In the U.S., millions of people remain underserved and underrepresented by credit scoring models that are deemed reliable yet cloak a population that could be especially attractive to lenders – including significant numbers of minorities who are underserved.

A recent white paper from FICO’s main competitor VantageScore Solutions titled “Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial?” addresses the need to challenge “every core assumption” of traditional scoring models. According to VantageScore, the latest iteration of its model, VantageScore 3.0, can accurately generate a credit score for millions of Americans that conventional credit scoring models ignore.

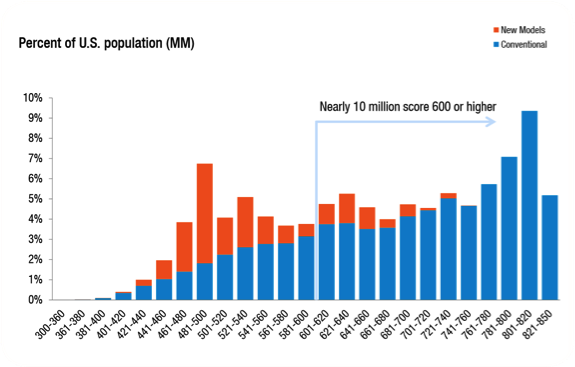

Among VantageScore’s conclusions: As many as 30 million-35 million American consumers, flying under the radar of traditional scoring metrics can have an accurate credit score and are now able to become visible and attractive customers to lenders. Many of these consumers have scores of 600 and above.

Source: VantageScore 3.0, “Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial?”

The latest VantageScore model accomplishes this by using a broader and deeper set of credit file data as well as more advanced modeling techniques. This allows the VantageScore model to capture unique consumer behaviors more accurately.

In the white paper, the conventionally unscoreable consumer universe is segmented into several criteria including four unique groups of behavior: “New to market,” wherein trades are less than six months old; “infrequent users,” where no trade has been updated in six months; the “rare credit” user, who has no activity on file through the past two years and finally, “no trades.”

VantageScore notes in the paper that the score associated with these consumers is highly accurate as demonstrated by a comparison of actual first year default rates among both the conventional and newly scored populations.

In addition, anonymous consumer credit data was compiled and aligned with Zip Code Information. That process sought to uncover whether a meaningful percentage of minority consumers might be “inadvertently” excluded from conventional scoring models, simply because they fail to consistently meet the minimum criteria currently in place with conventional credit risk scoring models.

From a fair lending perspective, 9.5 million Hispanic or African American consumers are additionally scored by VantageScore 3.0. — and 2.7 million of these consumers score above 600.

The white paper findings include data that shows about 7 percent of Hispanics fall under the rubric of infrequent credit users, and another 4 percent can be seen as rare credit users. Those numbers are similar in the African American population, as 7 percent of those users are marked by infrequent activity. Another 3 percent can be deemed rare credit users.

However, according to VantageScore, those populations may finally gain access to credit – and even escape predatory lenders — once lenders truly embrace “state of the art” risk scoring models that go beyond the “traditional” norms.

[gview file=”http://www.pymnts.com/wp-content/uploads/2015/06/VantageScore-Whitepaper-Universe-Expansion-20151.pdf”]

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More