Consumer sentiment is often reduced to a single headline number, a pulse check on how Americans feel about the economy at a given moment. But for retailers and other businesses navigating an uneven landscape, those feelings alone are not a comprehensive enough indicator. The inaugural PYMNTS Consumer Expectations Index (PCEI) moves beyond traditional confidence measures to capture something more actionable: whether households not only feel optimistic but also think they have the financial capacity and job security to translate that sentiment into spending.

The PCEI is a monthly, survey-based index designed to quantify U.S. consumer sentiment in a way that is directly interpretable for commercial decision-making. It builds on traditional sentiment measures (household finances, economic outlook and purchase climate) while extending to include variables that also shape spending behavior (debt manageability, savings capacity, emergency readiness and labor-market security).

Sentiment, after all, only drives behavior when households have room to act. The PCEI maps confidence, constraints and job risk into a clear 0-100 index that illuminates what’s next for spending. The higher the index score, the greater consumers’ overall confidence.

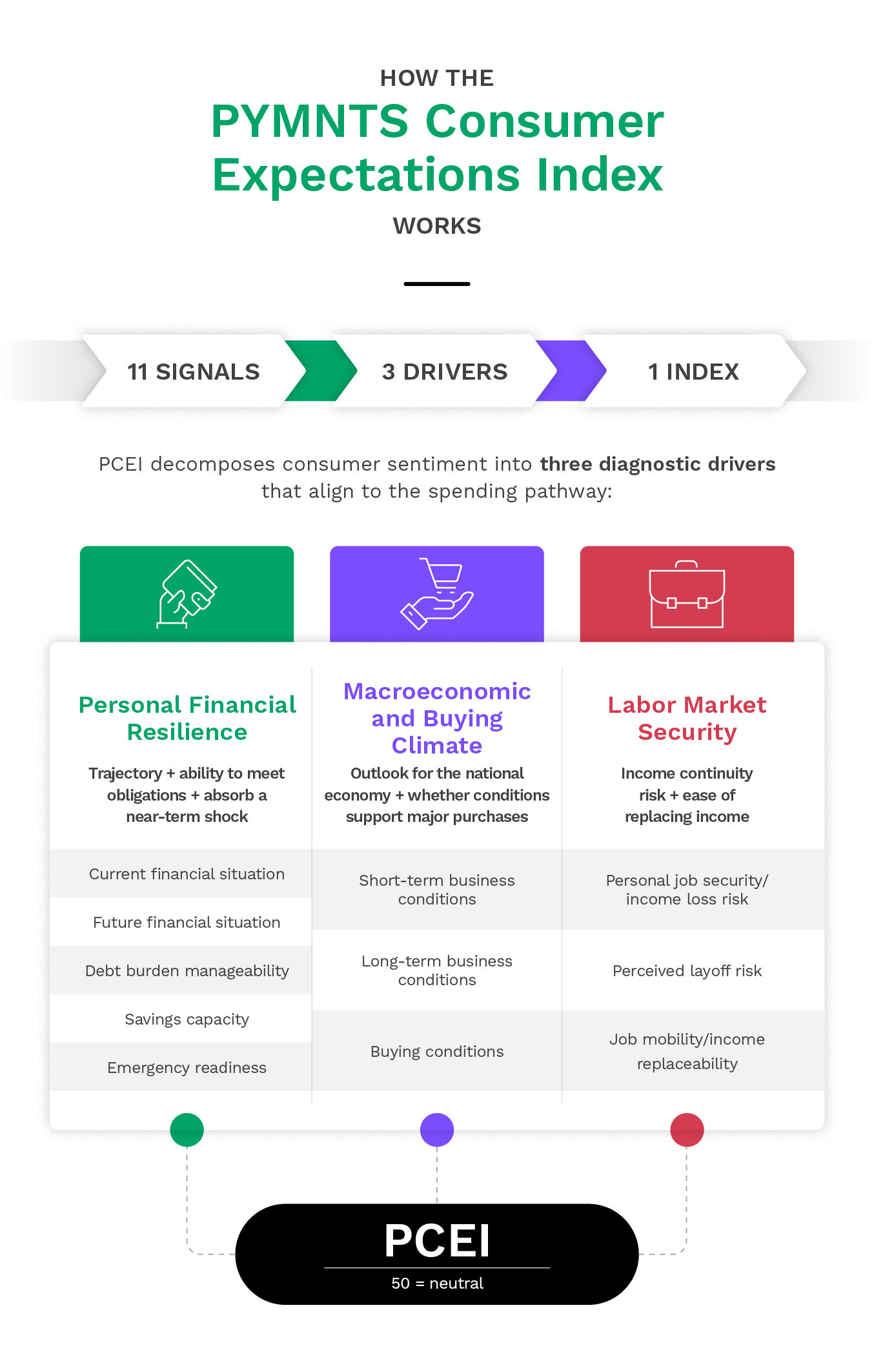

The PCEI is organized into three subindices—Personal Financial Resilience, Macroeconomic and Buying Climate, and Labor Market Security—that are combined into a single 0-100 index (50 = neutral).

- Personal Financial Resilience: Consumers’ perceived financial trajectory and capacity to meet obligations, maintain a buffer, and absorb a near-term shock.

- Macroeconomic and Buying Climate: Consumers’ outlook for the national economy and whether they feel like it is a good time for major household purchases.

- Labor Market Security: Perceived income continuity risk and confidence in replacing income if disrupted (including equivalents for self-employed respondents).

Those three drivers capture a consumer’s perceptions of 11 measures:

- Current financial situation

- Future financial situation

- Debt manageability

- Savings capacity

- Emergency readiness

- Short-term business conditions

- Long-term business conditions

- Buying conditions

- Personal job security/income-loss risk

- Perceived layoff risk

- Job mobility/income replaceability

Collectively, these subindices reflect consumer assessments of “Can I spend?” “Should I spend?” and “Will my income hold up?”

“Introducing the PYMNTS Consumer Expectations Index” is based on a survey of 2,304 U.S. adult consumers conducted from Feb. 6, 2026, to Feb. 12, 2026. It examines consumer sentiment along 11 key dimensions.

Living in Different Worlds

Financial lifestyle is a dominant driver of PCEI readings.

The financial lifestyle a consumer lives creates a large, persistent gap in PCEI readings over time. Consumers who do not live paycheck to paycheck remain solidly positive (index scores roughly in the low-60s), while those living paycheck to paycheck and struggling to pay bills stay deeply negative (index scores roughly in the low 40s). The group sits in between (index scores in the mid to high 50s), indicating meaningful dispersion in spending capacity and economic outlook.

Generational sentiment moves together, but millennials lead the pack.

Across generations, sentiment has followed the same pattern, softening last November, rebounding in December, easing in January and improving again in February. Millennials are consistently the most upbeat, rising to 60.7 in February, while baby boomers and seniors remain closest to neutral at 53.5. The spread between the highest and lowest cohorts is about seven points, indicating meaningful but not extreme generational dispersion relative to other cohorts.

Debt Confidence Is Strong, but Current Financial Conditions Lag

Households feel able to manage their monthly obligations but are less certain they’re better off.

Resilience is holding up overall, but the mix matters: Consumers feel strong confidence in managing debt, but their assessments of current financial conditions remain much closer to neutral. That divergence suggests that stability is being maintained through balance-sheet management rather than broad improvement in day-to-day financial circumstances. In practice, this pattern can be consistent with steadier spending in the near term, but it leaves less margin if prices rise further or households face new shocks.

Resilience is stable overall but splits sharply by financial lifestyle and gender.

Personal financial resilience is highly stratified by financial lifestyle across every month. Consumers who are not living paycheck to paycheck score around 69-73, while those living paycheck to paycheck and struggling to pay bills remain around 39-43, a 30-point gap that dwarfs differences by gender or generation. This pattern suggests that month-to-month movement in the headline resilience reading is more likely to reflect shifts in household cash-flow strain than broad demographic effects.

Cautious Spending Climate Masks a Two-Track Consumer Experience

The spending climate is improving but remains below neutral.

The Macroeconomic and Buying Climate subindex remains cautious, sitting below neutral in most months. It shows a notable improvement in December 2025 before easing again in January 2026. December’s uptick appears concentrated in short-term business conditions, while buying conditions remain the weakest component across the period. February shows renewed improvement, but the subindex still signals a consumer environment that is not yet broadly supportive of major purchases.

Consumers’ generally cautious macroeconomic and buying outlook masks sharp gaps by financial lifestyle and gender.

The Macroeconomic and Buying Climate subindex remains below neutral for the overall sample in every month except December, when expectations briefly reach neutral. The gap by financial lifestyle is large and persistent: Consumers not living paycheck to paycheck hover around 49-52, while those paycheck to paycheck and struggling to pay bills remain notably lower at 40-44.

A pronounced gender gap also appears, with men consistently near or above 50 and women materially below, indicating uneven confidence in the spending environment.

Workers Feel Secure, but Mobility Lags

Workers feel secure in their current jobs but are less confident that they can quickly replace lost income.

Labor Market Security is broadly positive, but weaker for Gen Z and financially strained households. In contrast, job mobility remains below neutral (mid 40s to 48), indicating that consumers feel safer staying put than switching. This combination supports steady spending in the near term but suggests limited flexibility if labor conditions weaken.

Labor security is broadly positive across the board, but weaker for Gen Z and financially strained households.

Labor Market Security is positive across most segments and improves into February for the overall sample. The largest separation is by financial lifestyle. Consumers not living paycheck to paycheck rise to 74, while those living paycheck to paycheck and struggling remain closer to 59. By generation, baby boomers and seniors trend highest (near 70), while Gen Z is consistently lowest (around 59-61), suggesting uneven confidence in income continuity across cohorts.

Conclusion

February 2026’s PCEI results reinforce a consistent theme: Expectations translate into spending power only when households think they have room to act. Across the index, the primary divider remains cash-flow strain. Consumers not living paycheck to paycheck report overall positive expectations (64.0), while paycheck-to-paycheck consumers struggling to pay bills remain firmly negative (44.5) a gap large enough to keep the “average” from describing the lived economy writ large.”

Methodology

The “PYMNTS Consumer Expectations Index,” a new PYMNTS Intelligence exclusive series, is based on a survey of 2,304 U.S. adult consumers conducted from Feb. 6, 2026, to Feb. 12, 2026. This report examines consumer sentiment along 11 dimensions. Our sample was balanced to match the U.S. adult population by age, gender, education and income.