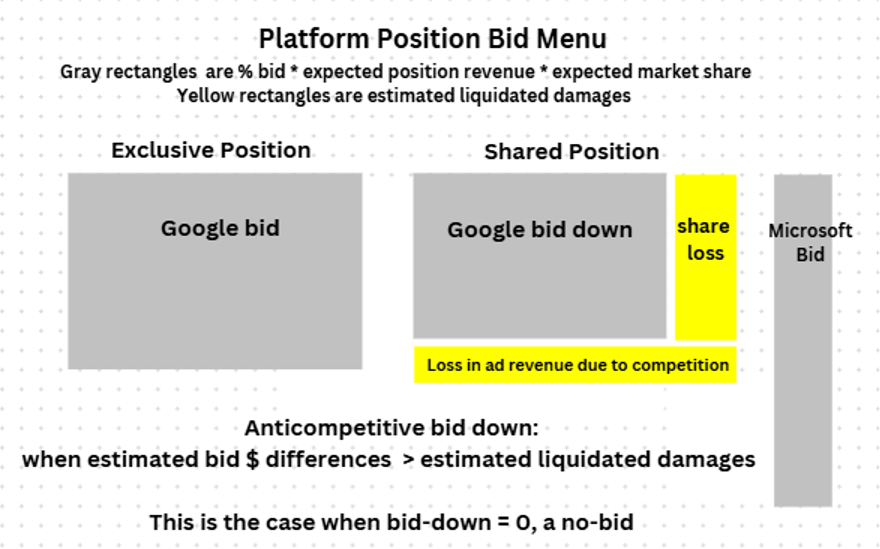

The basic rules of a combinational auction specify bid basis, bid menu and the winners’ determination equation. As in our example above, the winners’ determination equation involves comparing an exclusive bid with shared bids weighted by the market designer’s estimate of market share.

Below is an illustration of this auction design. We embed an estimated loss in ad revenue with a shared position contract due to competition for advertisers. Basically, both bidders and the market designer in our model factor in the effects of scale on profitability. .

A no-bid for a shared position contract is equivalent to a bid-down of zero in our model, clearly resulting in bid differences representing grossly overestimated liquidated damages and anticompetitive competition for contract. One takeaway from this paper is that it is problematic for a dominant supplier to have the record show a no-bid on a shared position contract offer while making a multi-Billion dollar bid on an exclusive position contract offer.

VI. Conclusion

There are benefits and drawbacks to our market design framework to antitrust cases involving vertical contracting. The drawbacks are that it is applicable in a limited number of cases and that it opens a new legal problem of market designer antitrust liability.

The benefits are that our model offers a “but-for” link between conduct and anticompetitive harm early on in competition for contract. The lower threshold for market power allows cases to be filed under Sherman Act, Section 1 as well as Section 2. Anticompetitive conduct is quantifiable.

Click here for a PDF version of this article

[1] There are no relevant disclosures pertinent to this piece. I have received no compensation or benefits from any party. I have a Ph.D. in Economics from Washington University in St. Louis and a B.A. in Economics from Amherst College.

[2] United States, et al. v. Google, LLC, No. 20-cv-3010 (APM) (D.D.C. Aug. 5, 2024), Dkt. No. 1033. https://storage.courtlistener.com/recap/gov.uscourts.dcd.223205/gov.uscourts.dcd.223205.1033.0_1.pdf.

[3] Manne, Geoffrey. A, A Critical Analysis of the Google Search Antitrust Decision, ICLE White Paper 2024-08-14 https://laweconcenter.org/wp-content/uploads/2024/08/Manne-Google-Search-Decision-Analysis-2024-08-14.pdf.

[4] United States, et al. v. Google, LLC, 108 – 114

[5] Abrams, Lawrence W., A Discovery Plan for Pharmacy Benefit Managers Collusion, Competitive Policy International – Pricing, January 20, 2025. https://www.pymnts.com/cpi-posts/a-discovery-plan-for-pharmacy-benefit-managers-collusion/.

[6] Aghion, P., & P. Bolton. 1987. Contracts as a Barrier to Entry, American Economic Review, 77(3): 388–401. https://business.columbia.edu/sites/default/files-efs/pubfiles/2018/contracts%20a%20barrier%20too%20entry.pdf.