Given the money invested and work hours put in, the digital transformation of payments and the ecosystems connected by them is still in its early days, with some standout exceptions.

In the landmark 11-nation study “Benchmarking the World’s Digital Transformation,” a PYMNTS and Stripe collaboration, we surveyed over 15,100 consumers across 11 countries in January and February, analyzing how (and how often) consumers in key regions are engaging in 40 activities that comprise our 10 pillars of the connected economy.

What we learned is that the connected economy is still in its formative stages, albeit well-formed in some areas, but with many connections yet to be made to raise the average index score from its current 27.1 out of a possible score of 100 to reflect fuller transformation.

- An average of 19% (152 million) of those in countries studied are highly engaged in digital activities today, although nearly everyone has the digital tools to engage.

Even with 84% of the world’s population owning a smartphone, more than 80% having access to mobile broadband service and over 14 billion mobile connected devices worldwide, the study stated: “The biggest impediment to a country’s digital transformation is that there are too few people engaged in digital activities.”

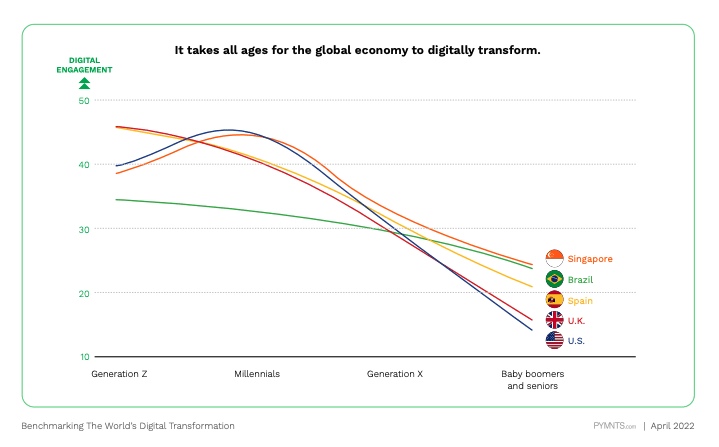

While millennials and Generation Z are seen as leading digital — and they do — the research found that “millennials, while important early adopters of online commerce, are not enough to bring about digital transformation; it requires the engagement of older generations to fully take hold.”

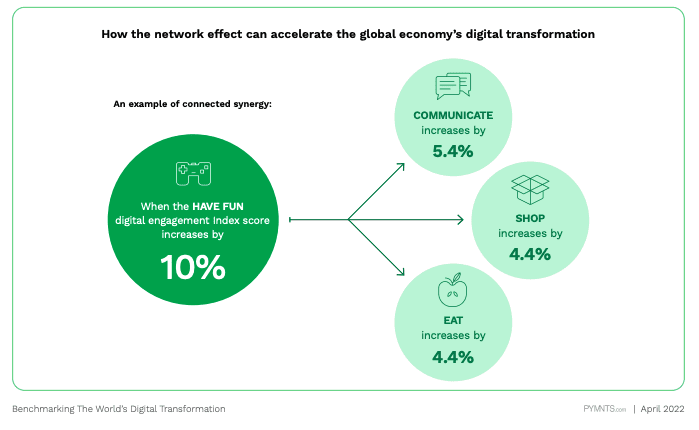

- Sixty percent of consumers who often engage in digital activities in the “have fun” pillar (video, music streaming) are highly engaged in the “communicate” pillar (messaging, social).

The connected economy enjoys flywheel effects of its own, as those who engage in activities in one pillar often find themselves seamlessly engaging in related but separate digital activities.

While six in 10 people streaming entertainment end up in social media and messaging apps as a result, we find examples throughout the study. For another example, 70% of consumers who said they’re engaging frequently digitally in the “shop” pillar “are also highly digitally engaged in the “eat” pillar (purchasing food from restaurants and grocery stores),” per the study.

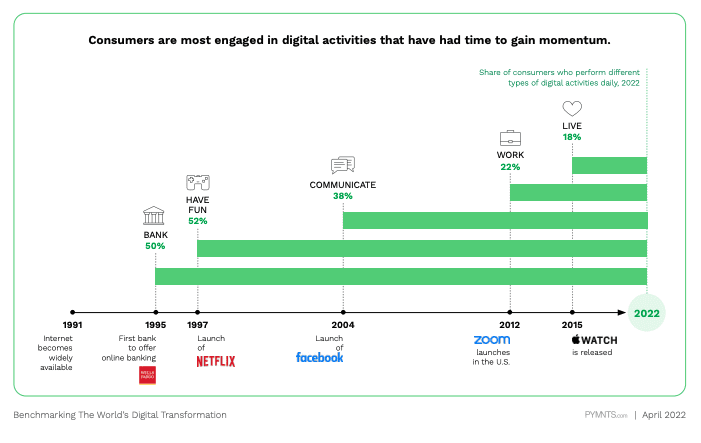

- 59% of consumers across all 11 countries engaging in mobile banking activities.

Clearly, the connected economy and the digital shift that it’s growing out of have growth potential to spare, yet some areas are already attracting high engagement, which spills over into others.

Finding 59% of consumers across all 11 countries engaging in mobile banking activities — with Singapore, Spain and the U.K. leading — “availability of attractive mobile banking alternatives to brick-and-mortar banking — coupled with the widespread availability of smartphones — drives both adoption and usage, and an increase in their overall CE Index ranking.”

Get the study: Benchmarking the World’s Digital Transformation