PYMNTS conducted a comprehensive survey of more than 30,000 consumers across 11 countries for its December ConnectedEconomy™ Index, “How the World Does Digital.” Concentrating on global digital transformation, the Index maps out how consumers worldwide integrate online tools, make transactions and participate in other activities via digital means on a regular basis.

Focused on Q3 2022, this edition of the Index demonstrates that overall global engagement in the ConnectedEconomy™ rose for everyday activities such as marketplace shopping, streaming music and online dating. Consistent gains in routine activities being absorbed into consumers’ daily lives signal steady growth for the global digital transformation, and Australia’s connected engagement for 2022’s third quarter illustrated just that. It mirrored the Index’s overall trajectory, with small, steady gains in daily, weekly and monthly digital activities.

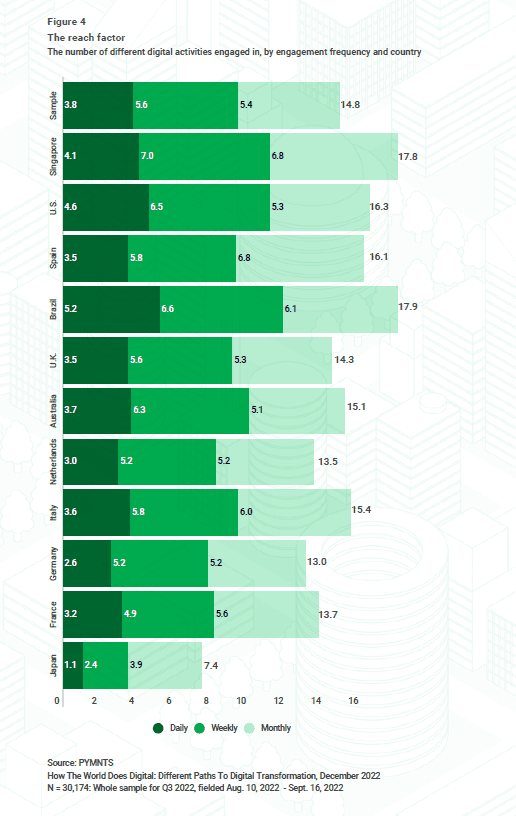

When measured by reach factor — the number of digital activities local consumers engage in regularly — Australia’s engagement may appear average for the Index. With a reach factor of 15.1, it is fifth among our 11 studied countries. A closer look, however, reveals that its digital payments innovations are anything but mediocre. The country continues to reimagine the potential of buy now, pay later (BNPL) and similar programs and is leading the worldwide charge in providing a regulatory framework for these offerings.

Australia is serving as a trailblazer when it comes to regulating BNPL programs, as the country considers treating these plans similarly to credit cards or other loans. Australia’s Credit Act doesn’t apply to buy now pay later (BNPL) and other installment plans, which has led the government to suggest three proposals to regulate the sector. The first is driven by stronger self-regulation and affordability tests. The second proposal partly brings BNPL under the Credit Act, requiring companies to obtain an Australian credit license to continue doing business. The third option has the sector fully regulated by the Credit Act, holding BNPL firms to the same standards as credit card companies.

PayPal is publicly supporting these efforts, releasing a letter earlier this month saying the company favored a “tailored, proportionate and thoughtful regulatory framework” for the industry.

Offerings in the region are plentiful. For example, National Australia Bank (NAB) provides its customers with a BNPL service, offering Australians more financial flexibility. Registered customers can access up to $1,000 and split purchases into multiple installments without any late charges, interest or account fees. Western Union has also entered the Australia installment plan space with its recent Beforepay partnership, offering consumers a “send now, pay later” service. The joint product combines Western Union’s cross-border money movement abilities with Beforepay’s wage-advance solutions. Customers can borrow up to $2,000 AUD for remittances to more than 200 countries and repay the funds on installments.

Each country tracked by the Index is forging its own path toward digital transformation. Australia’s BNPL innovations is just one strategy for countries finding their place in the ConnectedEconomy™.