Bank earnings came first, putting up card spending data that spotlighted consumers’ willingness to keep spending across debit and credit cards.

Retail sales data released Tuesday (Oct. 17) by the Census Bureau dovetailed with banks’ earnings, giving further credence to the sentiment that households in the United States have been resilient.

But questions remain. How long can things keep going? And how much of the sales gain is simply fueled by inflation — and the expectations that inflation is going to ramp up, which means that sales have been “pulled forward” from future periods.

The Headline Numbers

As measured in September, retail sales, overall, were up 0.7% as measured from August levels, which were in turn up 0.8% from the prior month. September’s sales were also up 3.8% year over year.

The data showed that only a few categories lost ground, marked by sales declines. Electronics and appliance stores’ sales were 0.8% lower than August’s levels, and clothing and accessories retail sales were down a commensurate amount, also month over month.

As to individual categories where there were notable gains, spending at grocery stores was 0.4% higher in September, month on month, and 1.6% higher than a year ago. Consumers spent 0.8% more last month at health and beauty retailers in September, up a whopping 8.3% from last year.

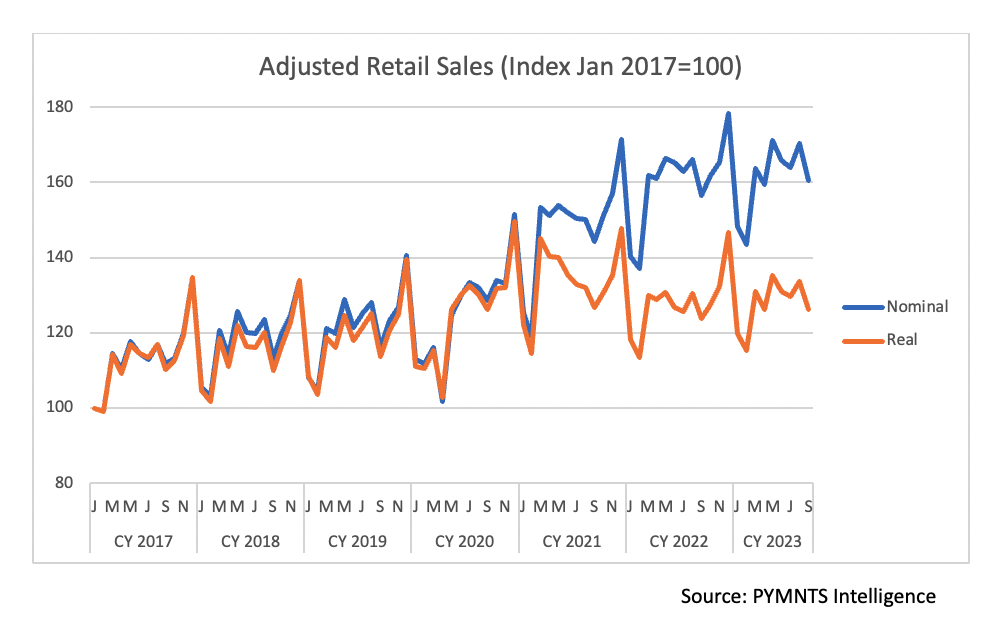

The Census Bureau numbers are not adjusted for inflation. But inflation has been a key driver of gains. When adjusted for inflation — and depending on where you look — sales are at best flat, and in many cases are declining.

As PYMNTS Intelligence found, trailing 12-month data indicates that sales gained 2.9% — that’s the unadjusted number. Adjust for price gains, and the boost is a bit smaller — at 0.8%. When adjusted for inflation, the trailing 12-month sales are 3% less than sales in the corresponding 2021 period.

In other words, we’re able to buy less — and we are buying less — even though we are spending more dollars than we were just a few years ago. The chart shows the difference between nominal and real (adjusted for inflation) sales using 2017 as the benchmark.

Running to Stay in Place but Falling Behind

Against that backdrop, then, the retail sales “surge” belies a consumer who is increasingly pressured to reach some parity with the way life was lived just a few months ago.

As noted by PYMNTS CEO Karen earlier in the month: “Over the last three years, most consumers have seen double-digit price increases against paychecks that haven’t kept pace with inflation. It’s that pain in the pocketbook that influences their perception of what the rate of inflation is, what a strong economy looks like and how long it might take to get there.”

PYMNTS has estimated that everyday goods and services are as much as 20% more expensive than they were in January 2020, and that’s through September of this year. Strip out the ever-volatile gas and energy prices, and the collective costs of food, clothing and shelter, among other categories, have leapt by 26%. In the meantime, consumers expect inflation to be lofty and price hikes to continue until sometime in 2025.

If consumers expect prices to keep rising, and they don’t feel like their paychecks are pacing those increases — 85% of consumers PYMNTS surveyed share that mindset — then they may be “pulling” future purchases to the here and now, ahead of the holidays, ahead of an uncertain 2024.