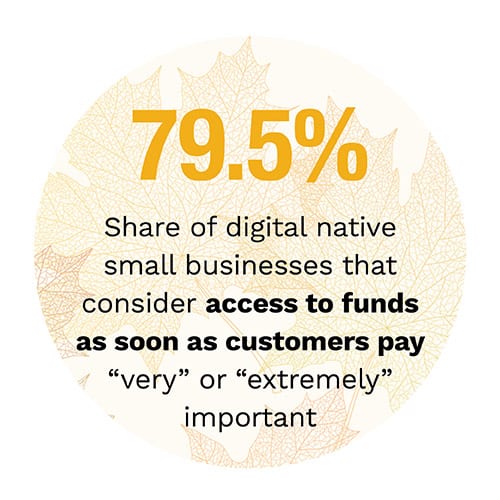

One day is long enough for many small businesses to experience negative impacts, however — and the more business a firm does online, the sooner these impacts surface, ranging from delayed vendor payments to missed payroll. Indeed, just over 50 percent of small businesses consider it “very” or “extremely” important to have access to funds as soon as customers pay, and this share rises to 79.5 percent for firms that generate at least 60 percent of their revenues online.

One day is long enough for many small businesses to experience negative impacts, however — and the more business a firm does online, the sooner these impacts surface, ranging from delayed vendor payments to missed payroll. Indeed, just over 50 percent of small businesses consider it “very” or “extremely” important to have access to funds as soon as customers pay, and this share rises to 79.5 percent for firms that generate at least 60 percent of their revenues online.

These are among the top findings in the latest The Small Business Guide To Rapid Settlement Playbook: Online Commerce And The Cash Flow Challenge edition, a collaboration with Mastercard, based on a survey of 480 firms with annual revenues of up to $10 million across a range of sectors, including hospitality, construction, retail and professional services. In the report, PYMNTS examines how the rise of digital commerce is affecting small businesses, and creating demand for solutions that can help them better navigate the new payments landscape.

To conduct the analysis, PYMNTS divided firms into three groups: digital natives, with online sales representing 60 percent to 100 percent of revenues; omnichannel, with online sales representing 40 percent to 60 percent of revenues; and brick-and-mortar, with online sales making up less than 40 percent of revenues. Firms were also divided into small businesses and microbusinesses, with the latter earning less than $500,000 a year.

The research shows that resolving settlement delays is an especially urgent matter for digital native and omnichannel businesses. Forty-seven percent of digital native small businesses said they experience negative impacts within one day of being unable to access funds, as does 38.1 percent of omnichannel microbusinesses.

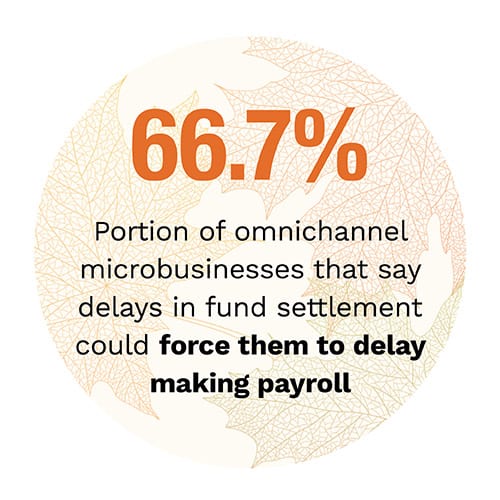

This does not mean that other businesses are spared from the effects of delayed settlement, however. In fact, 61.3 percent of brick-and-mortar microbusinesses said they might delay vendor payments as a result of not having access to cash, and 66.7 percent of omnichannel microbusinesses said this could force them to take longer to make payroll.

This does not mean that other businesses are spared from the effects of delayed settlement, however. In fact, 61.3 percent of brick-and-mortar microbusinesses said they might delay vendor payments as a result of not having access to cash, and 66.7 percent of omnichannel microbusinesses said this could force them to take longer to make payroll.

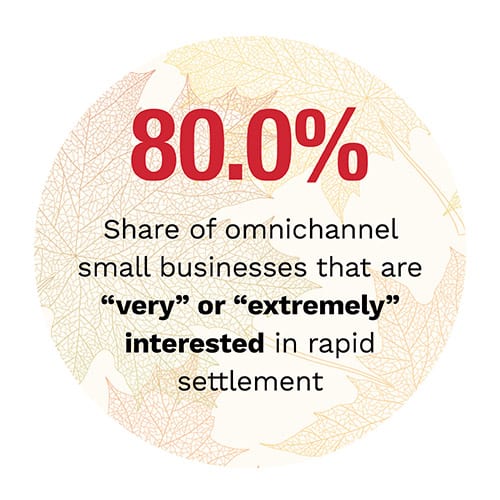

These challenges have given rise to substantial demand for rapid settlement services, which enable merchants to have access to funds within 30 minutes of payment through point-of-sale (POS) systems. Among digital native small businesses, 81.5 percent are “very” or “extremely” interested in rapid settlement, as is 80 percent of omnichannel firms. In fact, roughly the same share of these businesses would be willing to switch to POS providers that offer rapid settlement.

To learn more about how rapid settlement can help small businesses compete and thrive in the digital economy, download the report.

We live in an era when it is possible for a small business with a great product to go global almost overnight, thanks to the power of the internet and mobile commerce. Yet, the opportunities for growth have not resolved the age-old problem of tight cash flow that small businesses face. In fact, in some ways, they have made it worse: More online payments mean merchants have less cash in the till, so to speak. With the exception of cash, most forms of payment can take a day or longer to settle in merchant accounts, including digital wallets, which typically run on existing card rails.

We live in an era when it is possible for a small business with a great product to go global almost overnight, thanks to the power of the internet and mobile commerce. Yet, the opportunities for growth have not resolved the age-old problem of tight cash flow that small businesses face. In fact, in some ways, they have made it worse: More online payments mean merchants have less cash in the till, so to speak. With the exception of cash, most forms of payment can take a day or longer to settle in merchant accounts, including digital wallets, which typically run on existing card rails.