The CE100TM Index: A New Equity Index of 100 Publicly Traded Companies for Tracking the Digital Transformation and the Growth of the Connected Economy Methodological Appendix

To track the digital transformation and the growth of the connected economy, PYMNTS has developed an equity index based on 100 companies likely to be key players in its evolution. The Connected Economy 100 (CE100TM Index) is an equal-weighted equity index of 100 companies that represent 11 key components of the connected economy. Work on the CE100 Index TM began in April 2020 as part of a series of related research projects on the connected economy and culminated in the final selection of companies in May 2021.

SELECTION OF COMPANIES

The companies were selected based on the following methodology.

First, based on our extensive research, including surveys of thousands of consumers, we decomposed the connected economy into 10 “pillars” that involve relatively distinct ways in which consumers’ lives are being affected by the digital transformation.

While these categories provide a helpful organizational framework, our research found that companies are forging connections across pillars and this increasing interconnectedness across sectors is driving the overall growth of the digital economy. We also have identified an eleventh category of enabling technologies (Enablers), such as cellular and operating systems, that provide a foundation for these pillars. As with any classification there are gray areas, and we relied on our extensive industry expertise to make judgment calls on how to categorize these.

Second, for each of the 11 categories (10 pillars plus the enablers) we selected companies based on the following four criteria:

We did not consider the historical performance or market capitalization of candidate companies. The selections were made by Karen Webster based on her deep knowledge from researching the connected economy over the last decade, including interviews with more than 700 CEOs and C-Suite executives since 2019, and basic research conducted by the PYMNTS data analytics team. The results were a list of 140 candidate companies. Other senior members of the PYMNTS team reviewed the initial choices, leading to several iterations of the list.

Third, we recruited a group of eight highly experienced investors, primarily from venture capital and private equity firms, and asked them to identify companies based on the four criteria above for each pillar with which they were familiar. To ensure they provided independent input, we did not share our initial list. Many of their choices were the same as ours. Some were different and led to replacing our initial choices with their selections. In a small number of cases, we rejected recommendations from one or more advisors in favor of our own choices informed by our research.

We then narrowed the list to 100 firms. To ensure representation across categories we selected at least three and no more than 15 companies as the enablers and each of the 10 pillars based on the depth of participation in those categories. The CE100 Index, therefore, is based on a stratified sample of companies across the 11 categories with oversampling of nascent sparsely populated categories. This feature is important for making the CE100 Index representative of the dynamic growth of the connected economy.

The final list of 100 companies includes a wide diversity of firms, ranging from mature, traditionally non-digital firms that are making significant inroads into digital businesses to venture-backed, digital-only firms that recently have gone public. It includes firms that participate in multiple pillars of the connected economy as well as firms that are narrowly focused. The median market cap of the members of the list is $46 billion as of Feb. 4, 2022, with a range from $1.5 billion to $2.8 trillion. Of the 100 companies, 39 firms are listed on the Nasdaq, 53 on the NYSE, 3 on the OTC and 5 on foreign exchanges.

Table 1 shows the number of firms in each of the 11 categories, with category allocation based on each firm’s most significant digital capability.

CALCULATING AND UPDATING THE CE100TM INDEX

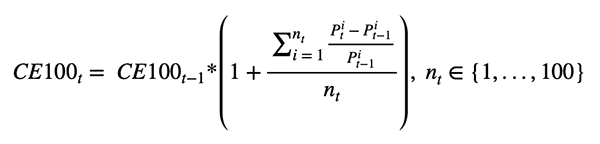

The CE100 Index is an unweighted index based on the average percent change in equity prices over time (adjusted for splits and dividends). The index at time t is equal to the index at time t-1 plus the average percent changes between time t and t-1 where t is any chosen unit of time.

We did not do a market-cap weighted index, as doing so would have made the index heavily dependent on a small number of highly valued companies (sometimes known as Big Tech or FAANG). Furthermore, unweighted indexes have been found to perform better than market-cap weighted indexes and similar to other alternatives.[1]

The composition of the CE100 is updated based on three criteria:

As a result of these compositional changes, the CE100 Index will be rebalanced over time and the number and identity of the participants in each of the 11 categories may change. Over time it is possible that we will merge or add categories as more information is revealed about the evolution of the connected economy. [2]

THE RELATIVE PERFORMANCE OF THE CE100 INDEX

The purpose of the CE100 Index is to track companies that will drive the digital transformation to a connected economy. Just like traditional equity indexes (the S&P 500, the Dow and the Nasdaq Composite), we expect the CE100 Index to rise and fall over time as new information is realized about the nature and speed of transition. Note that the Dow Jones and Nasdaq are market-cap weighted indexes.

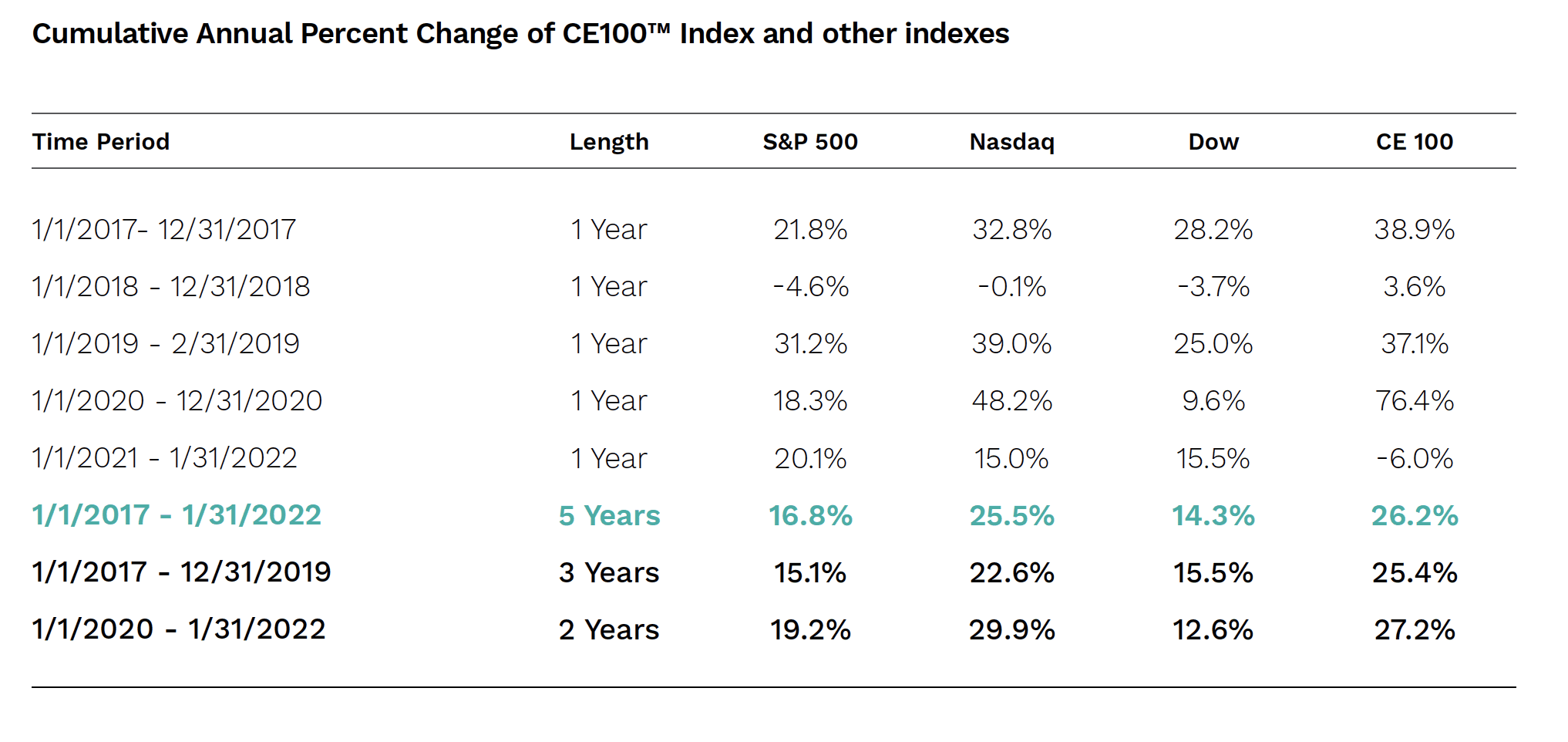

Figure 1 shows the five-year performance of the CE100 Index from Jan. 1, 2017 to Jan. 31, 2022, relative to the S&P 500, the Dow and the Nasdaq indexes. Figure 2 shows the two-year performance (from Jan. 1, 2020 to Jan. 31, 2022) of the CE100 Index TM relative to the broader indexes. The CE100 Index roughly tracked others until the early part of 2020, after which the CE100 Index diverged sharply from the other indexes as the pandemic accelerated the shift to the connected economy.

Table 2 shows the annual percent change in the indexes by year, from January 2017 through January. 31, 2022. For this period, growth in the CE100 Index led the other three major indexes, with an average annual rate of return of 26.2%. This was slightly greater than the Nasdaq, which returned 25.5% on average, and almost 10 percentage points higher than the S&P 500, which returned 16.8% per year.

TABLE 2

[1] See, for example, Hsu, Jason C. and Hsu, Jason C. and Chow, Tzee-man and Kalesnik, Vitali and Little, Bryce, A Survey of Alternative Equity Index Strategies (March 3, 2011). Financial Analysts Journal, Vol. 67, No. 5, September/October 2011, Available at SSRN: https://ssrn.com/abstract=1696333.

[2] We have replaced one firm from the CE100 selected in May 2021 to achieve broader representation across geographies and focus: we replaced US-focused AT&T with Airtel which operates mobile networks in Africa, India and other countries. We have not dropped any firms because of acquisitions or added any firms because of IPOs as of February 11, 2022.