As more transactions move online, banks are girding for, and doing battle against, a rising tide of fraud.

As noted in the report “The State of Fraud and Financial Crime in the U.S.,” a PYMNTS and Featurespace collaboration, 200 executives working at financial institutions (FIs) with assets of at least $5 billion noted that fraud attacks are becoming more commonplace.

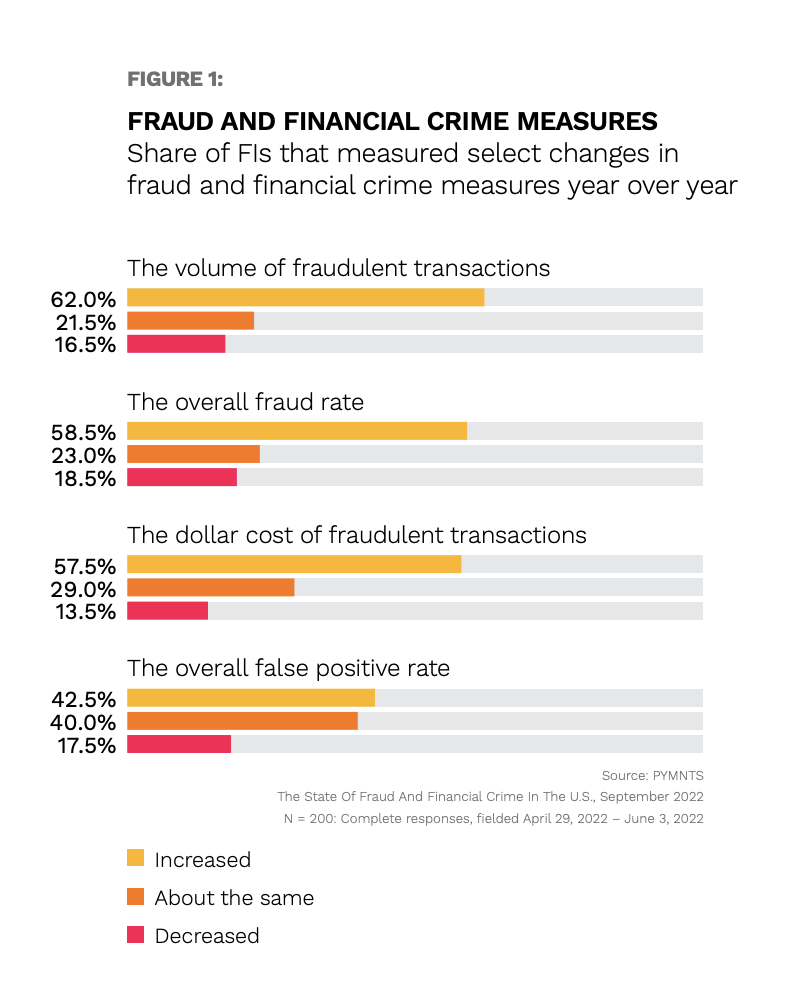

A total of 62% of FIs surveyed said the volume of fraudulent transactions is on the rise, and roughly 22% said the pace remains the same.

Only 16.5% said the volume is declining.

Making off With More Money

A full two-thirds of FIs have seen gains in fraud rates, and more than half of respondents said the dollar value of the fraud has increased.

Those data points indicate that bad actors are, for lack of a better term, winning the battle as they seek to compromise systems and make off with stolen funds and stolen data. The report found that the increase in fraud encompassed most payment methods issued by FIs, although credit cards were especially targeted. Fraud rates related to credit cards increased year over year for 64% of FIs. More than half of FIs reported an increase in fraud related to Zelle, and 32% said the same for Venmo transactions.

There are at least some pain points in the mix when it comes to FIs taking the appropriate, and optimal, measures to beat back these rising tides of fraud. The report found that 66% of respondents cited complex regulatory requirements as a challenge that winds up stymying FI executives’ attempts to harness new technology to combat the fraudsters. The downside is that many FIs, “even those with comprehensive anti-fraud and anti-money laundering strategies, may struggle to avoid pervasive losses without modern technology solutions.”

See More In:

banking, Banks, credit, data brief, Featurespace, fraud, News, PYMNTS News, PYMNTS Study, Security, Venmo, Zelle