Artificial intelligence has crossed a threshold that few digital behaviors reach. It is becoming the starting point for everyday life. Consumers are not merely “trying” AI—they are using it to plan, learn, shop, decide and move closer to transacting. As a result, the traditional consumer journey of search, browse, compare and purchase is giving way to a conversational AI-mediated journey where intent is expressed once and then refined in the resulting dialogue. PYMNTS Intelligence data suggests that this shift is already evident in reduced reliance on traditional search and in the growing tendency to begin tasks within dedicated AI environments.

AI adoption is now mainstream, but the economic impact will be determined by where consumers start, how fully the technology replaces old habits and which payment rails can be trusted within AI experiences. More than six in 10 consumers used dedicated AI platforms in the past year. However, behaviors diverge sharply by generation and intensity of use. Dedicated AI platforms (e.g., ChatGPT, Claude, Perplexity, Gemini) are becoming “first stop” tools for Gen Z and Power Users. These consumers are significantly more likely to reduce search usage and replace prior search methods. Finally, consumers signal that digital wallets are the most credible bridge from AI engagement to secure commerce.

These are just some of the findings detailed in “How AI Becomes the Place Consumers Start Everything,” a PYMNTS Intelligence exclusive report. This installment of the Agentic AI Report Series examines consumer adoption of agentic and generative AI across 54 personal-use cases in nine areas of daily life. It draws on insights from a survey of 2,113 U.S. adult consumers conducted from October 14, 2025, to October 29, 2025.

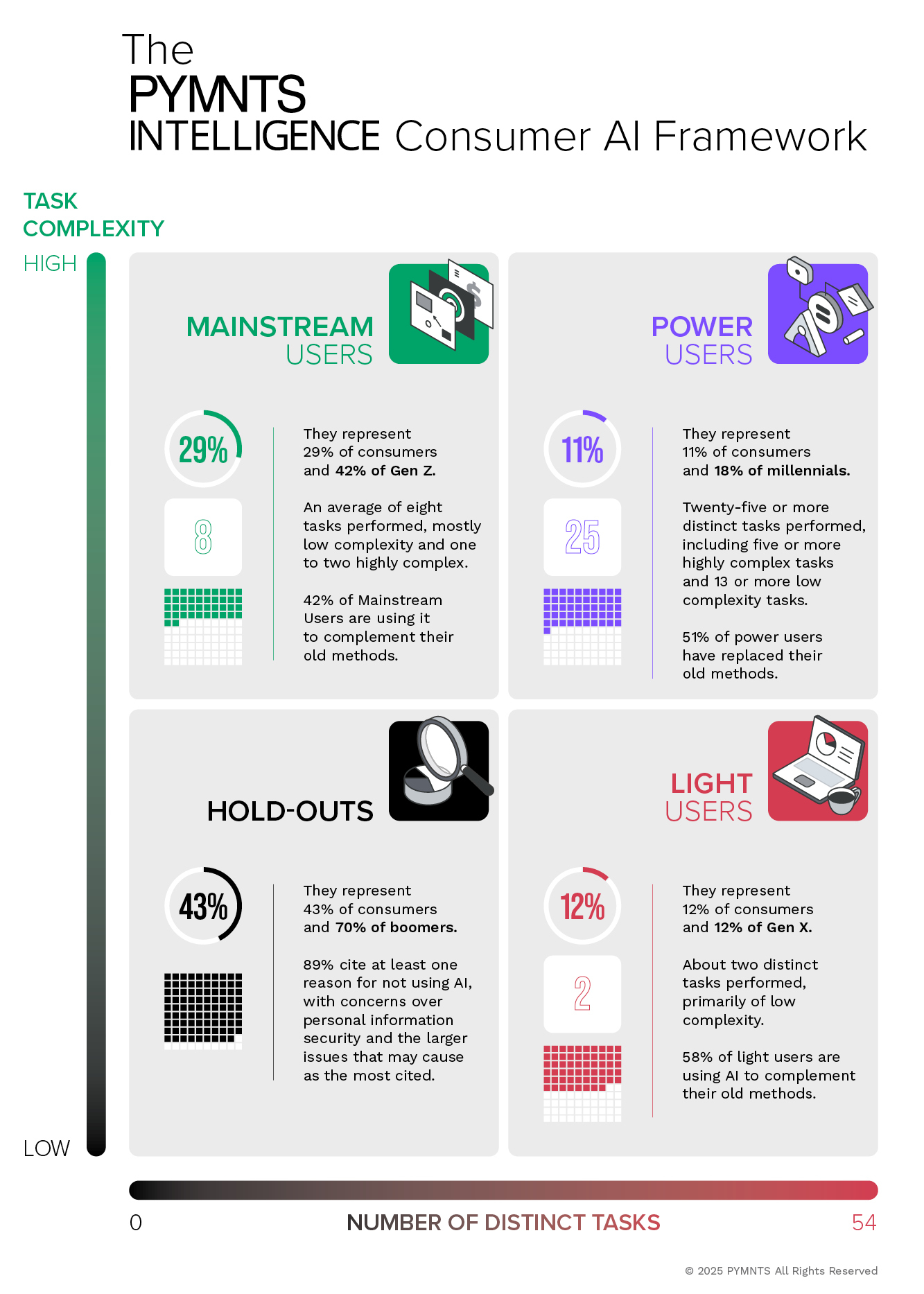

The PYMNTS Intelligence Consumer AI Framework Matrix

PYMNTS Intelligence assesses consumer AI adoption through a task-based framework spanning 54 activities across nine areas of daily life. These include shopping, finances, health, education and travel. Each activity is weighted to reflect the model sophistication required for reasoning and accuracy, the perceived risk to the consumer if the technology is wrong and the sensitivity of the personal information required to complete the activity.

This scoring yields four consumer personas mapped along two dimensions: task complexity and the number of distinct AI tasks performed. At one end are holdouts, i.e., those who do not use the technology and cite concerns about personal information as a key reason for non-adoption. The framework infographic also indicates that holdouts are concentrated among older cohorts. At the other end are Power Users, defined as consumers who perform 25 or more distinct tasks, including higher-complexity use cases. They are the earliest indicators of how AI can reorganize commerce, banking and decisioning. Between these poles are Light Users (limited, low-complexity use) and Mainstream Users (moderate breadth, typically low complexity, with selective, higher-stakes use).

Personal Tasks Drive AI Use

Personal tasks are the primary driver of consumer AI use, and Power Users deploy the technology across nearly every use case.

AI has entered the mainstream. More than six in 10 consumers used dedicated AI platforms in the past year. Usage is now broad-based, though uneven across age cohorts. Gen Z shows the lowest resistance to trying the technology, with 71% having experimented with it. Millennials stand out as the heaviest users, with nearly one in five qualifying as Power Users.

The intensity gap matters. Power Users extend the technology across shopping discovery, planning, learning and wellness. They effectively use it as a generalized personal operating system. Light Users cluster in lower-risk categories and remain cautious on higher-stakes activities such as financial tasks. Just 14% of Light Users report feeling comfortable using the technology for financial or banking tasks. The implication for financial services is not that “everyone will bank with AI tomorrow,” but that a measurable segment is already building the behavioral muscle memory that will normalize AI-mediated financial decisioning once trust, accuracy and user experiences mature.

AI Platforms Have Become the First Stop

Dedicated AI platforms are becoming the “first stop” for completing personal tasks, especially among Gen Z and Power Users.

The most consequential behavior change is not adoption alone; it is sequence. More than one-third of Gen Z consumers and Power Users turn to a dedicated AI platform as their first tool when tackling personal tasks. This “AI-first” behavior is accelerating. In just one month, reliance on dedicated AI platforms increased 36% among Gen Z and 28% among Power Users, signaling a shift in how these groups navigate information and decisions.

For digital economy executives, the strategic significance is clear: The front door is moving. When the technology becomes the default starting point, traditional acquisition and discovery levers such as search engine optimization (SEO), app store optimization and even comparison-shopping flows face structural headwinds. Winning attention increasingly depends on whether a brand’s offers, policies and product truths can be interpreted and recommended inside conversational environments. For financial institutions, this also raises a distribution question. If consumers begin with a neutral AI platform, banks and FinTechs must ensure they remain the trusted endpoint for advice, account actions and dispute resolution—even when the “conversation” started elsewhere.

AI Platforms Are Reforming Habits

Dedicated AI platforms are more likely to displace legacy behaviors than AI-generated search summaries.

The report highlights a widening behavioral gap between consumers who encounter the technology through dedicated platforms versus those who primarily use AI-generated summaries within search. Think Google Gemini versus Google AI Overviews. Dedicated AI platform users are 27% more likely to report reduced reliance on search engines, with 42% saying they now use search less, versus 33% among those who start with AI summaries in search. This is a meaningful signal that dedicated AI environments are beginning to supplant traditional discovery, not merely augment it.

Replacement rather than supplementation appears to hinge on the environment. Among consumers who primarily use dedicated AI platforms, 43% report fully replacing older methods. For those relying on AI-generated search summaries, 59% say they complement, not replace, prior habits. Light Users illustrate how this substitution may expand. They are most likely to replace old approaches to writing and communication and shopping discovery. The data indicates month-over-month acceleration in those low-risk categories.

Yet the path to deeper usage remains gated by trust and usability. The most common friction points center on privacy and the model’s limited understanding of user intent—barriers that directly constrain higher-stakes use cases, including financial decisioning and payments.

Digital Wallets Are the Gateway to AI-Platform Payments—For Now

Digital wallets are emerging as the most trusted bridge between interactions and payments.

If the first half of the AI shift is about discovery and decisioning, the second half is about closing the loop. That means converting engagement into secure transactions. In a phrase, it’s agentic AI. Consumers are already signaling how they want this to happen. One-third prefer linking a digital wallet to an AI platform for safer, easier payments. “Redirect to a merchant site” ranks second. Notably, this wallet preference extends beyond the most committed users, suggesting that wallets may serve as the trust layer that makes AI-mediated commerce viable at scale.

For financial services and payments leaders, the message is pragmatic. The winning design is unlikely to be “store your card inside an AI app.” Instead, consumers lean toward mechanisms that preserve control of sensitive personal data and rely on existing trusted authentication and tokenization flows. Those are the core strengths of modern digital wallets. As AI assistants facilitate more of the shopping journey, the wallet becomes the point of continuity between “intent expressed in AI” and “payment executed safely.”

Opportunities and Implications

Three implications stand out for executives designing consumer-facing AI in financial services and the broader digital economy.

Treat AI as a new distribution layer, not a feature.

The fastest-changing behavior is “AI-first” starting points, particularly among Gen Z and Power Users. When one-third of key cohorts begin in dedicated AI platforms, providers must architect for discovery in conversational ecosystems and defend relevance when consumers do not begin in owned channels.

Segment by actions, not demographics

The framework personas translate directly into product strategy. Power Users are already normalizing cross-domain usage, making them ideal for piloting higher-value, higher-trust services (e.g., financial guidance, proactive alerts, agentic workflows) with tight guardrails. Light Users are telling companies where to start: low-risk tasks that deliver immediate utility and reinforce trust. Holdouts are not a lost cause. They represent a design mandate. Privacy, transparency and control are central to unlocking the next wave.

Build trust and payment pathways as first-class capabilities.

Consumers cite privacy and misunderstandings as the chief barriers, even as adoption grows. In financial services, that translates into concrete requirements: explainable outputs, clear data-handling disclosures, user-controlled permissions and escalation paths when the model is uncertain. On the commerce side, digital wallets are the most credible bridge to AI payments, offering a low-friction, trusted channel that aligns with existing consumer expectations for safety and convenience.

One practical way to synthesize this message could be as simple as recognizing that AI users are not a single market. Power Users will pull the technology into high-stakes domains sooner and will reward seamless integration. Mainstream Users will scale usage when outcomes are reliable and workflows are integrated. Light Users will adopt in narrow slices where the value is obvious and the risks are low. Holdouts will move only when transparency and control are nonnegotiable design defaults. These differences should shape product roadmaps, risk models and go-to-market plans as much as they shape UX.

Conclusion

Consumers are steadily shifting toward an AI-first way of navigating daily life. Prompt-based AI is beginning to replace both traditional search behaviors and long-standing routines. Even Light Users are showing month-over-month growth in the simplest, most intuitive tasks.

For leaders in financial services and the digital economy, the competitive challenge is no longer whether consumers will use AI. It is where the technology will sit in the journey, which experiences will earn trust and which rails will carry payments. The next phase of adoption will be won by companies that design for segmented user maturity, build defensible trust through transparency and control and embed seamless wallet-based pathways that allow AI-assisted intent to become secure transactions.

Methodology

“How AI Becomes the Place Consumers Start Everything,” a PYMNTS Intelligence exclusive report, is based on a survey of 2,113 U.S. adult consumers. Conducted from October 14, 2025, to October 29, 2025, the findings examine consumer adoption of agentic and generative AI across 54 personal-use cases in nine areas of daily life. The survey sample was balanced to match the U.S. adult population in key demographics.