There’s an old story, possibly apocryphal, where F. Scott Fitzgerald tells Ernest Hemingway: The rich are different from you and me.

Replies Hemingway: “Yeah, they have more money.”

The exchange springs to mind as buy now, pay later (BNPL) sweeps the globe, and is finding favor even with the wealthy. Budgeting and stretching payments out over time, it seems, has its appeal no matter the income bracket.

Unicorn in the Middle East

BNPL’s firm entrenchment in the payments landscape is illustrated by news that Saudi Arabia-based BNPL platform Tamara became that nation’s first unicorn. The company’s website shows that the BNPL model looks much the same as it does elsewhere around the world, as payments are split over four equal transactions. Brands tied to the option include Shein and IKEA. The digital conduits remain in evidence, too, as consumers complete their choice of payment terms and manage the payment plan through the Tamara app.

The company also has a presence in the United Arab Emirates and Kuwait.

Saudi Arabia is the leading global oil producer, and like any country, has a broad range of income distribution, as is the case with Kuwait and the UAE. According to data from global organizations, these are relatively wealthy nations. Saudi Arabia’s average annual income tops $27,000. In the UAE, the average income is nearly $49,000. In Kuwait, the figure comes to about $40,000 annually.

These numbers may pale compared to, say, the United States, where average income stands at about $75,000, per U.S. Census Bureau data. But they fall within the top 30 or so richest nations, and given the marquee retailers mentioned above, consumers have disposable income at the ready.

The Saudi central bank has been crafting regulations for BNPL providers in terms of capital requirements and has more than a half dozen BNPL firms operating there, indicating that the path is being paved for BNPL to gain a greater foothold.

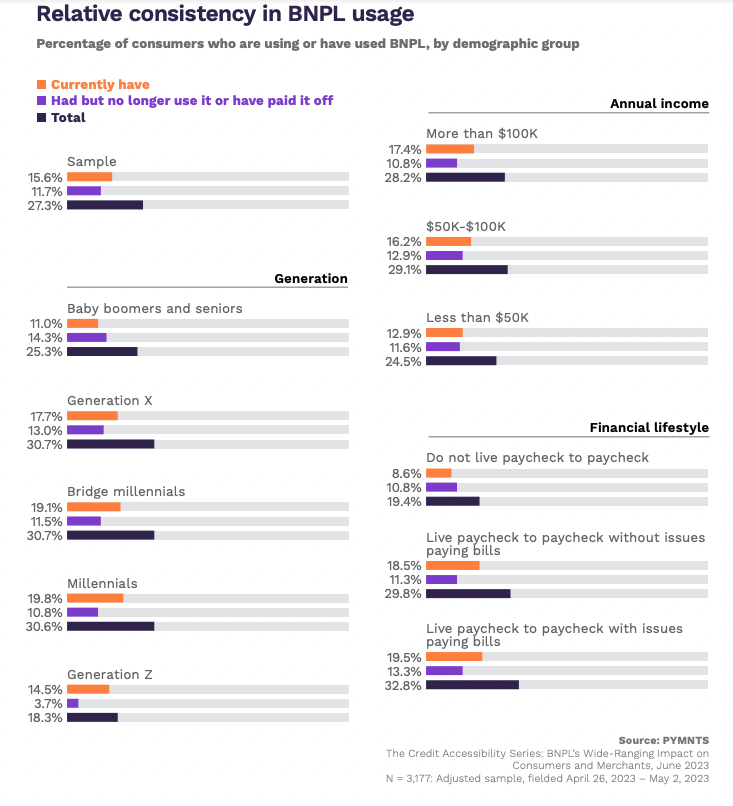

The growth of BNPL in relatively wealthier nations mirrors the trends seen in the U.S. “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants,” a PYMNTS Intelligence and Sezzle collaboration, found that 16% of overall consumers used BNPL, with a further 12% saying they used it at some point in the past. The usage skews higher for higher-income households, as of the cohort earning more than $100,000 annually, 17% have used the payment option and currently are using it.

A total of more than 28% of higher income earners have had at least some experience with BNPL, a bit higher than the average for the sample as a whole.