Embedded finance is made possible by banking as a service (BaaS), a fee-based model that enables nonbanking entities to provide financial services to their customers through direct connection with banks via application programming interfaces (APIs). In effect, BaaS allows nonfinancial companies to “embed” banking products and services into their own user interfaces without having to become licensed banks themselves. It thus establishes the essential infrastructure for any company to become a financial service provider — both quickly and cost-effectively.

Partnerships allow traditional FIs to keep up with the digital transformation

Partnerships between traditional banks and FinTechs, as well as other nonfinancial entities, have become a key driver in the adoption of embedded finance. This is because banks often do not have the technological capabilities necessary to enable embedded experiences on their own. Many large banks, for example, still rely on inflexible legacy infrastructure that does not support BaaS, and upgrading can be costly.

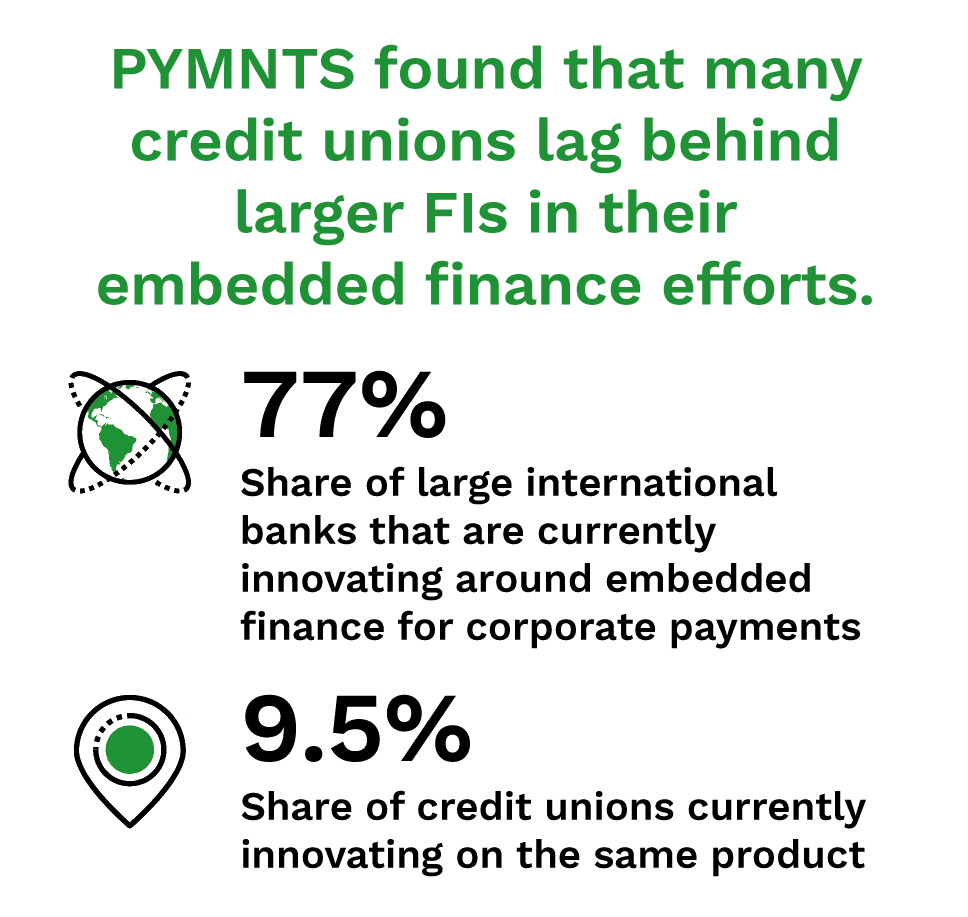

Small banks and credit unions (CUs) struggle to provide BaaS, too. Often hamstrung by a lack of funds and technical expertise, smaller financial institutions (FIs) are lagging behind their larger peers’ BaaS offerings and general digitization efforts. In a survey of leaders at small banks and CUs, 80% expressed concern that their clients will move to larger banks for better digital experiences, and 71% said their customers sought capabilities beyond what the institution’s infrastructure could support. As a result, these smaller organizations frequently look to partnerships to bolster their digital capabilities and keep up with larger banks.

The appeal of partnerships is that they enable traditional FIs to leverage the expertise, technology and customer base of FinTechs, while these tech companies gain comparable access to FIs’ banking infrastructure, licenses and knowledge. This can make it cheaper and easier to bring solutions to market for all parties, with one estimate determining that BaaS-using banks could cut the time to market of a new product by as much as 10 times.

BaaS can be leveraged to improve the customer experience and companies’ compliance needs

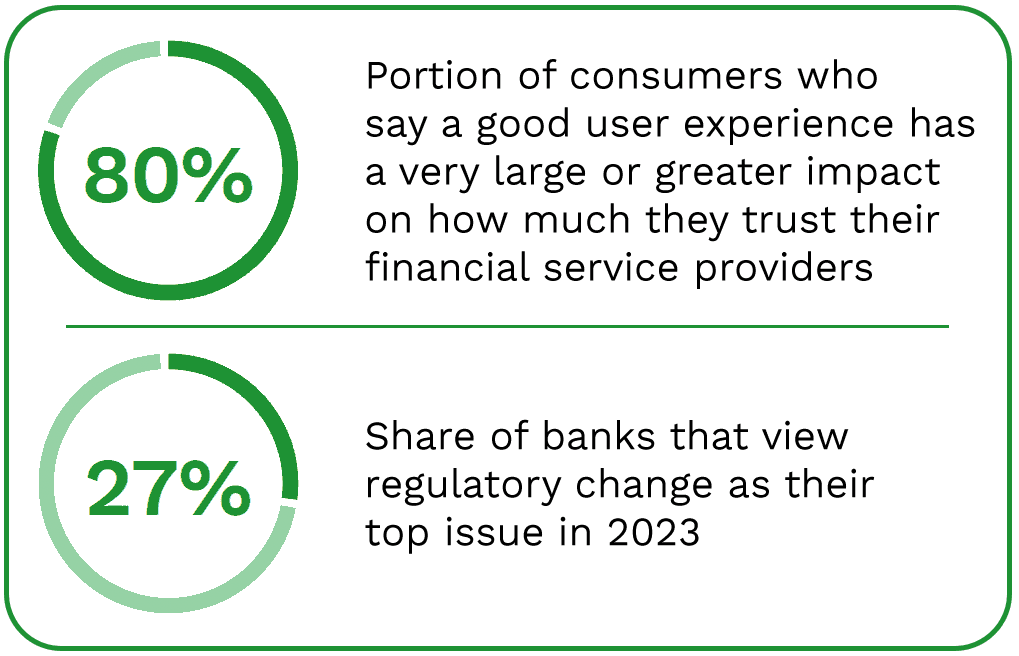

There has been such widespread interest in BaaS and embedded finance because they help address both customers’ and companies’ needs. One of the biggest benefits is improvements to the customer experience. Embedded finance creates smooth experiences in which customers can quickly get the services they need with ease. That matters, with almost 80% of consumers saying that solid user experiences have at least a very large impact on how much they trust their financial service providers.

For companies, higher levels of customer satisfaction can drive revenue and promote brand loyalty. Beyond that, though, embedded finance and BaaS can benefit companies in other ways. For example, BaaS providers are beginning to offer compliance as a service, which allows clients to avoid getting bogged down in onerous and ever-evolving banking regulations. BaaS can also be leveraged to prevent fraud, track consumer behavior and other helpful uses.