It’s not news that the 70 million people born between 1980 and 2000 — the millennials — are financially challenged. But Karen Webster says that new research out of Stanford sheds extraordinary new insight on their financial state of affairs. Only 50 percent of them will ever outearn their parents, and the picture gets worse for middle and lower middle class kids. That, Webster says, raises a whole host of questions for society and some big decision points for the payments, retail and commerce players seeking to serve them. She lays it all out here.

It’s a fact.

While they enjoy many FinTech innovations, most millennials don’t have a snowball’s chance of earning more than their parents — ever.

How big the income gap between those 70 million people and their parents depends on a few things, including how well-heeled their parents are. Not surprisingly, hardest hit are the kids born to middle and lower middle-income families — so, roughly 70 percent of the U.S. population.

Stop and think about that for a minute.

It’s one thing for the millennial offspring of the billionaire hedge-fund scions to fall short of making a billion because they only manage to pull down $760 million a year. No one’s worried whether those 30-somethings will be able to put food on their table or make the mortgage payment.

But when not even half of millennials born to middle-class families and a third of millennials born to families in the middle to lower middle-income brackets have a shot at making more money than their parents, that suggests that we are facing a very different set of problems as a society.

And a set of problems with some very pointed implications for everyone in payments, retail and commerce whose ambition it is to capture the purchasing power of this coveted generation.

Which may end up not being all that powerful.

This is not a new topic of conversation.

In 2013, data was beginning to trickle in that suggested that the generation that made Sriracha a food group and yoga pants a go-to corporate wardrobe staple was under financial duress. That year, research reported that the typical net worth of millennials was 20 percent lower than that same age cohort in 1983 — at the same time, that of their parents had more than doubled. The concern then was not on their income or spending power but the implications that suggested for the retirement and the subsequent standard of living that generation would enjoy (or not) 30 or 40 years into the future.

Since then, there have been dribs and drabs of insight into the millennial’s financial state of play, their mountains of student debt, their love/hate relationship with money and their attitudes about work and career. But it’s the recently published groundbreaking research by Raj Chetty, professor of economics at Stanford, and several other of his academic colleagues that finally put a pin in the fact that the generation that every brand is desperately trying to woo is, by and large, broke and is unlikely to ever attain the earnings potential of their parents.

This research is extraordinary — and extraordinarily insightful — because it did something that no one else has ever been able to do: link income patterns across generations. Chetty and his team did that by gaining access to the anonymized tax returns of people in their mid-30s over a 40-year period between 1940 and 1980. The complete piece of research can be found here, and New York Times columnist David Leonhardt did a brilliant synopsis of their work two weeks ago, here.

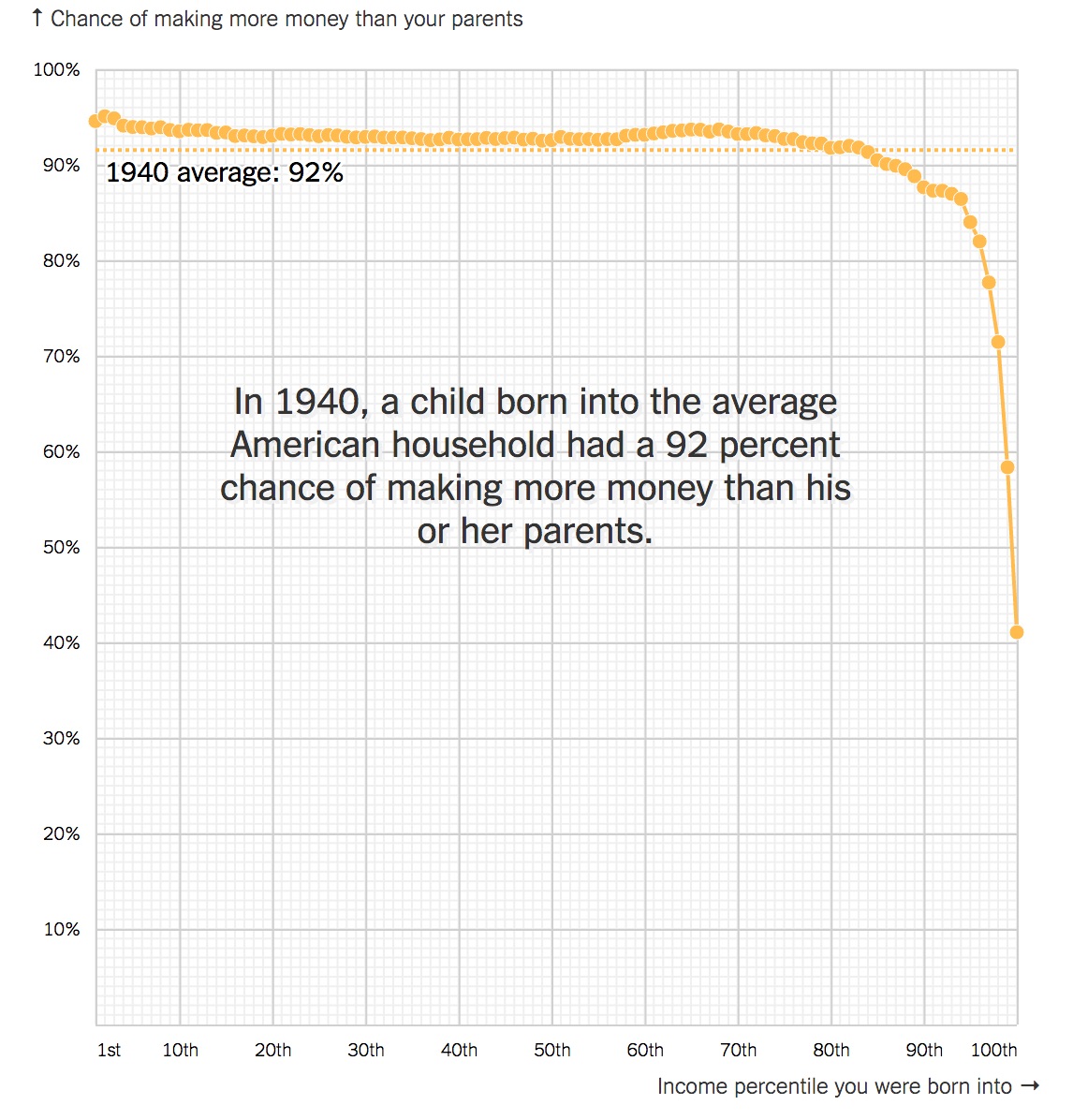

The Chetty paper is worth a read, but all that you really need to know about his conclusions is summed up in two charts, courtesy of Leonhardt’s column.

This one tells the earnings gap story at a high level.

Source: nytimes.com

The news flash here is that the prospect of kids entering their third decade of life and outearning their parents has been on a slippery slope since the 1950s. Kids of parents born in the 1940s had it the best, not surprisingly, given the intersection of the Great Depression in the 1930s and the rapid expansion of the economy that followed — driven by the wholesale shift from a farm-based to a manufacturing-based economy. The subsequent ebbs and flows of the economy caused by energy crises (the 1970s) and tech revolution and globalization (the 1990s) dented those prospects a bit for boomers (born in the 1950s–early 1960s) and a little more so for Gen Xers (mid 1960s–1970s).

But that downward slide took a nosedive for the kids born in the 1980s — or what we call today the millennial generation. Overall, only half of them will ever best the earnings potential of their parents and even, quite possibly, their elder siblings.

Depending on that millennial’s lot in life, even 50 percent may look optimistic.

The prospects dim for a great swath of millennials living in households with incomes that fall below $100,000 a year. That story is again best told courtesy of this chart found in Leonhardt’s column.

The millennials whose parents belong to the 1-percenter club will be fine, thanks to receiving a great education at the top schools and nabbing one of the high-paying jobs that go along with having that pedigree.

But those living in middle class families — those whose household income is between $50,000 and $100,000, or 50 percent of the U.S. population — fare much worse. Only 44 percent of those kids have the prospect of making more than their middle class parents. And for the 29 percent of the U.S. population earning less than $50,000, the prospects are very grim.

The explanation for this varies, and experts say that it isn’t necessarily the result of just one thing.

Some economists attribute at least part of this disappointing financial picture to an increase in the rise of single-parent households. Others attribute the problem to millennials entering the workforce during and/or in the immediate aftermath of the 2008 financial crisis. Those kids took lower-paying jobs just to have one — the undergrad in art history from Colby who took a job as a barista at Starbucks or underpaid member of a starving startup team — while others stayed in school longer since they couldn’t find even so much as that. A large portion of them work as part of the gig economy, and many rather like it that way. Regardless, experts say, millennials will be hard-pressed to make up the income deficit (and pay off the additional student debt for those who stayed in school) that’s been compounding over those last eight years.

At the other end of the spectrum, to the well-educated go the well-paying jobs as technology has evolved to change both the job specs and job requirements of what were once traditional businesses that employed big groups of people and paid respectable salaries.

Take the ad business.

In the days of Mad Men and even through the 1990s, selling advertising was often the domain of a slick sales guy (yes, a guy) calling on newspaper, magazine and broadcast executives over three-martini lunches. Creative copywriters and graphic designers were left to develop the persuasive copy and appealing visuals that moved products. Measuring effectiveness was hard, if not impossible — as the famous John Wanamaker quote underscored: All brands that wanted to sell their products bought advertising, and all of them knew half of it worked, just not which half. But the only way to get anyone’s attention about a product was to advertise on one of those three media channels. It was a pretty good gig.

Today, B2C advertising is increasingly a data game served by ad platforms to consumers toting digital devices who spend most of their time with their noses inside of social networks. Ads served up by algorithms created by PhDs in computer science and engineering working for massive ad platforms like Facebook and Google drive demand. Sure, there are still ad sales guys and gals that touch the brands who want to advertise, but their pitches are delivered remotely (even in a self-serve capacity) via a well-constructed, well-scripted, data-driven sales pitch. The genius data scientists get the big bucks, and the sales guys get a modest base plus whatever they can sell in the CPM-for-hire game.

All of this, Chetty points out in his paper, is coming at the same time that GDP in the U.S. is slowing and productivity gains are at an all-time low. The economy would have to post 6-plus percent annual growth to reverse this trend for the millennials, Chetty writes — something that he and most sensible economists agree would be a near impossibility to achieve.

The resulting productivity gap is something that even the brightest of economic minds haven’t been able to fully explain, much less prescribe a solution to overcome. But there’s no doubt that it exists and only seems to further seal the deal that millennials in the U.S. face a far different financial future than their parents and their grandparents before them.

I’ll leave the debates over policy and politics on this topic to someone(s) else. Instead, I’d like to get you thinking about the implications for payments, commerce and retail for a generation of 70 million that may be strong in number but weak in spending power.

We’ve all read the same stories and heard the same anecdotes: Millennials are saddled with sky-high student debt, aren’t buying cars or houses, don’t have credit cards, aren’t saving money and are job-hopping like there’s no tomorrow.

Besides that, they’re the ideal credit risk and perfect target to stake the future of FinTech, payments and retail.

Here’s what that looks like, by the numbers.

The National Association of Realtors says that home ownership for those under 35 — first-time homebuyers — is down to 36 percent of that age cohort from a high of 43 percent in 2005. The age of that first-time homebuyer is also creeping up — to a single person aged 33, up from a married 29-year-old in the 1970s. This, despite rents being 38 percent higher than mortgage payments and interest rates at an all-time low.

The big problem isn’t lack of want, experts say; it’s the struggle to come up with a down payment, first, and then qualify for a loan, second. Thinly credit-filed millennials, with their job-hopping, gig-economy proclivities and the future earnings power deck stacked against them, leaves lenders squeamish — the same lenders that observe mortgage payments rising from 1.7 times annual income in the 1970s to 2.6 times annual income today. And since most first-time home buyers are also single, marriage and family are also pushed further out into the horizon.

No home ownership (or marriage or family), of course, means no spending by them on home repairs, or furnishings, or insurance or the raft of kid stuff that triggers a myriad of expenses on the way to owning that piece of the American Dream and raising a family.

The same holds true for car ownership, which, for millennials, is also at an all-time low. Only 26 percent of millennials have a car loan, and fewer of them are buying cars at all. When uberX and Lyft rides cost only a few bucks to get across town, the investment in buying and maintaining a car seems pointless. Those with cars are hanging onto them longer and even refinancing them to reduce their monthly debt burden.

Then, of course, there’s the credit card, which accounts for 36 percent of all consumer debt and is the tool that the parents of those millennials used to finance their own American Dream. Only about a third of all millennials have a credit card — in other words, 67 percent of millennials don’t. Those who do carry a balance of roughly $5,800 on their cards, and 60 percent of them revolve their outstanding balances each month, compared to 47 percent of all cardholders who do the same.

Some millennials don’t want a credit card for fear of getting in over their heads, but most can’t get one. Thin credit files, while typically fingered as the scapegoat, are not entirely to blame. Unlike their parents and grandparents before them who could prove an upwards earnings trajectory and, therefore, could offer banks a healthy overall risk profile when they applied for one, millennials simply can’t.

Banks see these same trends. They see millennials as most likely to be high revolvers (they like that) but also among the most likely to miss payments completely (they hate that). These, of course, are the same bankers who understand that credit card debt typically peaks for individuals in the 45–54 age group — in other words, millennials a decade from now. Without cards, or the prospect of rising earnings power, issuers won’t be able to count much on millennials following, en masse, that pattern of borrowing — or the revenue that results from enabling credit for them.

All of this raises a number of topics for discussion over a cup of holiday cheer these next couple of weeks.

For instance, what does it mean for a millennial to be a good credit risk? If it isn’t the prospect of long-term earnings potential, then how does that change how banks and retailers think about extending credit? Or should it? Will the traditional credit card model give way to transactional credit models where risk is decided and credit extended one item at a time? Who, then, extends that credit, and what infrastructure is needed to support that one-item-at-a-time credit authorization? Will new players emerge with different methods of aggregating millennial debt? How would credit rating and scoring agencies have to adjust to accommodate any and all of these changes?

Then, there’s the bastion of the American Dream — the home mortgage. How will mortgage lending have to change? It may not be enough to simply offer millennials a totally digital mortgage application experience if the underlying facts about their borrowing profile don’t change: They’re not considered great credit risks given their employment idiosyncrasies, and they can’t come up with a down payment. Lenders — whether they be alt-lenders or traditional banks — only lend money to people they believe will pay them back. Will that mean a shift to banks and innovators helping millennials save and/or creatively thinking about how mortgages are structured and repaid?

Banks, clearly, are thinking hard about serving this group beyond just lending to a group of customers that may be hard to serve on that score. Yet, millennials still need banking services, FinTech, digital — of course — but more basic options to act as a store of funds, possibly with options to pay down their debt and help save their money. How will this force banks to think differently about the portfolio of products that they offer to millennial customers — and price them — who may not ever use credit at the same level as their parents?

Retailers, on the other hand, must contend with the reality that only a third of the millennial customers that walk into their stores have credit cards with them. For the obvious reasons, value for money is a key driver of loyalty for millennials, as are rewards and promotions. But payment, for most of them, is more likely debit card-driven than not. And while Durbin’s made debit cheaper than dirt for most retailers to accept, it’s cramped banks’ style when it comes time to doling out rewards when those cards are used. Will serving this group be served with a healthy dose of new thinking about how banks, digital wallets and retailers collaborate to serve this new customer and still maintain their own healthy bottom lines? Will retailers be challenged to think differently about how they extend credit to this group of customers? Will millennials take the retailer-branded debit card bait?

Food for thought: One of the most popular articles on PYMNTS.com this holiday season was the piece we did on Walmart’s layaway program. Layaway became popular in the 1930s during the Great Depression and was largely disbanded in the 1980s as credit card usage skyrocketed. Is it time for retail credit to go back to the future for this demo?

A few things in closing.

First, we need to be careful when talking about “millennials” since they are not a homogenous group. Even though 50 percent of millennials won’t outearn their parents, 50 percent will, and the fraction of those who hail from the more affluent households will ultimately have the spending power and means to do the things their parents did, even if they do start all of their spending a little later than their parents did. It’s the other 50 percent that represents the challenge for us as a society and as a payments and commerce ecosystem — and the much harder problem to solve.

There’s also the fact that the baby boomers — their parents — represent the wealthiest segment of the economy with the most disposable income at hand. As a group, they’re living longer and spending well into their elder years. The eldest boomers have turned 70, and they’re likely to live longer than their parents.

The millennial children of those parents, then, probably don’t need to worry. Their parents will have enough left over to hand them a nice inheritance. Unfortunately, that’s not true for the bulk of millennials. Their parents aren’t that well-off and need what they have to take care of their hopefully long lifespans.

For all of you wishing you were still “29,” maybe think again.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More