FinTechs Look to M&A for Profitability as Economic Shake-Up Continues

August 2023

Once fierce competitors, banks and FinTechs have dropped their guard to collaborate and partner in recent years. However, as FinTechs continue to feel the sting of economic headwinds in 2023, many may be in the market for banks seeking full acquisitions in the next two years and beyond.

01

FinTechs face powerful economic storms that are dampening investors’ previous fervor for these digital upstarts. Rising interest rates, high inflation and lower consumer spending have put pressure on FinTechs’ business models, resulting in some costly failures.

02

Regulators are finalizing guidance and stepping up enforcement against banks that fail to monitor their FinTech partnerships, but for banks and FinTechs that are compliant, the new guidance offers a powerful endorsement of their relationship.

03

Bank-FinTech alliances and M&A are proving to be a two-way street, bringing benefits — including profitability — to both. Banks are not the only buyers, moreover, with FinTechs themselves gaining new capabilities by acquiring other FinTechs.

Get Unlimited Access

Complete the form below for free, unlimited access to all our Data Studies, Trackers, and PYMNTS Intelligence reports.

Thank you for registering. Please confirm your email to view all our Trackers.

The economy stands to make for some unlikely unions in the financial technology space over the next 24 months. Banks have traditionally viewed FinTechs as agile rivals in the digital transformation of banking that has taken place over the last several years, especially as FinTechs rode a massive wave of growth. Although banks have been catching up on the technology, many are still fish out of water when it comes to launching state-of-the-art digital financial services, making FinTechs attractive targets for partnership — or ownership.

Some FinTechs, meanwhile, buffeted by strong economic headwinds since 2022, may be viewing acquisition by banks in a favorable light as they seek an exit strategy to avoid closing shop altogether. Moreover, banks are not the only ones doing the buying, with leading FinTechs themselves looking to expand their capabilities through mergers and acquisitions (M&A) with other FinTechs.

FinTechs face powerful economic storms that are dampening investors’ previous fervor for these digital upstarts. Rising interest rates, high inflation and lower consumer spending have put pressure on FinTechs’ business models, resulting in some costly failures.

FinTechs continue to struggle against a receding economic tide.

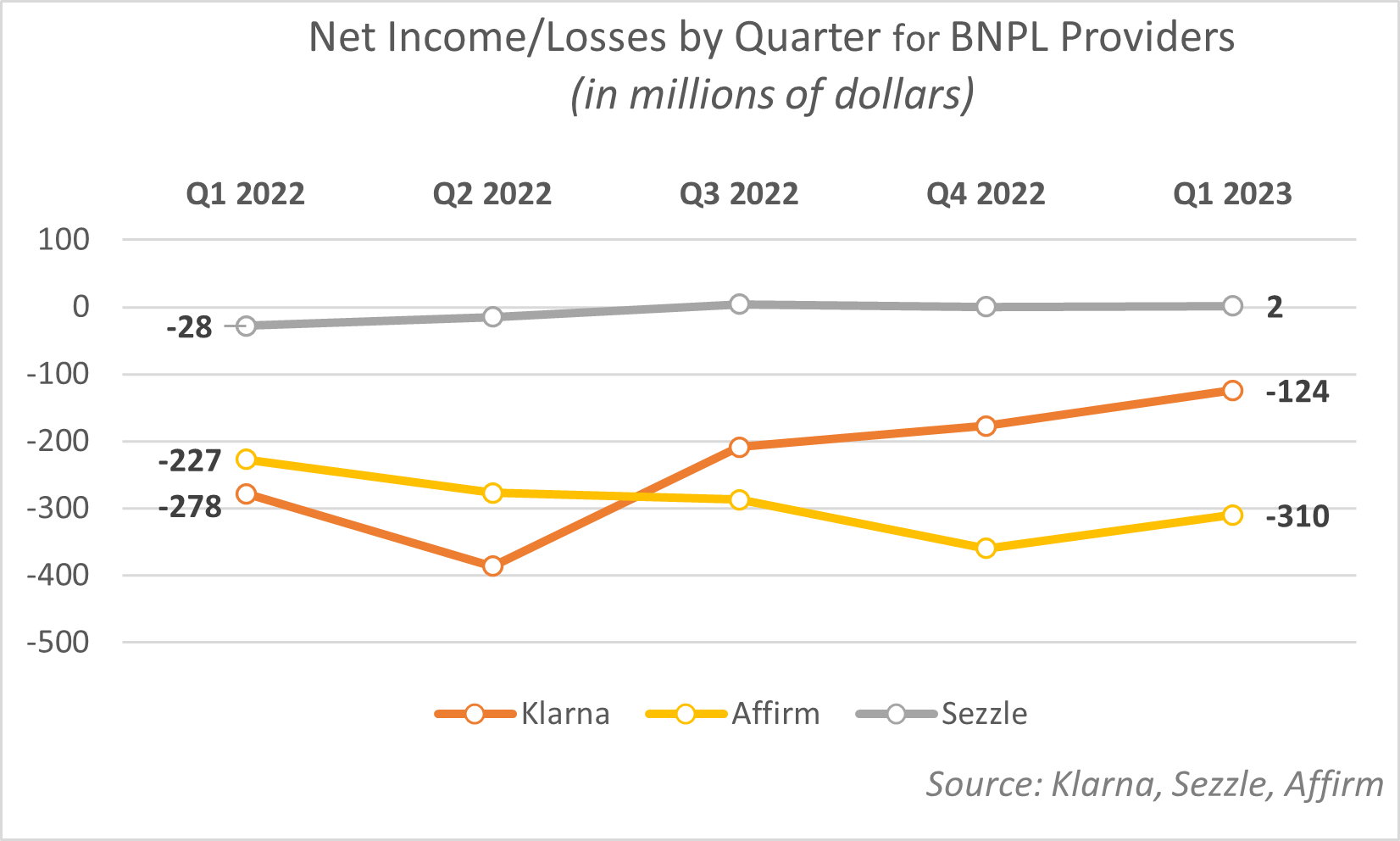

The FinTech space experienced a notable setback in 2022 as the forces of pandemic-fueled transformation and economic stimulus began to wane. The impact was especially pronounced in the buy now, pay later (BNPL) sector, culminating in major losses for some important players, including Affirm, Klarna and Zip. Klarna, for example, valued at $45 billion at its zenith in 2021 as the world’s second-most valuable FinTech after Stripe, dropped in valuation the following year to a mere $6.7 billion — an 85% tumble.

FinTechs continue to face powerful economic headwinds in 2023. Rising interest rates, high inflation and lower consumer spending have put pressure on FinTech companies’ trailblazing models, requiring some painful adjustments. For BNPL providers in particular, higher interest rates have made it harder for them to offer the interest-free payments that distinguish BNPL from other credit types, as providers typically cover the cost of the interest-free period.

FinTech funding is meeting with new caution from private investors.

Interest rate increases and a slow economy are also making private funding more expensive and less available for FinTechs. This development has the potential to set the stage for takeovers by banks, especially of smaller FinTechs hoping to consolidate with larger entities to scale and become profitable. Such acquirers, however, will be looking to minimize the costs of acquisition. With FinTechs still reluctant to lower their valuations, some may find themselves out in the cold once they finally realize what they stand to gain from a buyup by a bank or other company.

This is not to say that banks are calling the shots entirely, as they continue to struggle with digital transformation and have suffered an unprecedented spate of failures themselves, most notably in the recent meltdown of Silicon Valley Bank and others. Although many banks and FinTechs appear to be eyeing one another with a “wait-and-see” attitude, some analysts charge that consolidations are actually the best way forward for both.

Regulators Formalize Bank-FinTech Partnerships

Regulators are finalizing guidance and stepping up enforcement against banks that fail to monitor their FinTech partnerships, but for banks and FinTechs that are compliant, the new guidance offers a powerful endorsement of their relationship.

There’s been an ongoing link between recent enforcement actions and expectations that banks really understand how their FinTech partners are operating.”

U.S. regulators are formalizing bank-FinTech partnerships with finalized guidance.

Once sworn foes determined to replace each other, banks and FinTechs have forged strategic alliances as they realized their complementary needs, with FinTechs by turns serving as technology vendors to banks or as customers of banks’ licenses in banking as a service (BaaS). In the latest iteration of this growing relationship, legislators are establishing regulatory frameworks for bank-FinTech partnerships, signaling a new era of both approval and heightened scrutiny.

The Federal Reserve, the Federal Deposit Insurance Corp. (FDIC) and the Office of the Comptroller of the Currency recently issued finalized guidance to banks on their required due diligence when partnering with FinTechs. The guidance is intended to ensure that FinTechs, especially startups, comply with fair lending, privacy and anti-money laundering (AML) regulations. This marks the first time strong guidance of this kind has been issued in the United States, representing yet another sea change for FinTechs in the business climate going forward.

Lawmakers are getting tough with partnerships.

Regulators have worried about bank-FinTech partnerships being exploited to circumvent regulations, with banks merely serving to fund online lenders without clear supervision of FinTechs’ underwriting and loan servicing practices. The guidance seeks to “stop the gaming of financial regulations by laying out how banks are responsible for a FinTech’s compliance failures,” according to a recent article by Bloomberg Law.

Regulators are also stepping up enforcement against banks that fail to monitor these relationships accordingly, with the FDIC recently issuing a consent order to Cross River Bank regarding its alleged laxity in overseeing its FinTech partners. On the other hand, for banks and FinTechs that are compliant, the new guidance offers a cautious but potent nod toward their potential to profit from partnering.

Bank-FinTech Symbiosis Is Working

Bank-FinTech alliances and M&A are proving to be a two-way street, bringing benefits — including profitability — to both. Banks are not the only buyers, moreover, with FinTechs themselves gaining new capabilities by acquiring other FinTechs.

It has now become apparent to the FinTechs that the banks have opportunities to be the backbone of lending and/or financial services. And then [the FinTechs] get to be the frontman. … That can be a very symbiotic relationship. We bring the capabilities of a massive institution of lending and regulatory control. They bring the creativity of FinTech and customer experience and technological connectivity together.”

Bank-FinTech alliances are proving mutually beneficial.

Citizens Bank recently announced it will partner with FinTech Wisetack to offer BNPL loans to small to midsized businesses (SMBs). The partnership will expand Citizens Pay, the bank’s consumer installment payment service, to include pay-over-time financing for home improvement projects through the Wisetack platform of contractors, merchants and software-as-a-service (SaaS) solutions.

As one of the largest U.S. banks, Citizens has a considerable information technology team, yet it freely admits that the partnership’s focus will be to grow the bank’s technology by acquiring the infrastructures it lacks. These include the FinTech’s faster delivery capabilities and application programming interfaces (APIs). Wisetack, for its part, hopes to deepen its partnership with Citizens by launching additional joint products.

Some FinTechs are profiting substantially from acquisition by banks.

British workplace savings and pension FinTech Cushon recently announced it had been fully acquired by NatWest Bank for £144 million ($182 million), netting one of its biggest investors — itself a FinTech — a return of greater than 100%.

After leading Cushon’s Series A round in June 2021 with a £5 million ($6.2 million) investment, Augmentum Fintech raised it another £5.8 million ($7.2 million). Following the acquisition, Augmentum will gain £22.8 million ($28.3 million), representing an internal return rate of 61%.

FinTech leaders are also making acquisitions of their own.

FinTech giant FIS recently acquired BaaS FinTech startup Bond for an undisclosed sum. Thirty Bond employees as well as co-founder and CEO Roy Ng reportedly will join FIS but will continue to operate independently. Tarun Bhatnagar, president of platform and enterprise solutions at FIS, referred to the acquisition as a “small but important purchase” that will round out FIS’ stable of professionals with BaaS and embedded finance experts, permitting it to “close a gap” in its proficiencies.

Meanwhile, European FinTech unicorn Zepz seems to be getting a jump on the strategy by explicitly setting its sights on growth via M&A. The company, which is launching a digital wallet aimed at helping migrant communities that send money frequently overseas, seeks to enter new markets and strengthen its position in the industry by leveraging strategic mergers. Citing the downturn in private FinTech valuations, CEO Mark Lenhard recently told CNBC that acquiring or partnering with companies will allow Zepz to accelerate its growth, personalize services and thereby compete with bigger rivals, such as PayPal.

Expansion did not seem to be on Zepz’s road map during its recent cost-cutting efforts, including a workforce reduction of 420 employees globally. However, the CEO stated that the efforts were part of a restructuring to enhance its future growth outlook — suggesting, perhaps, that M&A was the game plan all along.

Regulatory Compliance Will Be Key to Bank-FinTech Consolidation

Many analysts and participants agree that FinTechs are on the brink of a swell in M&A activity. Some watchers are welcoming the current economic environment as an opportunity to separate the wheat from the chaff in the FinTech space and profit from investments accordingly. Areas such as embedded finance, BNPL and business-to-business (B2B) digital payments innovation are not going away, so banks will continue to view FinTechs that specialize in these capabilities as advantageous partners and purchases.

Whether they are considering strategic partnerships or M&A with banks, FinTechs’ first step must be to gird themselves both financially and for regulatory compliance. This will be critical not only for their own well-being but also for making them stand out in a pool of acquisition candidates, should a bank merger prove their best option. Sezzle CEO Charlie Youakim reported in a recent interview with PYMNTS that FinTechs’ eligibility for bank acquisition correlates directly with their becoming more “in tune” with regulatory matters. Similarly, FinTechs that fail to keep up with these requirements could miss their chance at a mutually beneficial alliance. As Youakim sees it, there are a number of prerequisites for FinTechs at this juncture:

Focus on proving profitability.

Recognize how essential the compliance and regulatory aspects of financial services are.

Cultivate a culture of building growth momentum.

As the economic shake-up continues, only the fittest FinTechs will survive and thrive. A back-to-fundamentals approach will serve them best, no matter which way the wind blows.

The bank-FinTech relationship is poised for further evolution as it responds to technological advancements, shifting regulations and economic conditions. Adapting to economic challenges, both banks and FinTechs will likely diversify revenue sources and refine their risk management strategies. Regulatory guidance will play a significant role, with both parties needing to adapt to changes in consumer protection and data privacy rules. The relationship will likely expand beyond traditional roles, with banks incorporating FinTech solutions and FinTechs offering broader financial services. This customer-centric approach will be pivotal as cross-border collaborations increase, potentially restoring investor confidence and encouraging market consolidation. Amid these changes, data security and maintaining customer trust will remain paramount for sustained growth and innovation.”

Charlie Youakim

CEO

About

Sezzle is a payments company on a mission to financially empower the next generation. Sezzle’s payment platform increases purchasing power for millions of consumers by offering interest-free installment plans at online stores and in-store locations. When consumers apply, approval is instant, and their credit scores are not impacted unless the consumer elects to opt in to Sezzle’s credit-building feature, Sezzle Up. This increase in purchasing power for consumers leads to increased sales and basket sizes for the more than 41,000 active merchants that offer Sezzle.

As the only B Corp in FinTech, Sezzle proves that all industries — even payments — can do their part to provide solutions and make a positive impact today and into the future. For more information visit Sezzle.com.

PYMNTS Intelligence is a leading global data and analytics platform that uses proprietary data and methods to provide actionable insights on what’s now and what’s next in payments, commerce and the digital economy. Its team of data scientists include leading economists, econometricians, survey experts, financial analysts and marketing scientists with deep experience in the application of data to the issues that define the future of the digital transformation of the global economy. This multi-lingual team has conducted original data collection and analysis in more than three dozen global markets for some of the world’s leading publicly traded and privately held firms.

We are interested in your feedback on this report. If you have questions

or

comments, or if you would like to subscribe to this report, please email

us at

feedback@pymnts.com.

Disclaimer

The FinTech Tracker® Series may be updated periodically. While reasonable efforts are made to keep the content accurate and up to date, PYMNTS MAKES NO REPRESENTATIONS OR WARRANTIES OF ANY KIND, EXPRESS OR IMPLIED, REGARDING THE CORRECTNESS, ACCURACY, COMPLETENESS, ADEQUACY, OR RELIABILITY OF OR THE USE OF OR RESULTS THAT MAY BE GENERATED FROM THE USE OF THE INFORMATION OR THAT THE CONTENT WILL SATISFY YOUR REQUIREMENTS OR EXPECTATIONS. THE CONTENT IS PROVIDED “AS IS” AND ON AN “AS AVAILABLE” BASIS. YOU EXPRESSLY AGREE THAT YOUR USE OF THE CONTENT IS AT YOUR SOLE RISK. PYMNTS SHALL HAVE NO LIABILITY FOR ANY INTERRUPTIONS IN THE CONTENT THAT IS PROVIDED AND DISCLAIMS ALL WARRANTIES WITH REGARD TO THE CONTENT, INCLUDING THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, AND NONINFRINGEMENT AND TITLE. SOME JURISDICTIONS DO NOT ALLOW THE EXCLUSION OF CERTAIN WARRANTIES, AND, IN SUCH CASES, THE STATED EXCLUSIONS DO NOT APPLY. PYMNTS RESERVES THE RIGHT AND SHOULD NOT BE LIABLE SHOULD IT EXERCISE ITS RIGHT TO MODIFY, INTERRUPT, OR DISCONTINUE THE AVAILABILITY OF THE CONTENT OR ANY COMPONENT OF IT WITH OR WITHOUT NOTICE.

PYMNTS SHALL NOT BE LIABLE FOR ANY DAMAGES WHATSOEVER, AND, IN PARTICULAR, SHALL NOT BE LIABLE FOR ANY SPECIAL, INDIRECT, CONSEQUENTIAL, OR INCIDENTAL DAMAGES, OR DAMAGES FOR LOST PROFITS, LOSS OF REVENUE, OR LOSS OF USE, ARISING OUT OF OR RELATED TO THE CONTENT, WHETHER SUCH DAMAGES ARISE IN CONTRACT, NEGLIGENCE, TORT, UNDER STATUTE, IN EQUITY, AT LAW, OR OTHERWISE, EVEN IF PYMNTS HAS BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES.

SOME JURISDICTIONS DO NOT ALLOW FOR THE LIMITATION OR EXCLUSION OF LIABILITY FOR INCIDENTAL OR CONSEQUENTIAL DAMAGES, AND IN SUCH CASES SOME OF THE ABOVE LIMITATIONS DO NOT APPLY. THE ABOVE DISCLAIMERS AND LIMITATIONS ARE PROVIDED BY PYMNTS AND ITS PARENTS, AFFILIATED AND RELATED COMPANIES, CONTRACTORS, AND SPONSORS, AND EACH OF ITS RESPECTIVE DIRECTORS, OFFICERS, MEMBERS, EMPLOYEES, AGENTS, CONTENT COMPONENT PROVIDERS, LICENSORS, AND ADVISERS.

Components of the content original to and the compilation produced by PYMNTS is the property of PYMNTS and cannot be reproduced without its prior written permission.

The FinTech Tracker® Series is a registered trademark of What’s Next Media & Analytics, LLC (“PYMNTS”)."