Whether it’s driving innovation or creating employment opportunities, small and medium-sized businesses (SMBs) play a vital role in the economy.

However, one significant hurdle stands in their way — access to credit. SMBs are grappling with the challenge of securing the financing necessary to survive, a challenge further intensified in today’s uncertain macroeconomic landscape.

As noted in ‘What’s Next in Credit: Why SMBs Prefer Corporate Credit Cards for Short-Term Financing,’ a PYMNTS Intelligence and Cross River collaboration, only 47% of SMBs with annual revenues of $10 million or less had access to business or personal financing as of July 2023, leaving them vulnerable to financial uncertainties.

Furthermore, the share of SMBs with access to credit differs across industries. For instance, the professional services and personal and consumer services sectors are less inclined to have access to financing compared to the overall average. Only 43% of professional services SMBs and 38% of personal and consumer services SMBs have readily available access to financing.

Irrespective of the sector, however, corporate credit cards stand out as the preferred choice for 52% of SMBs searching for alternative financing, surpassing options like business loans from online lenders (22%) or working capital loans from banks (21%), according to the study.

This trend holds true for larger SMBs, generating between $50 million and $250 million in annual revenues, which have outlined several reasons for opting for corporate cards as a working capital solution in the past 12 months.

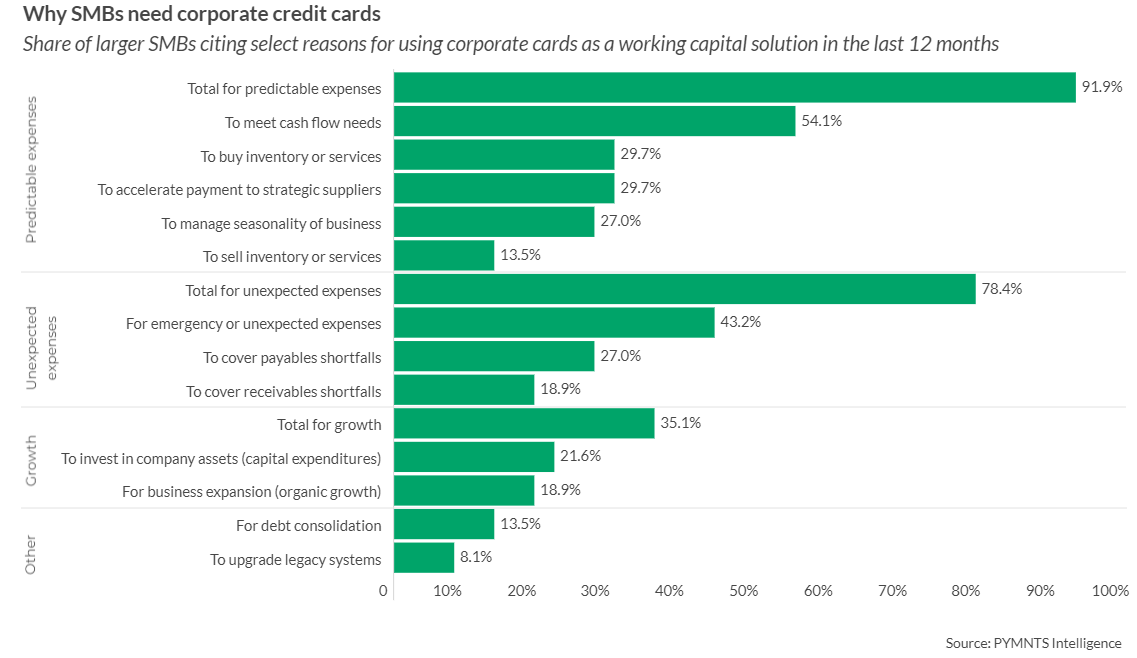

Top among these reasons is the ability to cover predictable expenses, cited by nearly 92% of surveyed firms. These expenses encompass meeting cash flow requirements, facilitating the purchase or sale of inventory or services, and expediting payments to suppliers. On the other hand, almost 80% mentioned using business credit cards to address unexpected expenses, ranging from covering payable and receivable shortfalls to handling emergency costs.

In addition to handling both anticipated and unforeseen costs, 35% of SMBs leverage virtual credit cards to support business expansion, including investing in company assets and facilitating organic growth. Additionally, about 14% of SMBs use corporate cards for consolidating debt, and less than 10% use these cards to modernize legacy systems.

That said, the path to obtaining corporate credit cards is not straightforward. Only 28% of smaller SMBs can secure these cards despite the plethora of personal and business financing options available. And among the obstacles hindering wider adoption of corporate credit cards, larger SMBs, generating between $50 million and $250 million in annual revenues, cite cost as the most significant barrier, followed by compliance requirements, eligibility criteria, and a complicated application process.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More