There’s no way to sugarcoat it. To boil down the performance of the CE100™ Index, one word would suffice: underperformance.

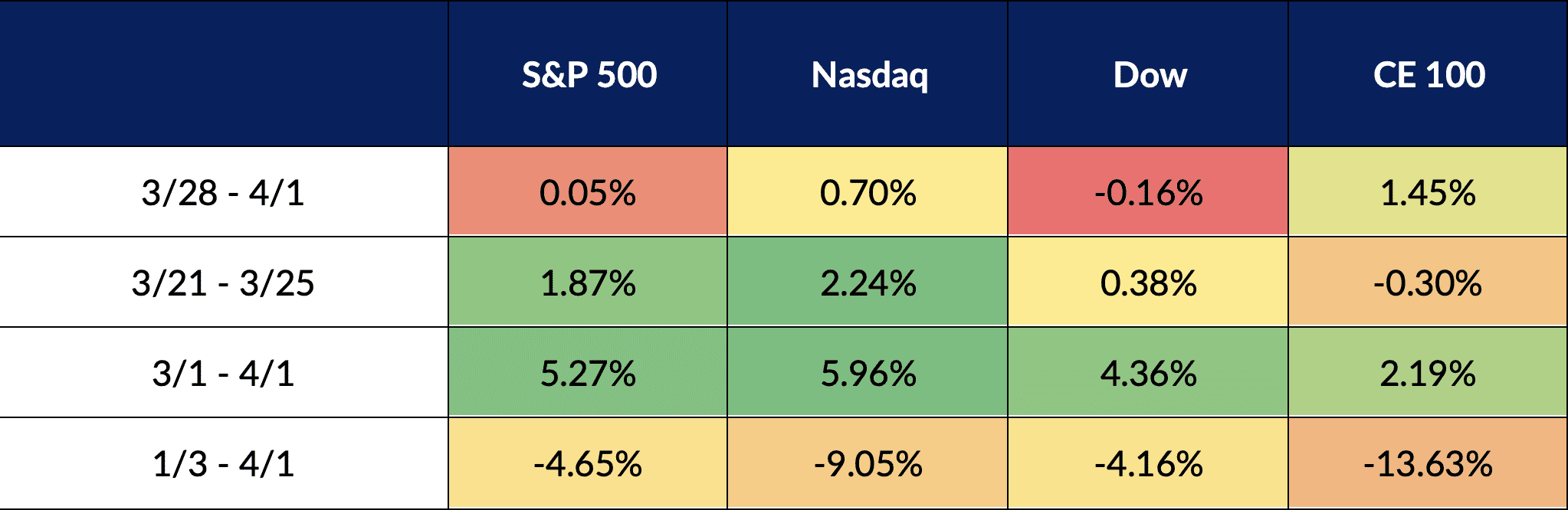

Through the first quarter, the Index was down just a bit more than 13.6% — significantly worse than the S&P 500 Stock Index, a broader measure of equities, and the tech-laden Nasdaq, which slid 9% on the quarter.

Things would be worse had it not been for the most recent week, which saw the CE100™ gain 1.5%.

We can see the relative performance in the table below.

CE100 Performance vs. Broader Indices

Source: PYMNTS

Source: PYMNTS

Drill down a bit and the overall performance for the quarter was dragged down by the Shop Index, which slipped 29%; the second worst-performing subset was the Have Fun Index, which was down 20%. The best performance was seen in the Be Well Index, which was still down, off 2.2% year to date.

In the past few days, we’ve seen a bit of resurgence of the enablers, where some names were up double digit percentage point gains. Fastly surged 12%, boosted by news that it acquired Fanout. Per the deal’s announcement this week, Fanout makes “a platform that makes it easy to build and scale real-time and streaming APIs such as live chat support, eCommerce, video streaming, gaming, collaborative editing and more.”

Those gains were offset a bit by Shopify’s decline, where the name sank by more than 9% on the week. As has been noted in recent weeks, Alphabet is reportedly making a deeper push into eCommerce.

The Bank Index, which is down 11% year to date, bears watching. In the past week, some of the marquee names in the sector have seen mid to high single digit declines. Citigroup slipped 7.8% on the week, and J.P. Morgan is off 14.1%. Notably, LendingClub has been one of the more significant laggards in the space, sliding 35% on the year so far.

It would be too simplistic to state that macro concerns alone are driving financial services names down. After all, in a period of rising rates, the conventional wisdom holds that banks (and other lenders) make more on the short term funds they lend out, while keeping rates paid on deposits relatively low. That asymmetry should keep net interest margins buoyant.

LendingClub, for its part, said this week that it it has helped over 4 million members since 2007, spanning “individuals who have obtained a personal loan, auto refinance loan, patient and education finance loan, or consumer deposit account.”

Read more: LendingClub Says It Has Exceeded 4 Million Members

Looking ahead, with the first quarter in the rearview mirror, we’ll start to see earnings reports detailing the state of the consumer and the interest they have in keeping things digital.

The banks and lenders will take note of consumers’ appetite to keep spending, and the restaurants and aggregators will discuss the interest in getting items delivered to the doorstep. Though economies are reopening, the urge to stay connected will likely prove to be persistent.