In payments, the rebound in SPAC listings — if we can call it that — will likely be a short one.

We wonder: Is the spate of recent headlines surrounding payments firms and FinTechs and other digital upstarts coming public via these once-blistering-got vehicles a green shoot opportunity or simply the special purpose acquisition companies (SPACs) running to get deals done before the two-year clock runs out?

The jury’s still out, but if the past is prologue, a fizzling will be in the works.

Headlines through the past several days show several SPAC deals coming to market.

Coming to Market

As noted in this space, for example, GloriFi, a Dallas tech company that bills itself as “pro-freedom, pro-America, pro-capitalism,” is getting ready to go public in a blank check merger worth $1.7 billion. GloriFi is slated to merge with DHC Acquisition Corp., a SPAC.

Elsewhere this week, Plastiq Inc., the B2B payment platform focused on SMBs, said it had entered into an agreement to merge with Colonnade Acquisition Corp. II and then list its shares. As detailed by the companies, the implied estimated enterprise value of approximately $480 million at closing, which in turn equates to 6.4x forecasted net revenues of $75 million, and roughly 4.6x the forecasted $100 million in sales projected for next year.

There’s more: Global FinTech platform Seamless Group will become publicly traded through a combination with SPAC INFINT Acquisition Corp., the two companies announced Thursday (Aug. 4). The transaction puts Seamless at an enterprise value of $400 million.

The activity is not confined to the United States either. Global Star Acquisition has set its sights on FinTech and prop tech, with a focus on the Nordic and APAC regions. That SPAC has filed to raise as much as $80 million via a public offering.

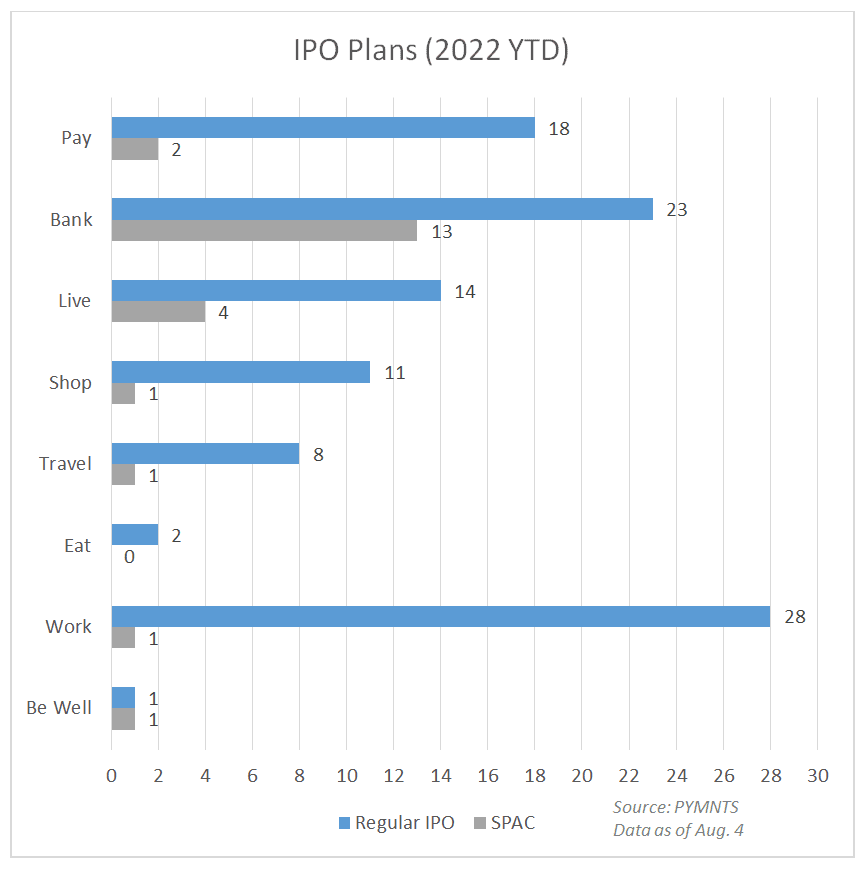

Drill down a bit, and the fact remains the headlines are but seeming blips in a trend that is pointing south. PYMNTS’ own trackers show that what we might term “traditional” or “regular” initial public offerings (IPOs) are far outpacing any blank check deals by orders of magnitude.

Chalk it all up to the fact that markets are still volatile and vulnerable. The headwinds are corroborated by the likes of CNBC, which stated that “the SPAC boom is officially a thing of the past.” There was not a single issuance on the public markets of a SPAC last month, said the financial news outlet.

The fundamentals and lure of FinTech, of the digital shift in payments, remain intact. We noted in coverage of Plastiq’s coming-to-market that the company estimates that 30%+ revenue growth lies ahead; and that its market penetration in B2B invoicing and payments is only a few basis points.

But as to taking these firms public, the traditional route may be the easiest path (with the caveat that market headwinds are tough to navigate). Recent, ongoing issues in the crypto space might be telling. As reported earlier in the year, crypto companies have been pushing back their target dates to list shares — and have been doing so because of a tougher regulatory environment.

Many blank check firms will soon bump up against their two-year investment horizons to get deals done. And regulations are changing. SPACs will have to disclose more details than they previously had to and rules would govern the ways they issue forward-looking projections for their businesses.

The bumps in activity we’re seeing right now, at least in SPAC-land, may be brief indeed.