The pandemic has accelerated the digital roadmap for everyone in financial services, giving rise to more innovation in the past few months than had been seen over the course of several years.

And according to five observers across the spectrum of traditional financial institutions (FIs), payment networks and digital-only banks, opportunities are there for digital-first and hybrid models alike to succeed — so long as they harbor a relentless focus on identifying and solving customer problems. And, they said, traditional players can find competitive strength by linking up with firms that had previously been viewed as foes (that would be FinTechs).

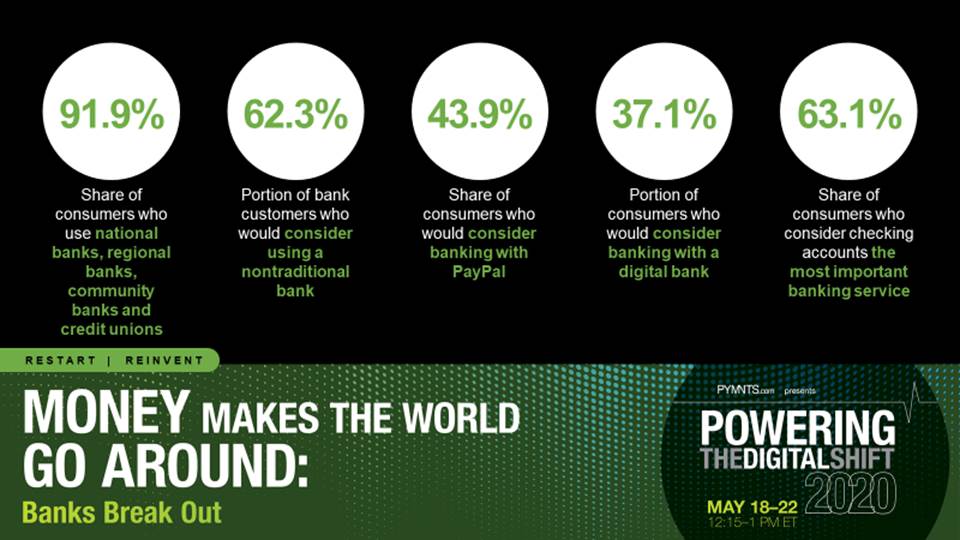

The panelists who joined Karen Webster for the discussion titled “Money Makes the World Go Around: Banks Break Out” included Clark Khayat, executive vice president and chief strategy officer at KeyBank; Zach Bruhnke, co-founder and CEO at HMBradley; Scott Zimmer, executive vice president, innovation and experience design officer, head of venture investing at Truist; Jess Turner, executive vice president, product and innovation at Mastercard; and Doug Brown, senior vice president and general manager at NCR Digital Banking.

For banks, the opportunity is there to cement the trust of their customers during uncertain times that have made individuals increasingly uncertain about personal health, job security, paychecks and even whether the money they have in the accounts is safe and sound.

At the same time, traditional FIs are facing competitive pressures from digital-only challenger banks that are looking to capture the attention of, and perhaps lure away, consumers.

The Great Stress Test

The pandemic, said NCR’s Brown, “is the ultimate stress test on every channel that a bank has to offer” — especially as measured across digital products and services.

“We saw things like digital interactive teller utilization going up by 550 percent, for example,” he told Webster, “and online and mobile banking spiking 300 percent to 400 percent in many instances.”

He noted that P2P payment volume moving across Zelle exploded, taking mere weeks to top what had previously been annual volumes.

That massive uptake in banking activity done in bits and bytes, he said, has come because of branch closures and social distancing requirements.

Digital-Only Players Take The Stage

The great shift has also opened up the playing field for challenger banks, relying on digital-only platforms upon which to build client relationships.

HMBradley launched high yield savings accounts and direct deposits at the end of March.

And as HMBradley’s Bruhnke told Webster, “I always joke that I don’t understand what traditional banking is. If you talk to a bank CEO, they will tell you that most of them want to grow deposits, unless you are big enough that you worry about allocating capital. If you talk to a consumer, most of them want to make money on their money.”

HMBradley offers FDIC-insured accounts through Hatch Bank based in California, and rates of about 3 percent on its savings accounts. The company also is aiming to launch “one-click credit,” consisting of pre-qualified offers to clients.

As evidence of the great shift to digital: Thus far, Bruhnke said during the panel discussion, the digital bank has seen almost as many customers signing up for its offerings born before 1970 as it has seen clients born after 1990.

Here, then, lies the challenge of the challenger banks: They’re poised to steal customers and deposits away from traditional players.

But maybe not — not if the FIs leverage the strengths they already have in place.

As NCR’s Brown contended: “Banks, community banks, Main Street banks and credit unions still have a strong value proposition to of their own when it comes to the relationship models that they have in their communities.”

Against that backdrop, he said, a number of NCR’s smaller banks have picked up a number of new business clients because those small- to medium-sized businesses (SMBs) have been largely overlooked by larger banks.

Drill down a bit, said Brown, and it has become apparent that despite the embrace of self-service options by necessity, consumers want to connect to bank employees as they navigate pressing needs like Paycheck Protection Program (PPP) loans and payment deferrals on, say, mortgages.

Keybank’s Khayat said the pandemic has “really caused us to get innovative and aggressive on setting up things that we did not have available” in terms of digital channels while bolstering already strong relationships.

As an example, he pointed to the PPP, which he said stands as a “fantastic version of what you can do in a really short period of time.” He noted that KeyBank has extended roughly 15 years’ worth of loans in a matter of weeks.

Pivoting To Partnerships

That’s not to say that traditional banking is immune from the pressures of digital-first and digital-only players. Banks are going to have to monitor and act on the digital pivot.

But they can’t do it alone.

For traditional FIs, agility is key, maintained Khayat. As far as how permanent the shift to digital might be, he likened the demand to a rubber band. A longer and more stretched out move to digital might mean that consumers will be loath to return to their old (physical) banking habits in the future.

“If we continue in this environment, we’re going to have to continue to be agile and not agile with technology, but agile in the business model,” he said.

Increasingly, in the jockeying to get new products and services to market, FIs are finding value in partnerships struck with FIs.

Mastercard’s Turner pointed to the collaborations between FIs and FinTechs as struck through Mastercard’s Accelerate Program, which she termed a “fast track” to innovation, such as getting people paid more quickly through digital disbursements. Improving liquidity has also been a key focus for smaller corporate clients, said Turner.

Keybank’s Khayat said the partnership model makes sense, both for his firm and for other traditional FIs.

“In many cases, we’ve decided, ‘Look, if we can’t build it all, and if somebody’s built a better mouse trap, why rebuild it?’ We’ll figure out a way to make a partnership,” he said.

Truist’s Zimmer said that the “new normal” of financial services in the wake of COVID-19 dictates that FinTech innovators are helping broaden the scope of what banks should offer to their consumer and corporate client bases.

Of the banks, he said, “people don’t always like to change, right? So, that’s one of the things you’re working against: mindsets.”

Challenger banks, he said, can help spur change, helping traditional FIs expand their horizons.

And while there has been an increase in what he termed mergers of equals in financial services (where two heritage banks combine), he said Truist is “looking to build things in house that can take on [HMBradley] and other challenger banks … and we’re looking to partner.”

As for worries about whether the bigger players are bearing down on challenger banks like HMBradley and looking to put them out of business, Bruhnke said that “anytime someone like Clark [at KeyBank] and Scott [at Truist] know my name, we’re doing OK.”

Moving Beyond Physical First

As banks navigate the movement beyond the physical branch, and move to digital-first channels, they have an opportunity to combine the tangible and digital channels into an effective hybrid as we move beyond the pandemic, said some panelists.

“There is still a ‘physical’ need,” said NCR’s Brown. “In healthcare, you still need to get to a doctor eventually and have a real interaction. Likewise, there is still a necessity in banking and money management that involves documents and other items.”

And, as Zimmer noted, the hybrid model represents a “changing frontier” where those FIs with the physical infrastructure in place, such as drive thrus, have the ability to be there for clients in safe and secure ways.

The pandemic is powering the digital shift, and we’re not on the other side of it yet, noted the panelists.

But as Zimmer stated, the opportunity is there for banks and challengers alike to find new ways to innovate and meet customers’ financial needs.

As Zimmer said, “You have to move quickly. You have to believe you can do what you didn’t think you can do. You’ve got to try, fail — and try again. At the end of the day, you watch, and you get better.”