Money movement is meant to be fast, safe, and, for FinTech customers, done any way they want.

But in one recent iteration of the 2023 “Money Mobility Index,” done in collaboration between PYMNTS and Ingo Money, we found gaps between what customers want and the FinTechs issuing accounts have (so far) delivered.

Ours is an increasingly digital world, where FinTechs jockey with traditional financial institutions (FIs) for customer loyalty, for the promise of speed and agility as technology has disrupted — and still will disrupt — the competitive dynamics of the financial services industry.

The account holders, of course, want to move money with aplomb between their own accounts — and to make sure that funds can be deposited into their accounts from outside parties across payment modalities spanning cash, ACH wires, debit and credit … well, you name it.

The FinTechs have their work cut out for them, given the fact that the data show frictions are still firmly in place. The mechanics of money movement, of data flows, compliance and other considerations tend to impede the speed (and success) of how money leaves and lands in accounts.

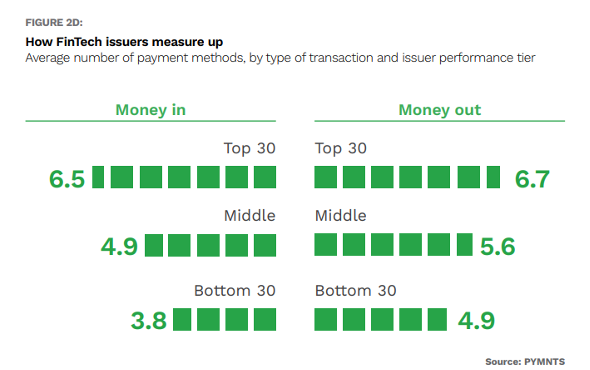

More Options May Mean More Loyalty

The fewer the number of payment options that are option for senders and receivers, the lower the satisfaction these FinTechs garner from their customers.

And as the accompanying chart shows, the highest “scoring” providers are the ones that offer at least six methods for senders and receivers to mull as they transact. The sentiment gleaned from more than 3,600 respondents shows that 23% of the top performing FinTech issuers generated more than $500 million in revenues, while 27% generated between $5 million and $10 million. The largest FinTech issuers are more adept at providing streamlined procedures to move funds into accounts: 57% reported that their customers face no problems when receiving funds.

Real-time access to funds, the data show, is top of mind for FinTech customers. Faster payment remains a leading expectation among account holders, and we find that the more instant payment options issuers provide, the more their customers are apt to use their accounts. We note that these findings predate FedNow, the Federal Reserve’s instant payment service that debuted at the end of last month. FedNow, of course, is likely to raise awareness of 24/7/265 funds availability, which means that the bar is going to be set ever higher for all manner of financial services providers.