Corporations can realize $250k in value with $250 million in AP spend from moving to 100 percent electronic payments. That’s the experience that NVoicePay CEO Karla Friede and Coupa General Manager Ashish Deshpande have seen when suppliers are given control over how they want to be paid electronically and businesses have a single system to accommodate that. Friede and Deshpande participated in a recent PYMNTS.com Digital Discussion to explain how they’ve not only seen this work, but helped clients realize those benefits.

THE B2B DIGITAL PAYMENTS CONUNDRUM

Based on research provided by Ardent Partners Ltd., the number one priority in accounts payable is migrating off paper-based processes to increase speed, efficiency, errors and more. According to Friede, this does not come as a surprise, as accounts payable may be “the last island of paper” in any given business.

“I have been in the industry for the last 10-15 years, and I have been seeing the same trend. It doesn’t seem like we’ve made any progress to move off of paper in spite of a plethora of solutions out there,” said Deshpande. Coupa, a cloud-based platform, saw this phenomenon too. When it came into the market, they saw the lack of adoption as a root problem – and accounts payable systems were built for expert users, not any user.

On the payments side, there is a huge priority to move off of paper, but the payment landscape shows that the majority of companies are still very paper-based. Research indicates that 70 percent of all corporate payments are still issued by check. The implication there, said Friede, is that 30 percent of the world has moved to electronic payments. But that 30 percent of the world has not been able to maximize their digital procurement to purchase process and the solutions have not delivered on the promise of that move.

THE COLD HARSH REALITY IN B2B PAYMENTS

“Using a P-card in accounts payable is like using a screwdriver to hammer a nail,” said Friede. “You can get it done, but it’s not very effective.”

The B2B payments landscape is littered with failed solutions and this has impacted the customer environment, Fried said. Customers haven’t had all of the pieces in place to move to 100 percent electronic solutions. Businesses do make some payments through ACH, even some that have perhaps adopted a P-card program and bought into the idea that they could move into a high percent of electronic payments by using a P-card. Other customers may have a forced workflow that they started for a solution they tried to adopt, then abandoned.

The majority of companies are only making 30 percent of their payments electronically, and in this environment, these companies are considered to have done pretty well given the solutions environment.

GETTING TO 100 PERCENT | THE 5 STEP PROCESS

The cloud is now bringing to payments the efficiencies it has brought to procurement. Key things that B2B payment solutions should be delivering to customers are:

1) SIMPLICITY: This applies to enterprises of all sizes, and means there is one workflow for all payments, accounting systems, and banking partners. No major process changes are necessary, such as changes to suppliers or customers. If businesses have to change their workflow to adopt it, or dictate a path for an invoice, it won’t be adopted. Simplicity is also about a choice in way customers want to send their payments and for suppliers which kinds of payments they want to accept.

2) FLEXIBILITY: Simplicity could mean restriction, but the cloud delivers flexibility in many ways, creating great user experiences. With cloud-based solutions comes the ease of implementation (measured in hours, not months), payment visibility, payment control, and ease of a real-time reconciliation.

Cloud-based solutions are bringing higher adoption rates to the table because they allow everyone in the business to start immediately using them. Training customers takes only an hour, and it lowers the barrier to adoption.

3) SUPPLIER ENABLEMENT: Ongoing supplier enablement is key. This means setting up the supplier and getting them ready to receive payments. In B2B payments, before a business pays a supplier, they have to collect some information: 1) what kinds of payments that supplier will accept, 2) contact point for remittance, 3) if the supplier accepts a form of ACH payment, the account and routing number is needed.

One-time supplier enablement doesn’t cut it, said Friede, as suppliers change over time. Unless someone is continuously managing the information, those customers cannot get to a solution that is 100 percent electronic. Today, there are solutions that maintain and allow for supplier enablement on an ongoing basis, and that’s critical.

4) PAYMENTS OPTIMIZED: Enabling digital payments is only the beginning. Payments have to be optimized at each point in time, dynamically matching up what the customer wants to pay with what the supplier accepts to deliver payment.

5) PAYMENT SUPPORT: Not a lot of solutions talk about their payments support or the ability to deliver it to both the customer and supplier. When dealing with B2B payments, there is a need to answer the question at that point in time. When questions arise, there should be one source for all payment questions.

Also, in payments, security is really “table stakes.” The most advanced solutions have those pieces in place – PCI compliance, SSAE reports, and payment liability. This is a foundation of all good solutions, and it’s important to start by asking for documentation.

ASKING FOR DOCUMENTATION

In payments, security is really “table stakes.” The most advanced solutions have those pieces in place – PCI compliance, SSAE reports, and payment liability. This is a foundation of all good solutions, and it’s important to start by asking for documentation.

NVOICEPAY AND COUPA TEAM UP

NVoicePay’s solution optimizes payments and pays 100 percent of suppliers through the same electronic process. It’s a simple workflow, and customers that have had to put up with partial solutions and multiple processes do not have to anymore, and the cloud has enabled this as well as the dedication to service.

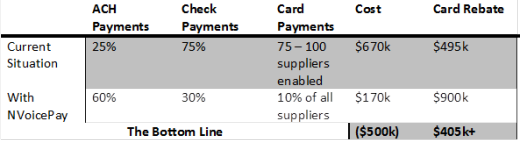

Coupa is partnering with NVoicePay because they see the value that customers receive. According to a Coupa case study based on one of its retail customers, 25 percent of payments made by the retailers’ active suppliers are ACH, and 75 percent of the payments are paper checks. The current cost is $670k, with a card rebate of $495k and 75-100 suppliers setup for card payments.

With the NVoicePay solution, 60 percent of payments would be ACH, 10 percent would be card payments, and 30 percent would be electronic prink check payments. The cost of the solution is $170k (a $500k cost reduction in this case) and the card rebate is $900k (a $400k increase in this case).

DOING THE MATH

Optimizing payments and pays 100 percent of suppliers through the same electronic process, based on supplier requirements, is the end game. But it is easier said than done. Business customers that have had to put up with partial solutions and multiple processes don’t have to.

Coupa partnered with NVoicePay to steamline the B2B payments process of their customers. According to Coupa, one of its retail customers reduced its costs by nearly 75 percent and improved its card rebate by nearly 100 percent.

THE ROI OF B2B

Corporations can realize $250k in value with $250 million in AP spend from moving to 100 percent electronic payments with the NVoicePay solution. The key foundational elements, said Freide, are ongoing supplier enablement, as well as payment optimization. Enterprises of all sizes, she said, can and should be realizing this value.

To listen to the full digital discussion, click here.