Banks embarking on a banking as a service (BaaS) journey may feel they have their work cut out for them, especially if they are relatively new to the digital banking scene. While traditional financial services such as loan approval, credit issuing and know your customer (KYC) are still vitally important to a smooth and secure BaaS experience, banks also must take on new functionalities, such as the use of application programming interfaces (APIs), payment gateways and a host of other technical capabilities.

Developing in-house BaaS solutions might work for large financial institutions (FIs) with dedicated IT staff, but the majority of banks will need to partner with technology providers to implement BaaS. This month, PYMNTS explores how banks can partner to enable BaaS and how these partnerships can help banks unlock opportunities for greater personalization.

The BaaS playing field

An understanding of the players is fundamental before deciding how or whether to take the plunge into BaaS. The first category of players consists of traditional banks, generally without strong technology expertise, that offer their licenses to digital banks or BaaS providers to enable nonfinancial companies to deliver banking capabilities to their customers. The second category consists of hybrid players that possess not only banking licenses, but also strong technology and API expertise. The third category includes API technology players that do not possess banking licenses but have a particular focus within BaaS, such as payments or cards, that may be especially appealing to certain license providers.

Incumbent banks must first determine whether BaaS can benefit them, either as users or as in-house providers themselves. For those that choose to enter the playing field, the best option will often be partnering with a technology provider that can develop the most products, allowing the bank to optimize customer experience at maximum efficiency.

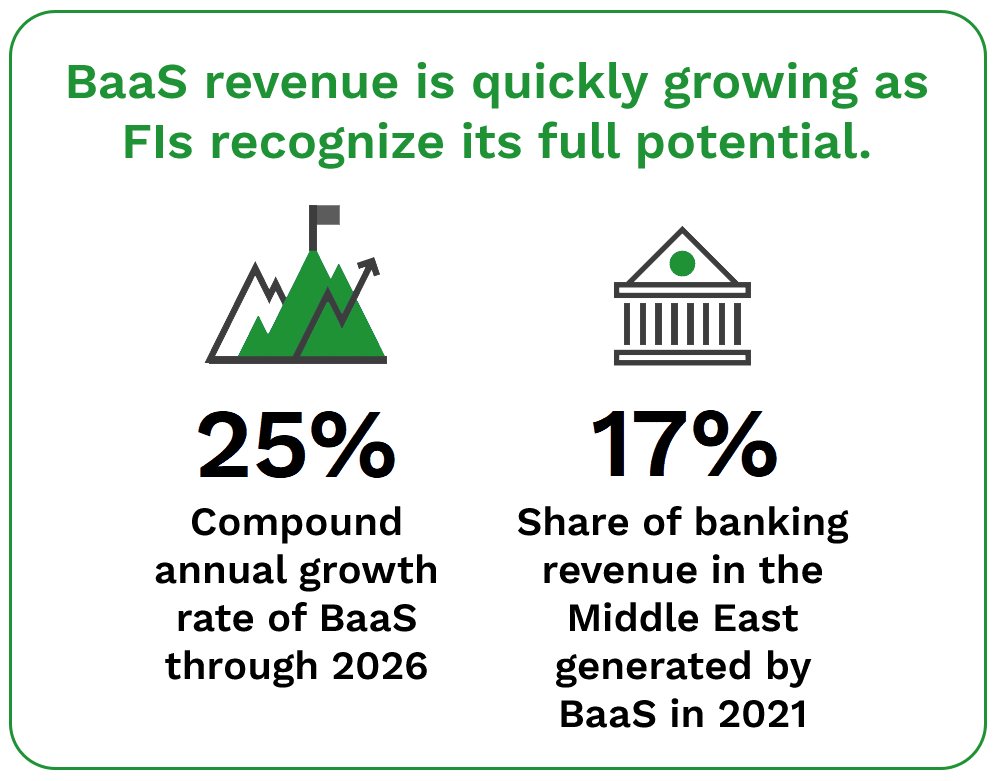

Enabling BaaS through partnerships can pay substantial dividends to banks. Revenue from BaaS operations in the Middle East alone is expected to total $5 billion by 2026, for example — 4% of the region’s total banking income. The potential for personalization can also pay in customer loyalty.

BaaS for unlocking personalization

Working with businesses on BaaS applications provides FIs with new data streams regarding the services that customers use most, the features that result in the most engagement and a host of other actionable data points. Banks, in turn, can mine data ecosystems via platform models to gather real-time insights and improve the personalization of both their BaaS offerings and their in-house banking services.

Customers are seeking increasing levels of personalization in their banking experiences. A recent survey found that 72% of banks reported an increase in demand for personalized financial services in times of economic strain, and 61% said that customer experience expectations have risen in recent years. Delivering personalized experiences via BaaS could be vital to retaining these customers in the face of increased FinTech competition.