The high cost of health care is leading many consumers to take on high-cost debt.

Recent data from the Consumer Financial Protection Bureau (CFPB) underscores the greenfield opportunity for providers to offer alternative financing and personalized payment plans — upfront.

As reported this week, a new report from the CFPB found that consumers spent $1 billion in deferred interest payments when using medical credit cards.

The CFPB said in its findings that financing terms for medical credit cards and medical installment loans include interest rates that the bureau termed “significantly higher than traditional consumer credit cards,” where the rates on those cards can edge beyond 27%.

The embrace of medical credit cards comes as the average deductibles for people with employer-sponsored insurance have grown 336% in the last two decades, from $650 in 2002 to $1,945 in 2020.

As the CFPB wrote, “it is increasingly likely that more people will use financial alternatives, including different forms of credit, to cover routine and unexpected healthcare costs.”

And in detailing the range of options that are out there, the report noted that Installment loans that originate with a medical provider “tend to have zero or low-interest rates,” adding that “loans originated through financing companies tend to charge market interest rate or above, depending on a patient’s credit risk.”

We note that beginning last month, gauging the impact of that debt may be a bit murkier. The three credit reporting agencies — TransUnion, Experian and Equifax — said they would no longer report medical debt in collections below $500 (and that’s the majority of such debt).

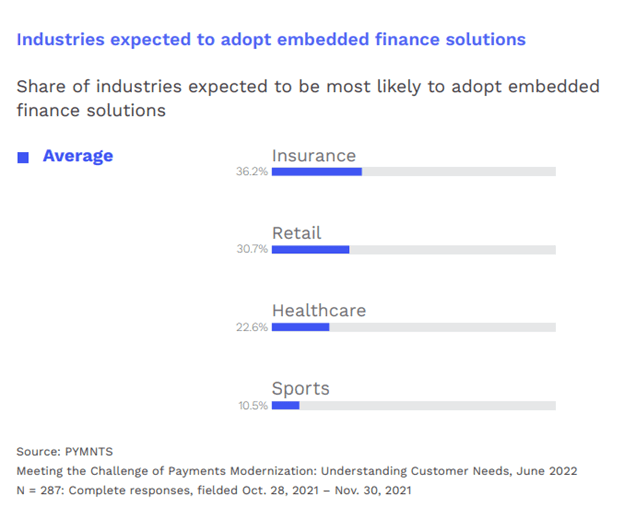

As PYMNTS data has shown, embedded finance is one avenue of promise within health care. As many as 11% of millennials have used installment options to pay for medical care, and 13% of paycheck-to-paycheck consumers with issues paying their bills have embraced those options. As the chart below shows, there’s some recognition of the need to bring more solutions into the fold to help patients pay for care.

Elsewhere, we’ve spotlighted the emergence of buy now, pay later (BNPL) applications across a range of practices within the medical industry. As detailed here, in one example, the payments platform TempoPay offers a zero-interest, zero-fee, flexible payment card that allows employees to repay immediate medical expenses and health-related services over time via deductions from payroll, personal bank account, or HSA.

In a report earlier this year, Healthcare Payment Pains Push Patients to Digital Portals, PYMNTS and Lynx found that there’s an increased recognition that digital channels can smooth the payments process itself — and give providers new avenues for reaching consumers with financing options that include, and go beyond, traditional credit products. As reported by consumers we surveyed with an online account with a digital healthcare or wellness-related portal, 48% reported that online channels improve at least one part of the overall payments and billing management experience. And 29% said digital portals make the experience (including payments) more convenient.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More