Online shopping has boomed over the past year, with consumers paying bills, buying necessities like groceries and making retail purchases digitally in higher figures. Forty million U.S. consumers reported shopping for groceries online in April 2020 alone, for example. eCommerce’s total retail shares expanded globally from 16 percent in 2019 to 19 percent by the end of 2020, according to a study released by the United Nations Conference on Trade and Development (UNCTAD).

This preference for digital shopping and payments appears to be expanding outside of the B2C world — notably, more companies are heading online to begin their sales relationships with new vendors or suppliers and to manage their payments. One of the key factors that appears to be helping to drive this growth forward is that many of those making B2B purchasing decisions at their firms are already used to making seamless digital transactions in other areas of their lives. A 2020 study found that more than 40 percent of millennial B2B buyers have a say in each step of the purchasing process, for example. As these digital-native buyers seek out new vendors or business partners, they are bringing their digital expectations with them.

Some challenges remain for companies looking to make the switch to digital-first B2B processes, however. The following Deep Dive examines how emerging trends and shifting preferences for B2C payments are influencing B2B payment approaches for businesses, focusing specifically on logistics and manufacturing firms — especially the smaller buyers. It also analyzes how automation, as well as flexible payment tools and technologies, can help these small buyers enhance their B2B payment processes to improve cash flow and the bottom line.

B2C Developments Fuel B2B Innovation

Many businesses have viewed digital payments as necessary for their continued survival. A recent study found that 98 percent of B2B manufacturers have already incorporated an eCommerce channel or plan to do so, with 45 percent of firms noting that boosting their sales was their main reason for doing so. The events of the past year pushed many of these entities to move much of their B2B processes online, with B2B eCommerce actually growing 200 percent faster than B2C eCommerce in 2020 as businesses across industries abandoned paper processes in favor of less cumbersome digital solutions. Many companies are now utilizing multiple sales channels to maintain their business relationships and conduct B2B payments, with digital sales becoming increasingly popular. Fifty-four percent of companies in the U.S. now place B2B orders via self-service websites, while 22 percent now do so through an online marketplace, for example. Only 16 percent of firms continue to place orders through brick-and-mortar locations.

This adoption of online B2B sales tools follows the path already laid out by B2C companies, with more consumers than ever now turning to digital channels first and foremost to make convenient routine purchases. The top 13 global B2C eCommerce companies reported that their collective gross merchandise volume (GMV) reached a value of $2.9 trillion in 2020, a nearly 21 percent increase from 2019 levels. These habits — which about one-quarter of consumers plan to retain for the foreseeable future, according to recent PYMNTS data — are beginning to filter into the ways many of them approach processes and payments as employees. Sixty-seven percent of all B2B buyers report having switched to purchasing from vendors that offer a “more consumer-like” experience, for example. This share is even higher among millennials, of whom 74 percent stated they had swapped vendors because the new company offered B2B experiences more similar to consumer payments.

The draw of consumer-like payments experiences for many companies appears to be the overall speed, convenience and personalization they grant shoppers. More B2B buyers are expecting to be able to browse through vendors’ products online without fuss, checking product reviews and other details before completing transactions. Companies have been moving steadily to nudge their B2B payment and sales processes to be more in line with B2C experiences for several years, but some — especially those in industries where such processes have traditionally been manual, such as manufacturing firms — are still facing challenges in doing so. Implementing automation, flexible payment tools and other key technologies into these processes is one way these firms, especially smaller manufacturing companies, may be able to cross that B2C-to-B2B gap.

Overcoming Manufacturing Firms’ B2B Innovation Challenges

Many manufacturing companies are still experiencing struggles when enhancing B2B processes to meet the current B2C-adjacent expectations of their buyers and partners. The U.S. steel and metals industry reported that 39 percent of total invoices were overdue at the time of the survey, for example. Smaller businesses in particular are still having difficulties collecting payments as they adjust their processes to digital channels, with over 60 percent of small to medium-sized businesses (SMBs) reporting that they routinely have their invoices paid late and 16 percent stating it can take more than a month for them to receive these payments. This can detrimentally impact cash flow, as 29 percent of these SMBs reported having to wait to finally gain access to their funds. One way to address these issues is by integrating automation into payments processes in a way that allows collections to be managed instantly.

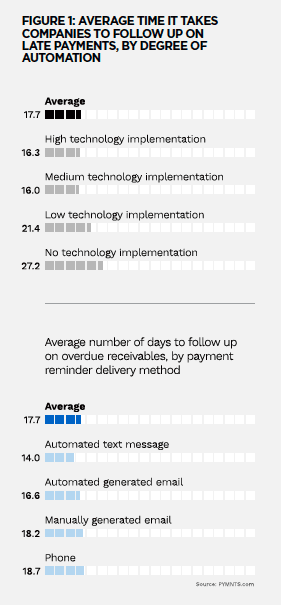

Recent PYMNTS data found that firms with a high degree of automation integrated into their AR processes typically take 16 days to follow up on late payments, far less time than the 27 days it takes those with no automation in these processes.

B2B firms of all stripes are also beginning to comprehend the importance of accepting credit card payments, which can help them flexibly adjust to the payment challenges they have encountered recently. Some B2B businesses have held out on accepting credit cards in an attempt to avoid the modest fees they charge, but many are beginning to change their tune because doing so could cost them sales in the era of eCommerce. Credit card acceptance can allow buyers to access one of their preferred payment methods as well as help their businesses expand. Sellers, on the other hand, get a better handle on their cash flows by gaining faster access to their payments.

Cutting down on payments time frames can help inch small buyers’ B2B experiences closer to the B2C-like interactions many are now expecting, allowing them to better compete. Failing to do so raises the potential for these companies to fall far behind other entities, especially as digital becomes the norm not only for consumer transactions but also for all types of commerce.