Pandemic-driven shifts in consumer needs have prompted players in the global financial sector to take a second look at how they are managing payments.

What has come into focus is that U.S. banks, businesses and even government entities still lean heavily on outdated legacy methods for disbursements. PYMNTS research shows that only about 29 percent of payments to U.S. consumers use speedier methods, such as same-day ACH, with most made by far less instant means, including cumbersome debit cards and paper checks that can take weeks to arrive in the mail.

The crisis and its related economic pressures have spurred not only a need to reduce reliance on these legacy methods but also a growing familiarity among U.S. consumers with instant disbursements. Consumers are becoming more likely to request instant payments when they know they are available, for example, with PYMNTS data finding that nearly 40 percent of consumers are either “very” or “extremely” likely to choose this method when it is offered.

Nordic countries such as Norway and Denmark have brought instant, digital payments into the financial mainstream and have valuable lessons to offer U.S. entities seeking to meet consumersʼ needs as they shift in this direction. The following Deep Dive explores the Nordic regionʼs progress in the use of instant payments and the challenges U.S. entities must confront to make this transition themselves.

The Nordic Instant Payments Approach

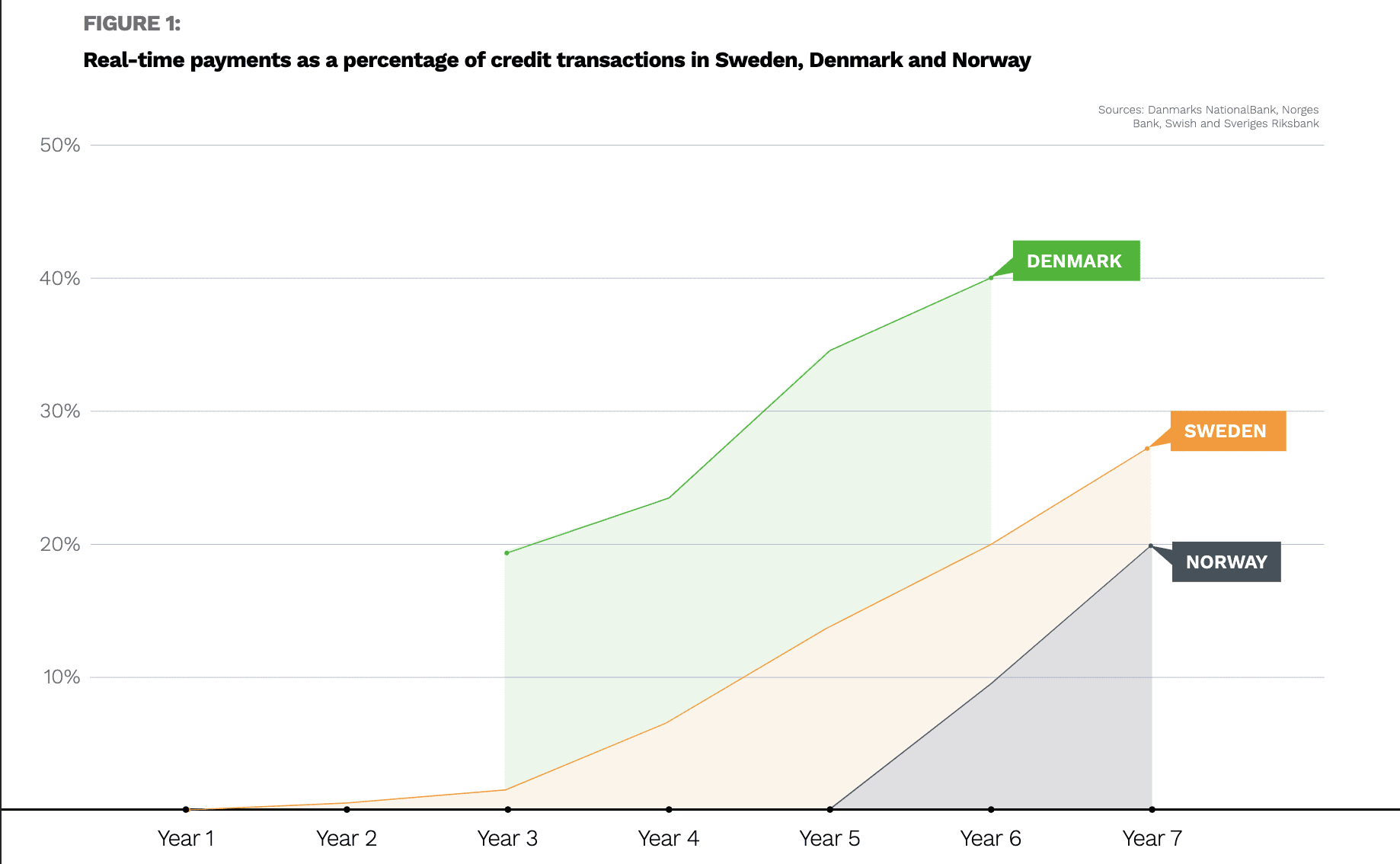

Nordic payments have been a subject of scrutiny for several years, provoking interest from financial entities worldwide. Instant payment solutions have been available for consumer use in the region for nearly a decade and have experienced rapid adoption during this time, with one report finding that the percentage of credit card transactions made with instant payments has steadily increased since 2013.

A critical point to note is why these solutions were so quickly adopted, which is closely tied to the reduction of cash use in the Nordic region. Many Nordic countries — with Sweden leading the group — have been working toward becoming cashless societies, and instant payments are crucial to successfully achieving this.

Cash use in such countries rapidly decreased over the past half-decade, representing only 1 percent of the total value of payments in Sweden as far back as 2016, for example, and leading many to claim that the country represents the worldʼs first cashless society.

A study from November shows Norway is close behind, with cash use now representing only 4 percent of its total payments volume. Mobile payments have equally taken flight in the Nordics, with 90 percent of consumers in Denmark now using Danske Bankʼs MobilePay app, for example.

Nordic financial players also gained support for instant payments as part of their overall cashless strategy in two distinct ways: by targeting businesses and consumers in their own countries, and by collaborating with other Nordic institutions for payments on an international scale. The initial creation of pan-Nordic instant payments service P27 by six of the regionʼs top banks in 2019 is one of the main developments that has placed it as the cashless vanguard, for example.

These countries also developed mobile and digital solutions geared toward their citizens, familiarizing consumers with these paymentsʼ capabilities. Applying a similar tactic may be one way that U.S. entities could integrate these solutions further into the financial foreground within the next few years.

Making Instant Payments Mainstream

The main strength behind Nordic countriesʼ instant payments adoption appears to be the cooperation among banks, FinTechs and lawmakers toward the common goal of becoming cashless nations, which encouraged innovation. Fostering this type of collaborative environment is crucial, but U.S. entities seeking to further instant payment adoption must also take note of consumersʼ role.

Consumer support for these developments played a critical part in entrenching instant payments in the Nordic financial world. U.S. consumers are increasingly requesting instant payment capabilities, but data also reveals a significant number of citizens who remain unfamiliar with them. The next key challenge for U.S. entities is thus twofold: to create the necessary infrastructure to support instant payments, and to educate and familiarize consumers with their benefits. Lags in either area could see the U.S. fall behind other markets in the instant payments race.