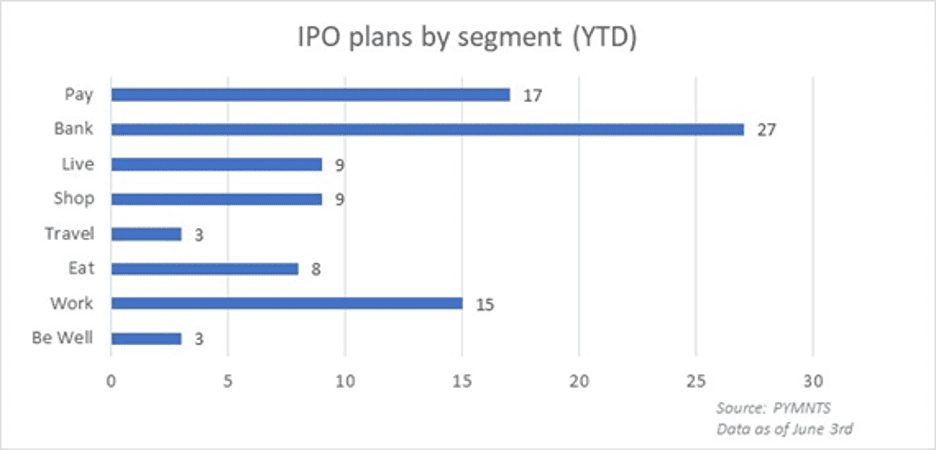

Amid a short market week in the United States (exchanges were dark on Monday, Memorial Day), new listings activity remained muted. Payment-related debuts year to date stand at 17, outpaced by banking at 27 initial public offerings (IPOs).

Among the companies that went public this week: dLocal, which focuses on cross-border payments in emerging markets, surged double-digit percentage points in its first day of trading, as spotlighted in this space.

Elsewhere, Marqeta, the payment card firm which offers a platform that uses APIs to streamline issuance, said this week that it priced it shares between $20 to $24 and plans to sell 45.5 million shares.

Looking internationally, in Turkey, the second largest eCommerce platform, as measured by market share, has applied to list in the U.S. on NASDAQ exchange. As noted by Yahoo Finance, Hepsiburada.com is formally known as D-Market Elektronik Hizmetler ve Ticaret AS. Terms of the listing — how many shares and the pricing of those shares — remain undisclosed.

Choosing Between SPACs And IPOs

Digging into the particulars of why some companies may choose one route toward listing over another — that would, of course, be the choice to undertake a “traditional” listing versus using a special purpose acquisition company (SPAC) — PYMNTS conducted an interview, via written exchange, with Marco Margiotta, CEO and founding partner of Toronto-based Payfare Inc.

Payfare, which is focused on instant payouts and digital banking for the gig economy, went public in March, raising gross proceeds of C$65.4 million.

Margiotta told PYMNTS that 2021 presented an opportune time for a digital banking firm such as Payfare to go public.

“The entire payments industry has witnessed a seismic shift in the last year to mass adoption of digital banking, payments and financial services. The global COVID-19 pandemic created a surge in demand for delivery,” he told PYMNTS, adding, “We learned that many gig workers are essential, as consumers stayed home and turned to online services to meet their essential needs like restaurant, grocery and even pharmaceutical delivery; providing transport to other essential workers,” among other activities.

In mulling its listing options, Margiotta said, Payfare examined both doing a SPAC and a direct listing, but said a traditional IPO “made most sense to us.”

SPACs can be useful, he said, if the right partner is found at an attractive price. A SPAC could also become a risk, he cautioned, “as a result of tying the listing to the closing of the SPAC transaction, whereas a path to an IPO can involve many different investors who could provide broader strategic value.” In reference to the traditional IPO, he said, shifting to online roadshows given the pandemic meant Payfare was able to capitalize on scheduling capabilities “without the inefficiencies” of traveling city-to-city across North America.

“I believe SPACs are gaining attention, but not necessarily all for good reasons,” the executive told PYMNTS. “There tends to be a negative connotation to SPACs versus a traditional IPO because of more speculative opportunities that seem to follow SPACs. One of the main benefits of SPACs is that they are less scrutinized and are typically quicker to get to market than a traditional IPO. In addition, there are usually less restrictive shareholder lockups for management and insiders.”

The proceeds raised in the offering, the company has said, will and are being used to pay down debt and finance growth and expansion initiatives. Digital banking for gig works is evolving at a rapid clip, he said, where larger platform providers and enterprises serving the gig economy are prioritizing the financial needs of their various workforce in a market that is worth, by at least one estimate, about $450 billion.

“For Payfare, we see digital bank accounts and instant access to earnings as the starting point for service offerings to the gig workforce,” he said. Pain points that Payfare has sought to solve include the fact that some gig workers, traditionally, have been offered ways to receive their earnings earlier through a third-party payment processor, but that option would be laden with fees that add up quickly.

Traditional bank accounts can be costly and are not always accessible to gig workers, he said, “leading them to turn to predatory check cashers and payday lenders to fill the gaps.” With a Payfare account, he said, gig workers — “who should be seen as entrepreneurs that require funds to do business” — have access to free ATM withdrawals, online bill payments, fund transfers and no minimum account balance requirements.