Small businesses play a vital role in the U.S. economy. There are more than 30 million companies that employ less than 500 people, representing the vast majority of U.S. firms and a key engine of job growth in the country.

Small businesses play a vital role in the U.S. economy. There are more than 30 million companies that employ less than 500 people, representing the vast majority of U.S. firms and a key engine of job growth in the country.

However, there is one issue with which small businesses have long struggled: cash flow. This challenge has persisted, even as digital and mobile technologies are making the purchasing experience ever faster and more efficient for consumers. Indeed, the diminished use of cash may have an outsized impact on small businesses, since they tend to lack the cash reserves of large companies, as well as access to generous lines of credit.

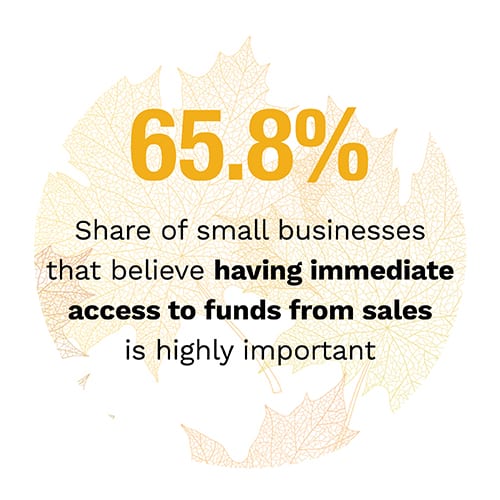

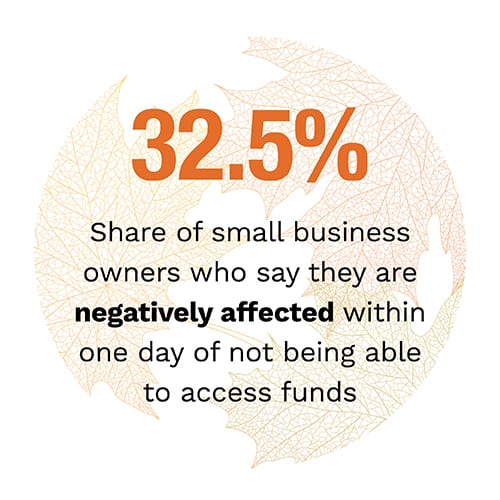

PYMNTS’ latest research lays out these challenges in stark terms: 75.8 percent of small businesses said their operations are negatively impacted by the lag time between when customers pay and when funds land in their accounts. In fact, one-third said these impacts can come within one day of not being able to access funds, and can include everything from delaying vendor payments to putting the survival of their businesses at risk. Underlying these challenges is the belief held by 65.8 percent of small business owners that it is “very” or “extremely” important to be able to access funds from sales immediately.

The Small Business Guide To Rapid Settlement Report, a PYMNTS collaboration with Mastercard, documents how this vital segment is managing these challenges in a shifting payments landscape. Crucially, the report also examines the potential for rapid fund settlement solutions to address these challenges. The report is based on a survey of 480 firms with annual revenues of up to $10 million across a range of industries, including retail, professional services and  construction.

construction.

The research confirms that the way consumers pay businesses is shifting, with cash and check use declining, and PayPal on the rise. Credit cards have emerged as the dominant income stream for small businesses, making up 21.6 percent of revenues, while PayPal is the second-largest source at 16 percent of revenues.

While digital services, such as PayPal and Apple Pay, may seem instant from the consumer’s perspective, it can take two days or longer for funds to land in merchants’ accounts, since they typically run on existing credit and debit rails. Rapid settlement allows merchants to access funds within 30 minutes of a transaction, however, typically through their own POS systems.

The research reveals that rapid settlement has already proven to be a difference-maker for small businesses. Those that have used such services are more optimistic about their growth and ability to manage cash flow. For example, 62.9 percent of companies that have used rapid settlement over the past 12 months expect their revenues to grow by at least 10 percent, close to double the rate of firms that did not use such services.

The research reveals that rapid settlement has already proven to be a difference-maker for small businesses. Those that have used such services are more optimistic about their growth and ability to manage cash flow. For example, 62.9 percent of companies that have used rapid settlement over the past 12 months expect their revenues to grow by at least 10 percent, close to double the rate of firms that did not use such services.

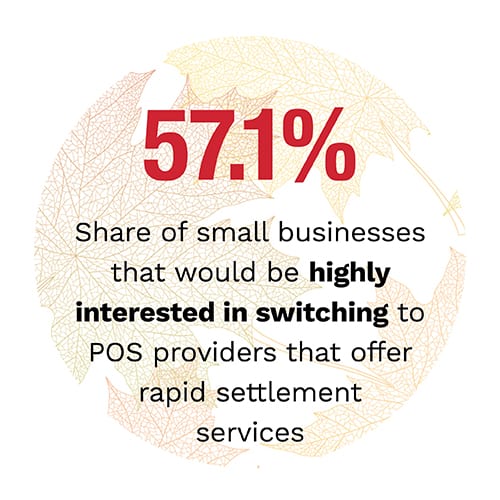

Yet, many firms are not taking advantage of rapid settlement — and this points to a wide opportunity for small businesses and their financial partners. Not only is a majority of firms “very” or “extremely” interested in rapid settlement, but 57.1 percent would be willing to switch to POS providers that offer such services. Moreover, nearly three quarters of firms would be willing to pay fees for rapid settlement in the range of 1.5 percent to 2.2 percent of the payment amount.

To learn more about the how small businesses can better navigate the shifting payments landscape, download the report.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More