According to PYMNTS Intelligence, credit unions (CUs) and community banks continue to gain traction in the consumer credit card space.

As we found in researching “Credit Unions and Community Banks Gain Credit Card Issuing Momentum,” a collaboration with Elan Credit Card, where once 76% of consumers turned to national banks to issue their primary credit cards, now only about 68% do so.

In fact, our study — based on surveys with more than 2,000 consumers — found that 24% of consumers would, given the option, prefer that a more local option, such as their credit union or community bank, issue the main credit card they use.

This may come as a surprise to those who assume credit cards are the province of big banks. These big banks already manage the lion’s share of accounts and card issuance in the U.S., providing them with an inherent cross-selling advantage.

The numbers bear this out. Among those we surveyed who say they have one “go-to” card, 68% say their primary bank issued the card. CUs, meanwhile, manage 8% say their CUs issued their number one credit card. Community banks come in at a distant third, with about 5% of the primary card market.

This suggests credit unions and community banks are missing out on opportunities to convince their members and customers to let them issue their main credit card.

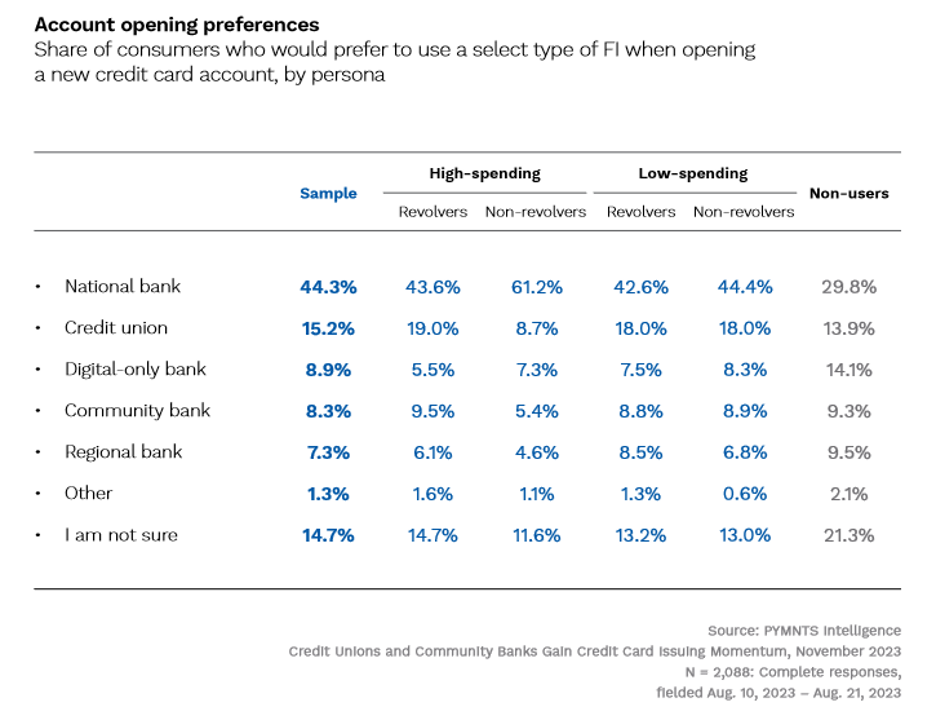

The missed opportunities become more apparent when looking closer at the data through the lens of the customer personas PYMNTS Intelligence generated. When asked which institutions they prefer to issue a new credit card, based on how they use their cards, the responses were revealing.

Less than 9% of “high-spending non-revolvers” — those consumers who pay for more than 40% of their total expenses using a primary credit card but rarely carry a revolving balance at the end of the month — would pick a CU to issue a new card. For community banks, the shortfall is more substantial, with just 5.4% of high-spending non-revolvers preferring community banks.

CUs perform best with high-spending revolvers — those who pay for more than 40% of their purchases with credit cards and usually carry a balance. Nineteen percent prefer credit unions to issue new cards. These are followed closely by the two low-spending personas, both of whom put less than 40% of their expenses on primary cards and either pay or their balances in full each month or not. Eighteen percent of low spenders prefer credit unions issue their primary cards. Nearly 9% of each segment prefer community banks.

National banks remain the goliaths of the consumer credit card industry, and their dominance will not likely be challenged any time soon. Nevertheless, CUs and community banks have gained significant momentum in the credit card space, and both institutions are well positioned to stake out a stronger segment of the primary credit cards market in years to come by simply becoming aggressive in the card marketing tactics.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More