By Sha’ista Goga1

I. Introduction

Enforcement agencies have amended laws and guidelines in recent years to deal with mergers that do not affect competition individually, but do on a cumulative basis. For example, amendments to the South African Competition Act allow for the authorities to consider other mergers engaged in by the parties involved over a set period,2 while the FTC Merger Guidelines of 2023 now explicitly incorporate guidance on multiple acquisitions.3

The adjustments and approach, such as the example above, are answers to a question that does not yet, however, have a clear-cut answer: whether serial acquisitions are harmful or not. On the one hand serial acquisitions are a predictable business strategy. A company with expertise and economies of scale in a sector is likely to seek out other growth opportunities that utilize their skills, which often can occur most easily through expansion in different geographic markets or adjacent product markets. However, concerns arise where acquisitions that are harmless when assessed individually increase market power when viewed cumulatively. The likely effects of these mergers may slip through the radar of competition agencies, where they fall under the notification threshold or there is no significant lessening of competition in the defined relevant market. A key question explored in this article is whether these difficulties pose a significant challenge to competition law enforcement and what measures can be taken to resolve them, using the South African experience as our focus.

Serial acquisitions that raise concerns typically fall into three main categories. Firstly, mergers in industries that typically have localized geographic markets but where there are elements of national competition dynamics. Secondly, conglomerate mergers by firms in adjacent markets; and thirdly, killer acquisitions (where a company purchases a potential future competitor with the purpose of closing it down). Assessment and enforcement become an issue where these mergers are not challenged (typically as they are below the merger notification threshold) or because they are not assessed when initial screening (taken in isolation) fails to identify a competitive issue.

II. The South African Experience

In South Africa, merger notification is based on turnover thresholds (although the Commission can require notification of small mergers). The test for blocking a transaction on the basis of competition, however, is whether a merger will “substantially prevent or lessen competition.” Within South Africa the impact of serial acquisitions (often termed creeping mergers) has long been a concern, with the concept being raised in Competition Tribunal cases involving sectors such as healthcare, retail, publishing and printing, and security. However, historically there has often been no merger-specific substantial lessening of competition found in the defined markets for these mergers, and transactions have been approved despite concerns over the broader pattern of increasing concentration. In Media24/Paarl the Tribunal noted that:

“There clearly is an established and ongoing practice…for the large players to acquire competitors in whole or in part while they are still relatively small. Such acquisitions often constitute “small” mergers in terms of the Act and therefore are not required to be notified to and considered by the competition authorities, despite the fact that the acquiring firm(s) involved may have large and growing market positions in the relevant markets and that the transactions thus have the potential effect of substantially preventing or lessening competition and/or raising public interest concerns.”

In this case, as in others, the issue was addressed by setting conditions, including conditions that the merging parties must notify the Competition Commission of small mergers in the future e.g. in publishing and printing of community newspapers (Media24 Paarl/Natal Witness),4 or in the security services sector (Fidelity ADT),5

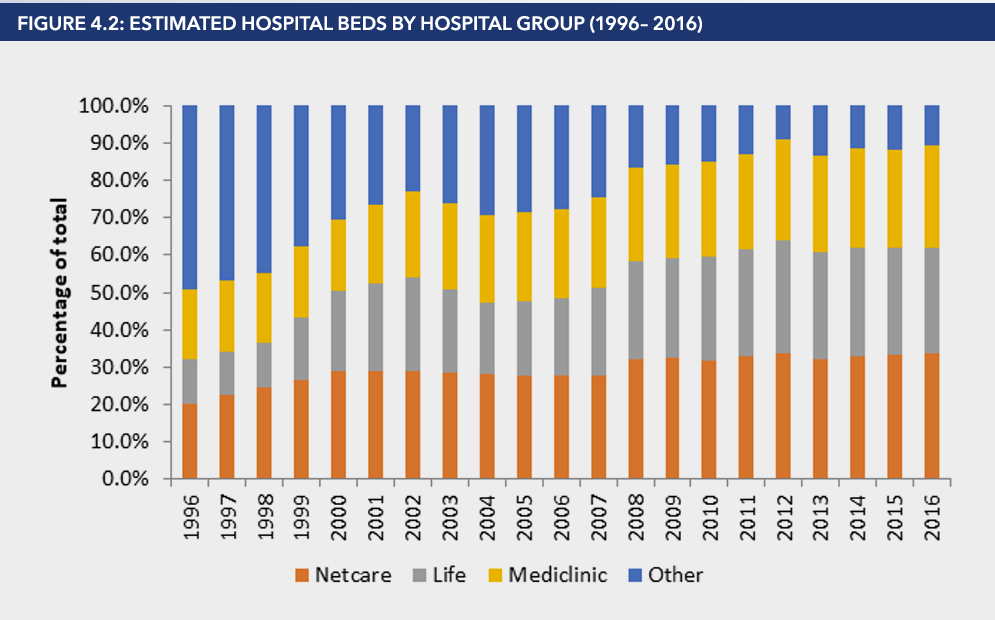

The impact of serial acquisitions is well illustrated in the hospital sector. The graph below, taken from the Competition Commission’s Healthcare Market Inquiry (“HMI”) in 20196 illustrates the change from a market in which over half of the market share was held by independents to one in which less than 10 percent of the market was out of the hands of three major groups, a situation reached largely through small, uncontested mergers or mergers that were allowed due to the small increment in national market share.

Figure 1: Estimated Hospital Beds by Hospital Group (1996-2016)

Source: Health Market Inquiry Final Findings Report Figure 4.2

In the healthcare industry this concentration has resulted in changes in bargaining power vis-à-vis the medical schemes7. The HMI describes how national hospital groups leverage their market share to prevent their hospitals from being excluded from scheme options and also helps them negotiate to receive higher tariffs with medical schemes.8 A range of hospital mergers assessed by the Commission in recent years considered these issues, with varying results given the legal framework at the time and the difficulty in providing sufficiently convincing evidence for the theories of harm. For example, while the Commission blocked the 2017 purchase of Lakeview hospital by Netcare, approval was given by the Tribunal (largely due to a lack of evidence).9 When the Competition Tribunal blocked the merger between Mediclinic and Matlosana, finding that it was likely to impact on Mediclinic’s leverage, lead to price increases, and a deterioration in patient experience, the decision was overturned by the Competition Appeal court who approved it, though this in turn was set aside by the Constitutional Court.10 This illustrates some of the challenges inherent in the analysis of small incremental mergers.

While in other jurisdictions serial acquisitions are often engaged in by private equity firms, this has not been the case in South Africa.

When the Competition Act in South Africa was amended in 2019, various factors that could be considered in a merger were specified. This included, in section 12A (k) “any other mergers engaged in by a party to a merger for such period as may be stipulated by the Competition Commission.”

This addition does help to some extent in capturing serial acquisitions within the South African context. If there is a merger that meets the notification threshold, in assessing it the authority can take all small mergers into account. This includes (i) increases in concentration that do not affect competition individually, but do so cumulatively, (ii) conglomerate mergers by firms in adjacent markets and (iii) killer acquisitions where there is a pattern of purchases. However, this is all premised on the Commission assessing the merger. This requires meeting the hurdle of the notification threshold unless notification is mandated at least once through another process such as a market inquiry. As such a gap still remains – if a merger is under the threshold and there is no ad hoc reason for notification it will likely not be considered.

III. Complexities in Considering Serial Acquisitions

While the legal possibility of considering prior mergers when assessing a merger that appears to be part of a serial acquisition strategy exists, even when a merger is flagged for further assessment, significant complexities may still arise.

Firstly, it is challenging to isolate a tipping point, or the stage at which a small incremental purchase leads to sufficient a shift in competitive dynamics that the blocking of a merger is justified. For example, even if an authority was concerned about concentration in the pharmacy sector, on a practical basis, would there be concern over Mr. Smith’s sale of their small pharmacy to a major group, leading to a 21 percent market share? Or the subsequent sale by Mr. Jones, leading to a 22 percent market share? Drawing the line of concern a priori absent any safe harbors or guidelines is a matter of judgement, and this can be quite challenging.

Secondly, identifying industries is not always straightforward. While it may be easier to look back at an industry and say this industry is now too concentrated, it is far more difficult to stop this concentration from occurring in the first place. The question for enforcement agencies is, therefore, whether situations in which serial acquisitions are going to be problematic can be identified in advance, and how industries of concern can be flagged. This could entail considering the patterns exhibited in markets in which serial acquisitions are a concern and assessing whether a similar pattern appears to be developing.

Enforcement agencies could consider whether there are ways of mapping and highlighting industries of concern. In South Africa this is partially done through concentration tracker studies, noting that competition markets may not coincide with the markets as defined in such studies. Market inquiries are also a tool that can potentially be used to study these markets in further detail.

Thirdly, the weighing of pro- and anti-competitive effects can be challenging. There can be difficulty in balancing different factors, such as the benefits of scale and efficiency against the potential anti-competitive effects, which are likely to be small when assessed individually and only manifest over a longer term. This is when aggregation or taking a longer-term viewpoint and considering the specifics of the actual market becomes important. Questions that require nuanced judgement include how an authority should deal with the third largest firm engaging in a serial acquisition strategy, for example, particularly when this would lead to scale and efficiencies enabling it to deal with larger competitors or suppliers. What happens from a dynamic perspective if authorities prevent entrepreneurs from monetizing their investments? What if this curtails one company but not others, risking the creation of asymmetric burdens on one company in the industry or a perception of bias?

IV. Potential Framework for Analysis

While these mergers are likely to be complex and require case-by-case analysis, the following section will now outline a tentative framework as a starting point for discussion.

Step 1: Classify what type of serial acquisition is at hand, and what the likely theory of harm may be. For example, if it is a classic staggered merger (where what should be a single transaction is split up over a few years to sneak under the notification threshold), an aggregation model for combining and treating these as a single transaction is a good and fairly straightforward way of dealing with the situation. For other types of transactions further analytical steps may be necessary.

Step 2: Analyse multiple markets. It is necessary to consider whether the competition analysis changes over different markets, including different market definition scenarios. This involves considering whether the primary competition market is adequate or whether alternative market definitions should also be considered. This would involve looking at market shares and dynamics, incorporating adjacent markets, and looking at broader or narrower markets where necessary. For example, in the motor vehicle retail sector, considering the impact of a merger on market shares in a narrow geographic area, or for a broad market for a class of vehicles may lead to a particular outcome, while considering the impact in a wider area for a particular brand where a buyer may be building a regional monopoly may lead to a very different result. In effect, a careful understanding of dynamics and analysis on all possible definitions, especially where local vs national dynamics are of concern. While this may broaden the scope of analysis it still requires merger specificity.

Step 3: Consider market dynamics carefully for both narrow and broad markets. This includes assessing how decisions are made upstream and downstream, and how changes in concentration shift power dynamics. This would require looking at the role of negotiations with suppliers in the market and the impact of the company purchased on suppliers. Is there a particular “must-have” branch that is being bought which may shift bargaining dynamics with customers or suppliers? In this, it is essential to consider the company’s past trajectory and future growth plans through acquisition, considering internal strategy documents to understand motive. The enforcement agency also needs to consider comparative markups and profits.

Step 4: Consider potential harm. This means considering potential changes in pricing power and bargaining power that could alter the competitive landscape. The nature of competition in the market is also important. It is necessary to assess whether independents play a constraining role in the exercise of any market power. Are any of the target firms mavericks or innovative firms? Another area for investigation is network effects and understanding what the benefits of additional purchases would be on the acquiring firm. Where the company involved is in an innovation sector consideration of the likelihood of a “killer acquisition” should be considered.

Step 5: Balancing factors: The benefits that may accrue because of the merger, including creating efficiencies resulting from economies of scale or other factors as well as the benefit of rescuing a failing firm need to be considered.

The vast part of this analysis can be done using existing frameworks if competitive dynamics are considered very carefully. However, for most mergers, reaching the threshold for consideration is a key issue.

While this all sounds straightforward, it is likely to create consternation from practitioners. One of the concerns with greater scrutiny of serial acquisitions is that it could potentially lead to a lack of predictability for merging companies. Having to consider a range of market definitions and theories of harm is onerous and has impacts on for legal certainty. It also has significant implications for the resourcing of competition authorities as thresholds are essential to limiting the case load.

As such, there is a question about how best to approach this in a manner that creates transparency. One approach is to focus on sectoral prioritization. Particular sectors can be identified and marked for further scrutiny based on market inquiries that indicate that there are rising challenges in a particular sector or identified through other forms of research such as concentration studies. This can also be done through creating rule-based structures. Consideration can also be given to creating safe harbors, potentially based on aggregation of mergers over time in the primary competition market, for example. Given the experience of other jurisdictions with respect to private equity “roll-ups” in sectors, private equity purchases over a threshold where there are previous purchases in the sector should have simplified automatic notification rules that allow for monitoring of incremental purchases in a sector.

V. Conclusion

Serial acquisitions can create serious competition issues if left unchallenged. Identification of sectors, and analysis of these mergers, while replete with challenges and nuances is possible and is ultimately still based on an understanding of competitive dynamics. However, given the potential effects on transparency, and the likely impact on resourcing if many smaller mergers require more in-depth analysis consideration should be given to creating a clearer means of flagging industries of concern and creating a framework for consideration.

Click here for a PDF version of the article

1 Director, Acacia Economics.

2 South Africa, Competition Amendment Act of 2018 available at https://www.gov.za/sites/default/files/gcis_document/201902/competitionamendment-act18of2018.pdf.

3 U.S. Federal Trade Commission (2023), Merger Guidelines, available at https://www.ftc.gov/system/files/ftc_gov/pdf/P234000-NEW-MERGER-GUIDELINES.pdf.

4 South African Competition Tribunal, Case no: 15/LM/Jun11.

5 South African Competition Tribunal, Case no: LM100Sep16.

6 Competition Commission of South Africa, Health Market Inquiry Final Findings and Recommendations Report, September 2019.

7 Medical schemes in South Africa are a form of non-profit private health insurance governed by the Medical Schemes Act with particular statutory requirements such as open enrollment, no price discrimination across older or less healthy members (community rating), and a minimum level of prescribed benefits.

8 See, for example para 65-67 of the Health Market Inquiry Final Findings and Recommendations Report.

9 Competition Tribunal of South Africa, IM193Oct17.

10 Competition Commission of South Africa v Mediclinic Southern Africa (Pty) Ltd and Another (CCT 31/20) [2021] ZACC 35; 2022 (5) BCLR 532 (CC); 2022 (4) SA 323 (CC); [2023] 1 CPLR 2 (CC); [2022] HIPR 200 (CC) (15 October 2021).