There is hardly a more difficult conversation to be had, CreditRiskMonitor CEO Jerry Flum told Karen Webster in a recent conversation, than the one the finance guys have with a sales guy about why they can’t approve shipping out a big order to a big buyer – especially if that buyer has a long-term relationship with the supplier.

It is, nonetheless, a conversation that more and more companies need to have up and down their organizations when making decisions about trade terms, and even about which companies to do business with.

Take Toys R Us, Flum and Webster noted. It’s just the latest cautionary tale about why these conversations must be the exception and not the rule on the topic. Brands and toy manufacturers that shipped their products on credit to the failing chain will now likely be left with pennies on the dollar – if any pennies at all – as assets are liquidated to pay creditors ahead of them in the line of payees.

So why are so many suppliers left holding the bag?

“The dirty little secret is that companies on the road to bankruptcy pay their bills – and often on time,” said Pete Roma, CreditRiskMonitor SVP, “right up until the day before the lights go out.”

That, Roma said, lures companies into a false sense of complacency when dealing with buyers, particularly the big ones – until it is, unfortunately, too late.

Roma and Flum blame a lack of reliable data that can put the right tools into the hands of the finance and credit risk managers to assess the risk of companies – public and private – and take steps to de-risk their trade terms with them. It also happens to be why CreditRiskMonitor was founded some 20 years ago.

“We’ve spent about two decades building [risk] scores, and at this point we are 96 to 97 percent accurate in our bankruptcy predictions,” Flum noted, something he said is becoming increasingly crucial because there is a lot more risk out there than most people understand.

A Different Kind of Credit Score

While the Toys R Us crash-and-burn came as a surprise to many, who perhaps saw the brand as too iconic to fail, Roma was not one of them. However iconic the retailer may have been, Roma noted, their system had already ranked it with a score of 1, which indicates the riskiest type of firm.

CreditRiskMonitor produces these scores using a model that examines market capitalization and stock price volatility as measured by the Merton credit risk model, a modified version of the Altman double-prime Z-score, ratings by the credit rating agencies (Moody’s, Fitch and Standard & Poor’s) and a proprietary “crowdsourced” model based on observed research patterns of risk managers who tap into the CreditRiskMonitor platform.

“It is a very proactive form of modeling,” Roma noted. “The risk professionals using our platform are large firms, and although we look at the worst case scenario – bankruptcy – we produce data that helps companies get out in front of it, which is why it is a graded scale.” Scores range from a 1 (bankruptcies in waiting) to a 10 (rock solid).

If, for example, a supplier is working with or wants to work with a buyer with a 1 or 2 rating – à la Toys R Us – he might decide to modify the trade terms they are offering. Instead of shipping goods and waiting on payment for 30 or 60 days, he noted, firms can adjust.

On the buyer’s side, Flum noted, it might also mean seeing that a supplier is getting in trouble and having enough time to find another. Or it might even mean buying that supplier because they comprise a rare or truly fundamental part of a firm’s offering.

But what is key, Flum told Webster – and Roma reiterated – is that both buyers and suppliers are ready for their partners to face disruptions, so they are not knocked down like a domino in the event that something goes wrong for one of their partners.

So Have You Heard the One About the $2.5 Trillion Ticking Time Bomb?

Flum noted that if one were to go by the reports of the media and the talking heads, everything in the economy is just hunky-dory. He thinks those people are very dangerously wrong.

“Looking at the data we look at, there are problems in many places in the economy that are worse than they were in 2007-2008,” he said. “That this is getting missed in the papers and nightly news is beyond me.”

The problem, he noted, comes down to suppliers shipping to buyers and then waiting as much as three months to get paid, combined with the reality that businesses across verticals have radically and drastically over-leveraged their balance sheets.

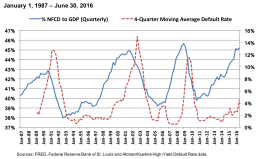

“Those gaps are a ticking time bomb, and when you look at the scale of all that debt, it’s easy to understand that there is a 2.5-trillion-dollar time bomb,” Flum emphasized. “I’m not anti-debt; there is a normal amount of credit and debt risk in any modern society. But the excessive leveraging we are at today – this isn’t something we’ve seen since the beginning of the Great Depression,” Flum noted, referring to the below chart to illustrate the level of debt that firms have taken on over time.

That level of indebtedness, Flum and Roma explained, occurs because debt has been cheap in the era when central banks have held the interest rate at, near or, in some cases, below zero. The incentive for business, then, was to absolutely fill balance sheets with debt, because it was so cheap to do so.

As for where that money went, the answer varies depending on vertical. Sometimes it went into taking retailers private, other times it went to stock buybacks or dividend payments. But the net result, Flum told Webster, is that there is a “staggering amount” of high-risk businesses that will impact everyone on some level.

“The investment world owns all this paper, and there is a much higher risk of not being paid back on it than people with retirement funds – which are part of that paper – think there is,” said Flum. “And this took a long time – like 15 to 20 years – to get to the excessiveness we see in debt all over the world.”

As long as firms remain successfully in the black, they can service their debt, Roma noted. But when business slows down, trouble begins. And because of the interconnectedness of the economy – combined with the fact that debt is so pervasive and spread across market segments – it doesn’t take all that many firms falling apart at the same time to create a lot of up-and-downstream chaos.

“Then you start seeing very bad sequential problems emerging – like Great Depression bad.”

Which is not to say, Flum and Roma noted, that the sequel to the Great Depression is necessarily upon us. What their data shows isn’t that the end is nigh, but that there is a lot more risk out there – and more interconnected risk – than most people are fairly accounting for, which is dangerous.

Risk, they noted, is part of a functioning credit system, and it can be mitigated. “But for people to mitigate a risk properly, they have to know it’s there.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More