When eCommerce accelerated during the pandemic, merchants suddenly found they were acquiring more and more customers online — and they didn’t know them as well as their in-store customers.

“With that, we needed to come up with a solution that allowed an omnichannel experience that was secure and intuitive,” Martha Salinas, chief commercial officer at TreviPay, told PYMNTS.

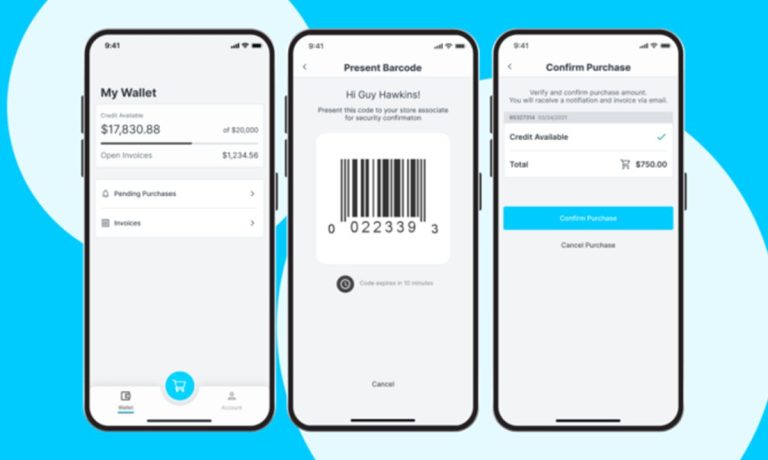

That solution was TreviPay’s mobile payment app, which is designed to give business-to-business (B2B) customers who purchase in-store an omnichannel experience. This one-click payment app for B2B buyers found its first partner in Staples Canada, which is now leveraging the offering in all its stores.

Giving Instant Data to Both Buyers and Merchants

Six months after the launch of the app, the mobile payment app is being used in 305 Staples stores in Canada.

“We are in conversations with other clients about leveraging the mobile app solution,” Salinas said.

For added security, there’s a multifactor authentication application so that when the buyer uses the mobile app at the store, it generates a code that the store scans in order to identify the customer at the point of sale.

Related: Could 2022 Be the Year of Digital Authentication?

Meeting Buyers Exactly How They Want to Buy

The app gives the customer access to a credit line immediately, without having to wait for a plastic card. The customer can use it immediately to buy online, in the store or by calling a salesperson.

It allows the merchant to offer these options without having to upgrade their point-of-sale (POS) system, and it provides a competitive advantage because the merchant can meet customers where they want to be in terms of payments.

“So, it is giving another tool to the buyer to meet them exactly how they want to buy,” Salinas said.

While the app is designed to be intuitive, clean looking and easy to use in order to bring a business-to-consumer (B2C)-like experience to the B2B space, it’s also as secure and robust as a B2B app needs to be.

“It needs to go beyond the B2C experience because in the B2B space, there’s more stakeholders, the credit lines tend to be larger and fraud is a little easier because the information about the business is more accessible and available to people,” Salinas said.

See also: TreviPay: 2021 Was the Year of Flow

Providing Flexibility for Both Merchants and Buyers

B2B programs also require flexibility, Salinas added. A B2B payments solution like TreviPay deals with both small- to medium-sized businesses (SMBs) and large enterprises, and each of those segments has different needs. They also deal with different verticals, and the needs of those in education may be different from the needs of those in manufacturing.

“We know that in B2B payments there’s no such thing as one-size-fits-all,” Salinas said. “So, for us, it’s very much about flexibility for both the merchant and the buyer.”

Looking ahead, Salinas said customer experience (CX) is going to become more and more important for all companies. Because people are doing more business online, it’s easier for them to switch to a different vendor or different merchant when they’re not getting the experience they want from their existing ones.

“That’s why not only the customer experience but having tools to track the customer experience and how happy your buyers and your merchants are, such as NPS and other tools, are paramount to making sure that you are providing the value to your merchants and your customers that you need to be providing as a payments solution,” Salinas said.