Contrary to conventional wisdom, having good credit, an excellent FICO score, and financial stability may still not be enough for many consumers to take out a credit card and splurge.

This, as new PYMNTS data shows that among worry-free consumers who have not had a credit card in the past 12 months, 40% of them say they do not use them because the temptation to overspend is too great.

The findings come in The New Credit Model: Why Financially Worry-Free Consumers Still Want Alternatives, a PYMNTS and Sezzle collaboration, and shed new light on consumers’ retail purchasing and payment preferences. The research also presents new evidence on the need for retailers to rethink the way they’re attracting affluent or worry-free consumers, who average 52 years of age and oftentimes earn upward of $100,000 annually.

Perceptions Matter

Nearly half of those surveyed — 46% — said they thought they could improve their credit scores by opening up a new credit card. However, 40% of financially worry-free consumers said they have not had a credit card over the past 12 months, not just because of overspending concerns, but because they felt interest rates and fees were too high, or in 15% of cases, due to mistrust of credit card issuers.

While the financing decisions and options available to consumers living paycheck to paycheck are clearly more limited, the credit push-back trend at the upper end of the economic spectrum is more puzzling, albeit in line with recent spending trends that reflect a growing preference for debit.

Read more: Paycheck to Paycheck Consumers Squeezed By Largest Import Food Price Increases In 10 Years

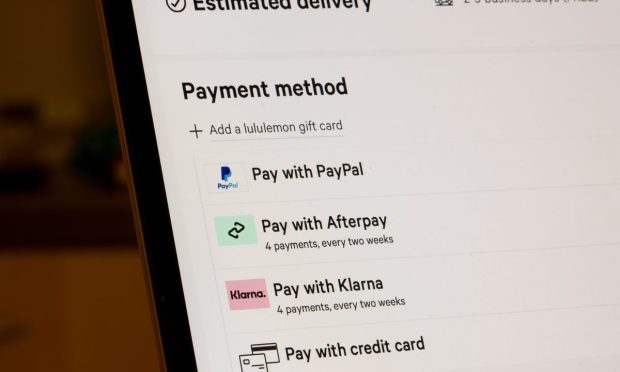

But there is one thing the data found that consumers agreed upon — regardless of their financial station — and that is that flexibility and choice matter.

Shifting Priorities = Retail Opportunities

Consumers are generally becoming more aware of individualized payment options and how to take advantage of them as needed. On that note, there’s a growing interest among the more financially well-off to have traditional credit card alternatives, according to our report. In short, this group is very interested in finding new ways to save money and better manage how they spend. Although this consumer group may not generally struggle with making ends meet or live paycheck-to-paycheck, they do want to focus on budget management.

A reported 43% of financially worry-free consumers said if they had a big one-time retail expense, they’d be willing to break it up into installments such as Buy Now Pay Later, with 24% of this coveted demographic indicating they’d do so to cover medical expenses too.

Regarding paying for necessities like food, just 14% of financially worry-free consumers said they’d consider paying for their groceries via a payment installment plan, and only 7% would use BNPL to pay their rent or mortgage.

Embrace the Budgeting Process

Most financially worry-free consumers see flexible payment options as a means of freedom, with 57% saying financial choices and payment options help them manage their spending.

Flexible payment options, therefore, represent a way for consumers to continue living within their means, provide a bit of a financial buffer when unexpected expenses come up and allow them the ability to buy more expensive items without feeling guilty that they’ve spent too much money. For the financially-worry-free, flexible payment options also are valued as a means of helping bump up credit scores.

As a result, retailers must get inside the heads of worry-free consumers and recognize how offering payment options will improve consumer buying power and customer retention. Add in the increasingly important attribute of helping consumers improve credit scores and achieve their financial goals, and the need for merchants to offer solutions beyond the traditional credit card is a lock.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More