Small business is the lifeblood of the U.S. economy, and cash flow is the lifeblood of small businesses. Firms struggle when funds don’t reach their accounts in a timely manner. Silvana Hernandez, senior vice president of digital payments and labs at Mastercard, tells Karen Webster that rapid settlement can close the gap, letting firms deploy capital to grow — and send positive ripple effects through the economy.

It’s been said that small business is the lifeblood of the U.S. economy. And it’s been said, too, that cash flow is the lifeblood of small business.

Take that logic a step further — and small business cash flow, then, is the lifeblood of the U.S. economy.

But there’s a structural challenge in the mix, one that keeps cash flow from being a steady stream, and thus prevents companies from reaching their full potential.

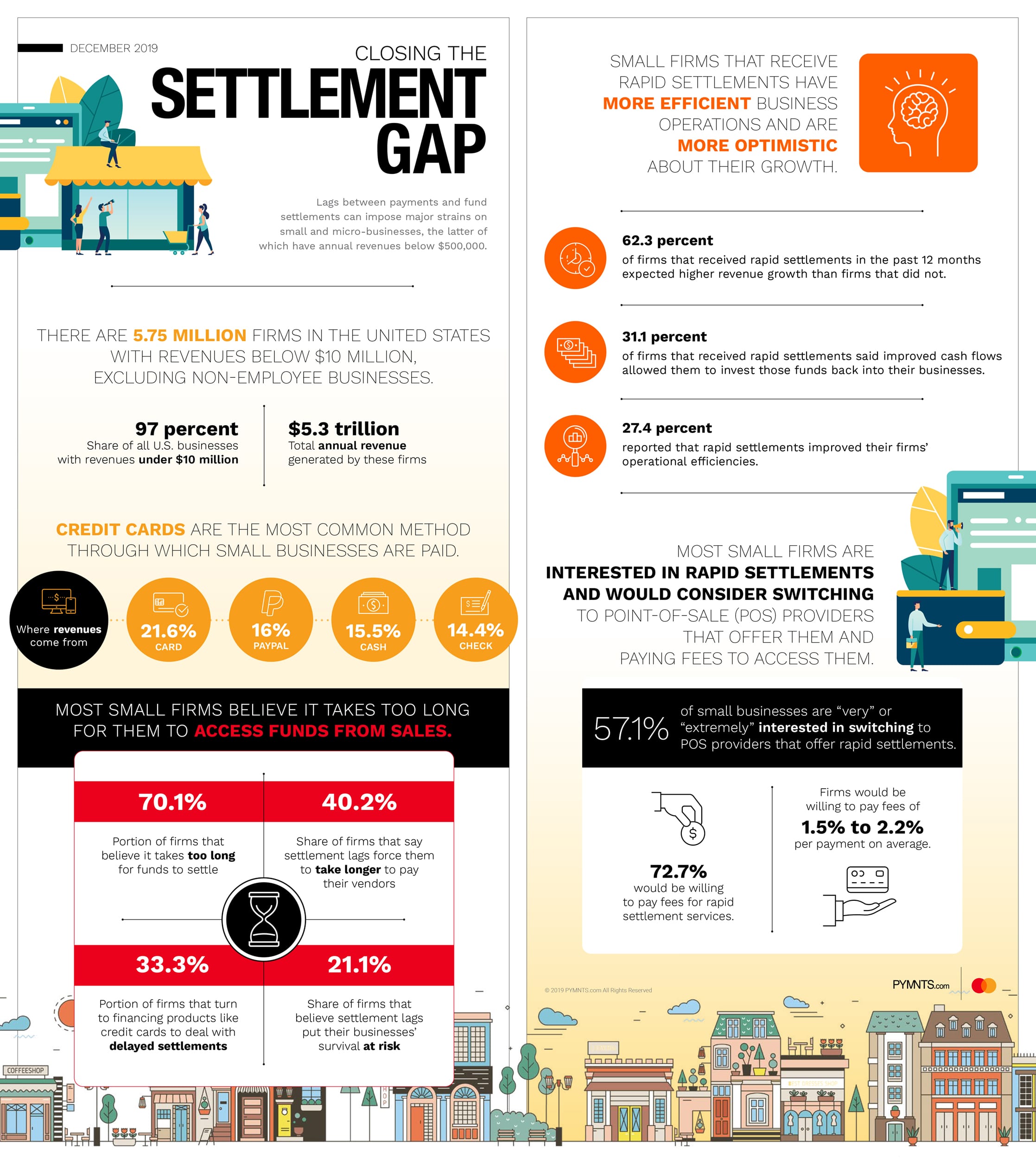

A recent Small Business Rapid Settlements study, done in collaboration between Mastercard and PYMNTS, finds that among more than 760 small- to medium-sized businesses (SMBs), more than 70.1 percent say it takes too long for funds to settle, which is felt when small business receive payments through checks or ACH. And nearly 66 percent believe it is “very” or “extremely” important for companies to have access to funds as soon as customers make payments.

As many as 47 percent of companies say they feel negative impacts if they don’t receive funds within a day.

The PYMNTS/Mastercard study hints at a larger issue: namely, that companies would benefit greatly from a more visible, and faster, flow of funds.

That is especially true against a backdrop where firms logging annual revenues of $500,000 to $10 million and micro firms (with sales below $500,000) number 5.75 million in the U.S. These smaller firms, as a group, account for the vast majority of companies in the U.S., at 97 percent of the total roster, and also generate $5.3 trillion in annual revenues. These are the firms that spur innovation, create jobs, pay wages, and, by extension, keep consumers’ pocketbooks full.

For smaller firms, especially, there are hiccups from the time it takes for the fruits of labor – a completed sale, in other words — to translate into cash in the bank.

In an interview with Karen Webster, Silvana Hernandez, senior vice president of digital payments and labs at Mastercard, said the joint study illustrates that the ability to manage cash flow is a constant concern for most small businesses.

“Cash flow is critical for businesses of all sizes, but especially for small businesses, because they struggle to have access to capital, and they also struggle to build and maintain cash reserves,” she told Webster. “So cash flow is really something business owners lose sleep over.”

Ideally, capital — replenished in a visible, reliable manner — gives firms the ability to manage inventory, hire staff and capitalize on growth initiatives, thus having a positive impact on the community at large.

Those sleepless nights can multiply when unforeseen external events require emergency outlays of cash to keep a business running — and the needed funds aren’t there.

Even strong sales may not translate into a steady stream of cash. We at PYMNTS note that revenues are an accounting construct, matching sales to expenses in any given period. It’s the days, weeks or months between invoicing and settlement that matter. (As they say on Wall Street, cash is king.)

How bad can it get? Consider the fact that, as the study shows, as many as one in five firms said the lag time between making the sale and getting proceeds into the bank puts the survival of their business at risk — an extreme example of the impact that looms when rapid settlement is not available.

To counter that lumpiness, executives usually resort to several tactics to smooth the funding gap — including taking out business or personal loans, or even charging business expenses to their credit cards. Of course, that’s assuming such funding mechanisms are on offer, and they may not be. As Hernandez stated, having to use alternative funding measures is a pain point for small firms, and was cited as a concern by a third of business owners. If such stopgap measures are not in place, noted Hernandez, vendors and employees might not get paid on time.

The Ripple Effects

The ripple effects of not being able to make timely payments can be long-lasting. Suppliers may think twice before taking orders from a company that cannot pay on terms. The workers who don’t get paid on time may move to more stable places of employment. The double whammy is that avenues of growth are effectively closed off for small businesses — the very same cohort that is responsible for two-thirds of job creation in the U.S. economy.

Among notable findings from the study, as called out by Webster: Brick-and-mortar firms do not have the same pain points when it comes to lag time between sale and settlement as their more online-focused counterparts.

According to Hernandez, online firms may have fewer expenses tied to physical stores, but they have relatively higher operational costs when it comes to consumer acquisition and order fulfillment.

One example of the vagaries of doing business online is that customers may buy two or three items from a company with the intention of keeping only one. The result is that the eCommerce firm has less visibility into final sales and cash flow, a scenario further compounded by the costs tied to offering free returns.

As Hernandez noted, there is a growing awareness of the need for (and availability of) rapid settlement when it comes to traditional payment methods. And Mastercard is partnering with financial institutions, businesses and service providers to enable rapid settlements for small businesses through their Mastercard Send push payments solution. As one example, she cited Mastercard’s partnership with Square to enable merchant rapid settlement for their sellers.

The Intangible Benefits

The availability of rapid settlement may improve cash flow. It also has the intangible impact of boosting morale. The PYMNTS/Mastercard survey found that more than 62 percent of firms that received rapid settlements in the past 12 months expected higher revenue growth than firms that did not. And about a third of firms that received rapid settlements said improved cash flow allowed them to invest those funds back into their businesses.

“When a business has sufficient cash flow and good visibility, they are more comfortable taking on new sales and new projects, or developing new products,” said Hernandez. Good cash flow visibility also translates into stronger relationships with vendors and employees.

Financial institutions and other financial services firms would do well to pay attention: Nearly 57 percent of SMBs would be interested in switching to point-of-sale (POS) providers that offer rapid settlement, and more than two-thirds of respondents would be willing to pay fees for those services.

For now, at least, rapid settlement represents a new revenue stream for providers. At some point, earlier access to capital will become table stakes.

“We are going to start seeing more acquirers and service providers innovating in this space and addressing this pain point,” Hernandez predicted. “Eventually, it’s going to be a feature they need to offer. And it’s no surprise that Mastercard is helping to lead the way.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More