It is hard to imagine Harvard professors as anything but the sorts of people inclined to shop at J. Crew and with excellent manners. So naturally it comes as some surprise when one Harvard professor accuses another of popularizing a signature theory that she believes is mostly and dangerously wrong. That was the dust up among those hallowed halls last week when Jill Lepore went after Clay Christensen’s theory of disruptive innovation in The New Yorker. Never one to let a good debate go to waste, especially one in her own backyard, MPD CEO Karen Webster wades into the great Cambridge disruption discussion – and comes away with some of her own provocative ideas on whither disruption in payments.

Boston has hosted its fair share of public disputes over ideology. Some, like the Boston Tea Party and the American Revolution, have even changed the world. Last week, Boston hosted another public dispute, this one between two Harvard professors. But instead of taxes and political tyranny, their spat is over the one word that strikes the fear of God into the hearts of existing enterprises and has inspired tens of thousands of people to leave those firms to start their own: disruption.

It all began when Jill Lepore, the Chair of Harvard’s History and Literature Program wrote an article that was published in The New Yorker. She pretty much carpet bombed just about everything that her fellow Harvard colleague, Clay Christensen who teaches across the river at the B-School, ever wrote about disruptive innovation. She called into question his theory, alleged a lack of academic rigor behind his theory of disruptive innovation and accused Christensen of hand-picking stories that suited his theory just to keep it relevant. She claims disruptive innovation is nothing more than a conversation-starter about why some firms fail, not a methodology for how they could or should succeed. She produces evidence: she claims that most of the companies that Christensen points to as poster children for disruption actually failed themselves; points to Christensen’s famous quote about Apple in 2007 (“the prediction of the theory would be that Apple won’t succeed with the iPhone); and notes that the ROI of the $3.8 million Disruptive Growth fund started in 2000 using Christensen’s theory of disruption as its investment strategy which lost 64 percent of its value during the 2008 financial crisis crash (the Dow lost 50 percent during that same period).

Perhaps her most stinging rebuke is her depiction of the disruptors-can-do-no-wrong gospel; an attitude that condones and even celebrates failure because disruptors take risks and they’re supposed to fail while successful incumbents are only successful because they’re living on borrowed time and haven’t been disrupted yet. Both views, she says, force companies new and old to attach an artificial importance to the notion of disruptive innovation at the expense of just about everything else.

As you can imagine, Christensen didn’t find any of this terribly amusing, calling Lepore’s piece a “criminal act of dishonesty – at Harvard of all places,” in an interview he did with Bloomberg BusinessWeek last Friday.

Christensen’s 1997 book, “The Innovator’s Dilemma” is the tome that launched a thousand consulting careers not to mention the whole “disrupt or die” organizational mantra. His words of warning to established companies were that unless they did that, they were more or less hosed because new firms would come out of nowhere with new technologies that solved unmet customer needs and clean their clocks. The innovator’s dilemma he articulated is that established companies were actually doing the wrong thing if they were too busy doing the right thing (e.g. delivering shareholder value, running their businesses) to notice this new threat and so would shrivel into corporate oblivion. He cites evidence across industries like computer storage, steel and even retail that have all been upended by new players with new technologies over a period of time.

Lepore doesn’t drink that kool aid, not even a little bit. Her view is that disruption has become a catch-all buzzword applied retroactively to the companies that conveniently support Christensen’s hypotheses.

The one point on which they both agree is the need to “rein in” the runaway use of the word disruption in order to bring some “discipline” and rationality to the concept.

Disruption has become the catch-all word used to describe just about anything that anyone is doing that’s new. No one (but apparently Clay Christensen in 2007) would dispute that the iPhone is a massively disruptive innovation. But the word “disruption” loses a little of its luster and a lot of its credibility as a concept when used by every new start up or business to describe their idea. Yes, there are lots of good ideas and some really innovative ones. But there are very, very few truly disruptive innovations. Nielsen hands out innovation awards for products that are not merely a slight change to an ingredient or an overhaul of packaging or portion sizes. And whether an innovation is disruptive or not is sometimes not apparent for many years or sometimes longer. Yet, the halo now associated with bringing “disruptive” ideas to market and the market’s expectation that everything worth doing now has to be disruptive to matter creates a pressure to describe everything as disruptive – nothing less now will satisfy investors, CEOs and boards.

But is that the right way for companies to think about innovation?

Disruptive innovation is really, really hard to deliver, much less sustain and profit from. Most of the startups that attempt innovation of any kind fail, never mind the disruption innovation of which Christensen writes. So, unfortunately, do most of the established companies that try it.

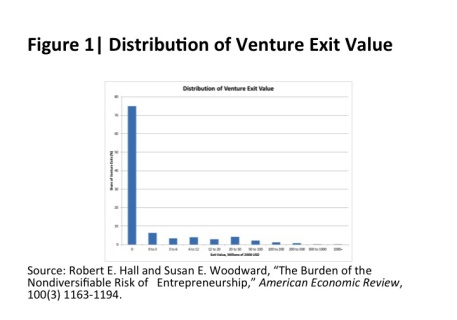

According to a whitepaper that my MPD colleague and economist David Evans co-authored in March 2014 on the topic of innovation, 50 percent of all new US firms (weighted by employment) fail in less than five years and only a third of startups that secured venture capital funding in the United States exited with a value of more than zero within five years. And those patents that are going to deliver the big pay day and big barrier to entry? The median value of a patent was just over US $1500 and only a very small percent end up being worth a lot. If you looked at big companies that engage in innovation the story isn’t much different. It’s a lottery. Most efforts at innovation fail. It would be great for a company to come up with a disruptive innovation, so it wouldn’t be disrupted itself; it would also be great if I won the Powerball Lottery.

If we look critically at the payments industry over the last decade or so, we’ve seen very few truly disruptive innovations and hear little about its many, many failures. Payments as a business are particularly hard. There isn’t one set of customers to figure out and please, there are many, and two in particular that hold all the cards: consumers and merchants. An idea that appeals to one of those customer groups is no guarantee that the other will find it just as interesting; and the payments landscape is filled with thousands of flops that couldn’t strike the right balance and, to use our word, ignite in a timeframe that was relevant to their customers and investors.

Now none of this is a knock on innovators and innovation but rather a stark reminder of just how hard it is for any new idea to succeed, never mind the one in a million disruptive innovations that Christensen writes about and says will fell industry giants in a single swoop, especially if those giants are in payments. If success is defined as delivering a return to shareholders or investors, the empirical evidence suggests that most simply don’t. Yet that doesn’t stop existing companies from feeling pressured by their boards and executive teams to “be disruptive “every time any innovator launches something new.

Part of the problem is the unrealistic expectation that everything has to be totally disruptive to be relevant. The other part is that disruptive innovation is really hard to define – and real disruption isn’t really seen as being truly disruptive until after the fact, a point that I think Lepore unfairly knocks in her piece as evidence of the uselessness of Christensen’s theory of in predicting what will be disruptive.

Take the iPhone, for instance, something we all now recognize as completely and totally disruptive.

When the iPhone was introduced, it wasn’t the first or even second smartphone ever to hit the market, but it was a great product with a great design and a new business model. The Blackberry, Symbian-OS based phones, and Windows-based phones were all slugging it out for market share. The iPhone evolved to become disruptive as its apps store ignited and the ecosystem around the iPhone and app store took off. The iPhone then not only became a disruptive innovation – but not of the laptop industry as Christensen remarked in his interview last Friday – but of the content distribution and marketing and advertising industries. The iPhone’s real source of disruption now is in its use as an enabling platform for many other disruptive innovations that leverage it to solve the unmet consumer needs that those innovators identify.

And it’s on that point that I think Christensen misses an important dimension of disruptive innovation.

His definition of disruption is “using new technology to solve unmet customer needs.” But that implies that everything disruptive gets its bona fides from using brand new technology that the disruptor invented from scratch. Apple didn’t invent the technology that it uses in the iPhone, its engineers and software developers leveraged existing software and circuitry and technologies and other components to develop something truly disruptive. But what it did achieve was something that is characteristic of true disruptors – it shifted the balance of power in the ecosystem. In Apple’s case, it did that by creating a platform that developers wanted to be a part of; one that was so compelling that mobile operators were willing to adjust their own business models to be a part of Apple’s new one.

Now, if those mobile operators had been Christensen’s students, the theory of disruptive innovation would conclude that that they should have seen the iPhone coming and developed it first. But is it really fair to think that any of those carriers – whose skill sets and core competencies are entirely different from Apple’s – would have the wherewithal to create the next iPhone? Maybe no more so than expecting Smith Corona to have developed the laptop out of its typewriter business. It just seems implausible to put pressure on any organization to be something they aren’t and can’t become. The expectation that every single incumbent firm sign up to being a disruptor or suffer a fate worse than death seems more than a little unrealistic and even unhealthy for the shareholders.

But does that excuse them (or any incumbent) from watching the competitive landscape, monitoring technology innovations, understanding who their customers are and how their needs are changing and then devising plans to respond to all of the above with innovative new products and services? Of course not , but that’s unlikely to lead to big-bang/holy-moly/game-changing innovation of which Christensen speaks, but rather the incremental innovation that I would argue is just good business and provides the basis for delivering a return to the shareholders.

So, how should firms think about innovation and disruptive innovation so that they can convince themselves and their investors that they won’t end up on the “wrong side” of it?

For established players firms, it’s always first about doing the things that provide a return to their shareholders and investors. That doesn’t mean that firms shouldn’t be innovative, but rather than they understand both their assets and their limitations and then decide how to leverage and manage both to (a) satisfy customers and (b) make profits. Yeah, I know, you say, tell that to Amazon, but they are the one in a million company that has gotten a pass from Wall Street without making much of a profit. Most companies aren’t that lucky and a lot of VCs are now even using a company’s ability to break even as a litmus test for investing.

Companies do well when they realistically take stock of what they can do best and then build an innovation roadmap from there. Sometimes that means innovating incrementally, other times it means being a fast follower (when it makes sense) or not a follower at all (when it doesn’t). Other times it means acquiring firms or people to accelerate an agenda. Frankly, sometimes it means recognizing that the best thing for shareholders is to simply milk the asset and recognize that firms like people, die. But all of the time it means having a clear vision and rationale for the future based on good data – about them, their market, their customers, technologies – and the good judgment to recognize fact from passing fancy.

And, that’s where I think that Lepore’s criticism of the disruptive innovation disciples makes some sense. The innovator’s dilemma disciples would argue that the past is useless in predicting the future because disruption comes out of nowhere and you can’t learn anything from looking back. As a historian, you would imagine why she would disagree with that. But history has told us a lot about how innovation in payments ignites if you’re willing to take the time to examine it. Its what my colleague David Evans and I relied on in the mid 2000s to question whether NFC had the cojones to make it in payments. I think it explains why NFC hasn’t ignited and Beacon has. Why Square could ignite initially as an mPOS player and why it has struggled to ignite as a digital wallet. Why the payments networks and banks find it hard to get traction with digital wallets and why PayPal and Apple have a powerful advantage there. Why Chase Merchant Services may be able to pull off creating a new three party system and why Clinkle was doomed from day one. And why Amazon’s new Fire phone will struggle to ignite, in spite of its efforts to pay developers to play in its apps store and why Google Checkout and the early attempts at Google Wallet stalled. It’s also why Silicon Valley is head-over-heels-in-love with bitcoin: it’s disruptive so it must be fabulous!

I also agree with Lepore that for disruption innovation to be predictive, it needs a methodology which is rigorous and empirical and upon which decisions can be based with confidence. Predicting the future efficacy of cancer treatments, for example, is all about having a rigorous methodology for experimenting and documenting what does and doesn’t work and learning from the mistakes and the successes. Deciding how to innovate in payments isn’t at the level of curing cancer, for sure, but having a rigorous methodology for assessing why disruption did or didn’t succeed is pretty critical in payments and commerce where ecosystems are overlapping and decisions about what to do become more and more complex (and critical to get right) each year.

We lack that today. But only when you can you rise above the hand-waving vagaries of everything-has-to-be-disruptive-or-its-no-good attitude and separate the signal from the noise can you really begin to devise strategies that will (a) satisfy unmet customer needs, (b) make profits, and (c) deliver innovation, and if you’re extremely lucky, maybe even the disruptive kind.

It’s frankly what’s inspired us to do just that around an initiative you’ll be hearing about very soon – an Innovation Index that we are working with a Harvard Business School professor (not Clay J) to develop and launch. It will measure the state of innovation in payments and then provide an important benchmark for helping established companies assess how to allocate resources accordingly, and show them with data where they are relative to the payments ecosystem and their peers. It’s certainly not designed to tell companies where to invest for innovation, but more clearly help them decide how to sure up their own resources to innovate in a way that adds value to their shareholders.

Stay tuned.

Until then, where do you come out on the innovation and disruption and the showdown at Harvard?

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More